Rating: Buy-High Risk Price Target: $7.10

Business Overview

Qantas is one of the most recognisable brands in the world. It's been Australia's unofficial national airline almost since its inception just over one hundred years ago. It has had its ups and downs, but generally, Qantas is widely regarded as one of the most consistently profitable airlines in the world.

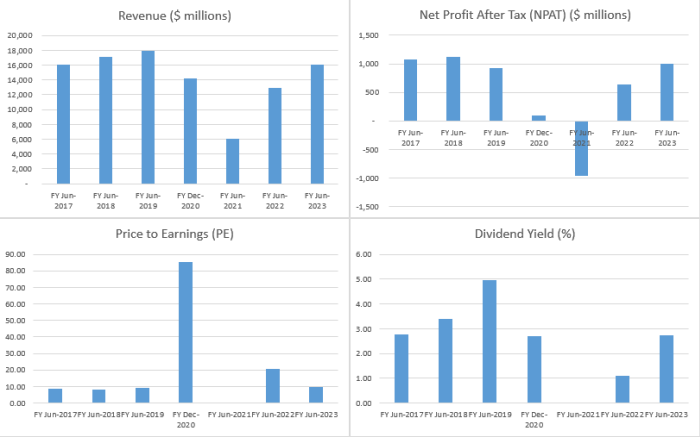

But, there's no sugar coating it, 2020 was a terrible year for The Flying Kangaroo. The Coronavirus global pandemic changed the global travel industry like never before. Locally, Australia's international border was closed on 20 March 2020, and within a week, all states and territories had also locked down interstate travel. These restrictions, and similar measures overseas, hobbled the Qantas's international and domestic operations. Revenues, which totalled $18 billion in calendar year 2019, almost completely evaporated in just a few weeks.

By the end of FY20 in June, the business had suffered a 97% drop in international travel (the remaining portion limited to repatriations), and a 50% drop in its bread-and-butter domestic travel business. In its FY20 results, Qantas reported a staggering 82% fall in revenue (don't forget the first half was unaffected by the pandemic), and a $2.7 billion statutory loss. It was also forced to raise just over $3 billion in debt and equity to ensure it could bunker down and survive the crisis.

Outlook

But markets look forward, not backwards. A number of coronavirus vaccines are already being distributed around the globe, and vaccinations are due to commence over the next few days and weeks locally. This is a major step along the path to normalisation of movement. Australia's international border is likely to remain closed for the rest of 2021, but this is unlikely to prevent a significant improvement in Qantas's financial performance this year.

International travel typically accounts for only around 5-10% of the company's earnings. Domestic travel accounts for around two-thirds of earnings, and the rest comes from Qantas's famous and very profitable loyalty program. According to Qantas's December 2020 update, domestic capacity was back to 68% of pre-COVID levels, and it is expected to rise to nearly 80% by the end of March 2021. So a big chunk of earnings is already on the way back. Add to this a major improvement in Qantas Freight, which saw its earnings contribution spike as e-commerce volumes exploded during the pandemic, and the recovery in Qantas's top line earnings could occur very quickly.

Another big driver of the company's bottom line is the massive recovery plan which management announced in June 2020. This restructuring is on track to deliver $600 million in structural cost benefits in FY21, reaching at least $1 billion in annual cost improvements from FY23 onwards.

Even better, a significant backlog of supplier payments and refunds have been cleared over the last few months, and by 31 December 2020, approximately 50% of redundancy payments associated with 8,500 job losses had been made.

Qantas management expect to be close to breakeven at the Underlying EBITDA level for the first half of FY21, and net free cash flow positive (excluding redundancies) in the second half. Their balance sheet has been bolstered by the massive capital raising in 2020, and they have plenty of liquidity ($3.6 billion) to face future challenges.

Risks

Many risks remain for Qantas of course. Net debt is rising, from $4.7 billion at 30 June 2020 to over $6 billion by end of FY21. This will need to be serviced, and eventually paid down, diverting capital from growth and potential dividends.

Also, most importantly, nobody can say with any certainty how the pandemic will play out. Will the coronavirus 'play nice' and fade off into the sunset post-vaccinations? Perhaps, perhaps not. If 2020 taught us anything, it is that things can change very quickly. The possibility for continued disruptive spot lockdowns, delays in the rollout of vaccines, and possible virus mutations are all key risks to consider before investing in Qantas.

