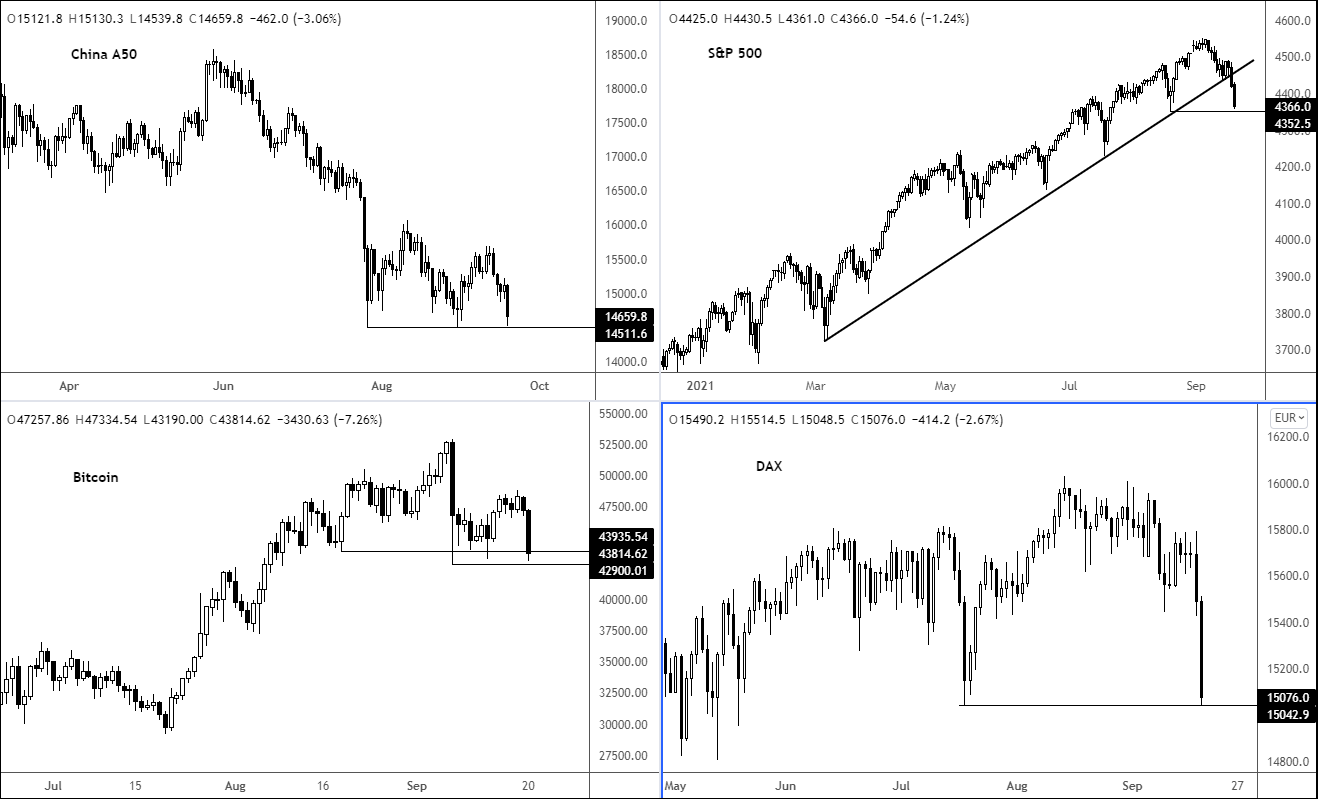

European stocks and US index futures remained deeply in the red during the European morning session, with the major indices being about 2% or more lower after a 3% drop for the Hang Seng overnight. US markets looked set to open with big gaps, which could lead to further panic selling. With risk appetite falling, cryptocurrencies, crude oil, copper and all major risk-sensitive currencies suffered.