Investment Case & Valuation

Qantas was an excellent business heading into the pandemic. It has taken a massive hit and has had to adapt and evolve to survive. It should exit the crisis in a stronger position than when it entered it, and as the world returns to normal, the business should return to strength.

We will get a better idea of how the Qantas recovery is tracking when it releases its first half FY21 results on 25 February. It's probably no surprise that first half earnings before tax, interest depreciation and amortisation (EBTIDA) estimates are wide ranging (anywhere from a $200 million loss to a $500 million profit).

We're expecting somewhere between a breakeven to a $200 million profit. For the full financial year (FY) 2021, we expect the company will report further losses of approximately $700 million, and logically, no dividend will be paid. FY22 should see a return to profits however, and based upon the current price of $5.05, the shares are trading at around 20 times expected FY22 earnings. Assuming our growth estimates can be maintained, this rate falls to around 10 times expected earnings in FY23. The dividend yield should recover to around 1-2% in FY22, and closer to 3% in FY23 (compared to a FY19 dividend yield of 5.2% fully franked).

It is clear that investors in Qantas have to 'look past the valley' to the recovery on the other side. As it tends to happen in markets though, if you wait for the recovery to occur, the share price has generally already moved higher to account for it. So, investors have to make the decision now as to whether they want to participate in the Qantas recovery, and in doing so, take on the accompanying risks.

Technical Analysis

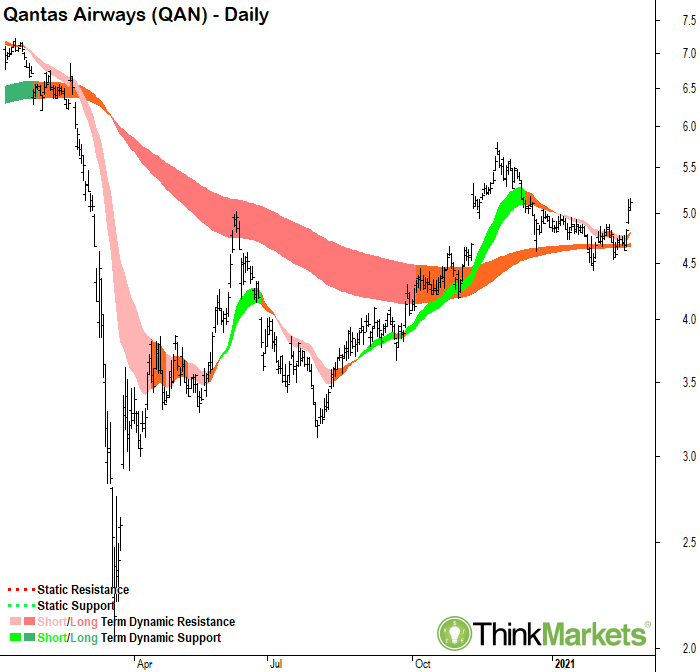

Qantas has been in a long term downtrend as evidenced by the bearish setup in the long term moving averages since March 2020. The long term moving averages often provide resistance to price increases in a downtrend, and this was certainly the case for the June rally. That rally was clearly premature, and further consolidation (long term supply removal and long term demand building) was required.

The long term dynamic resistance zone was tested again in October 2020, but this time the price broke decisively above the zone. The rally petered out as a number of spot lockdowns occurred across the states at the end of 2020 and start of 2021. This dented demand for the shares and triggered another consolidation. This consolidation, just above the long term moving averages for the most part, is a positive sign.

Also a positive, is the return to higher peaks and higher troughs in the price action as it confirms building demand and diminishing supply. The break higher on 23 February has likely kicked off a new short term price action uptrend with a major trough now confirmed on 1 February at $4.43. We would expect to witness significant support at this level going forward.

The target for the next move higher can be measured by adding the rally from the 3 August 2020 major trough of $3.12 to the 25 November 2020 major peak of $5.79. This results in an upside technical analysis target of $7.10. The all-time high of $7.46 set on 20 December 2019 will also likely impede further price appreciation in the medium term.

(Source: AusbizTV February 23, 2021. "The Call: Tuesday 24 February". Full video available from: https://www.ausbiz.com.au/media/the-call-tuesday-23-february?videoId=7399)

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

Learn and earn more today.

Visit our Education Centre