Source: ThinkMarkets and TradingView.com

Chief among investor worries has been Evergrande’s debt woes and its potential spillover on other property developers, lenders and other sectors – not only in China, but elsewhere too. Investors are not sure whether Chinese authorities will be able to contain the fallout from a possible disorderly collapse of the heavily indebted company. The situation is made worse by the fact China will be closed in observance of the Mid-Autumn Festival until Wednesday. But Evergrande’s Hong Kong listed shared fell a further 13% as its market cap dropped to its lower ever level as a potential bankruptcy looms large. The company was due to pay interest on bank loans on Monday and some $83.5 million in interest on Thursday for its offshore March 2022 bond. Failure to make these payments will mean default, which appears likely as Chinese authorities have apparently already told major lenders not to expect repayment.

If the problems ended with Evergrande then there wouldn’t be too much of an issue as far the wider financial markets are concerned. But this could have repercussions on many other companies. So, the contagion risks may be much wider than the markets currently expect. Equally, a lot depends on how China’s authorities will respond to this crisis. Will they bail the company out, or let it collapse and make an example of it? China is also cracking down heavily on other key sectors in the economy, providing additional uncertainty hanging over the Chinese markets and economy.

Will Wall Street traders buy the dip?

Given the huge uncertainty, investors are unwilling to take any risks and we have seen the impact of that on the markets already so far today. Will the Wall Street open help to lift the mood remains to be seen. Here, investors are concerned about the risks of surging inflation undoing the recent strong economic recovery, just as the Fed and other major central banks are about to reduce their bond buying programmes.

Speaking of central banks, there will be a few major ones to look forward to this week, as the US Federal Reserve, Bank of England, Bank of Japan and Swiss National Bank all decide on monetary policy. We will also have a few potential market-moving data, including the latest manufacturing and services PMIs.

Inflation concerns on the rise

Inflationary pressures have risen sharply due to supply bottlenecks and rapidly rising oil, gas and electricity prices. The intense heatwave in parts of southern and eastern Europe saw demand for air condition and refrigeration rise sharply, just as lockdown measures were lifted in many parts of the region. Calmer weather meant the amount of renewable energy from wind was not sufficient. So, demand for gas has risen significantly to fuel power stations, causing gas stockpiles to fall sharply. Meanwhile, crude oil prices have remained strong owning to the OPEC’s ongoing supply curbs and stronger demand due to the global re-opening.

Will energy prices fall back?

Although crude prices fell back on Monday, it is not clear whether this was driven by the general risk-off trade or otherwise. If prices recovery and remain near recent highs then this will directly impact consumers’ disposable incomes, and indirectly lower their purchasing power through inflation. Rapidly rising energy prices in Europe has forced some factories to halt production. Rising input costs are going to squeeze manufacturers’ margins and hurt their profits. The drop in buying power of consumers will only make things worse. Against this backdrop, the stock market outlook appears uncertain to say the least.

FOMC meeting (Wednesday)

The dollar has not gone anywhere fast, although it has noticeably gained ground against some of the weaker currencies like the euro. Traders are expecting the Federal Reserve to start unwinding QE in the not-too-distant future, which could keep the greenback on the front-foot. At Thursday’s FOMC meeting, all the focus will be on any indications on how soon the US central bank will start to taper its bond buying stimulus programme. But after a weak jobs report, the Fed may decide to wait a little longer before being more open about its tapering plans.

Bank of England (Thursday)

Inflation has surged higher in many parts of the world as a result of the abovementioned factors. The UK’s CPI measure of inflation, for example, jumped to 3.2% year-over-year from 2.0% recorded in the previous month. It is not just headline CPI, but core CPI, RPI, PPI – you name it – everything is going up.

The pressure is thus growing on the Bank of England to act. The BoE is unlikely to hike rates at its meeting on Thursday, but what the market will be watching out for will be any noticeable change in the tone of the MPC that would suggest policy tightening is going to be imminent in the coming months. If that’s the case, we may see a sharp rally in the pound, after the currency spent much of the summer trading in a sideways range.

Global PMIs (Thursday)

Meanwhile the recent trend of economic data from China and the US have not been great, raising fears that the economic recovery is slowing at the world’s two largest economies. European data has been somewhat better, but let’s if weakness from China will weigh on growth here, too. The upcoming PMI data should provide us with good indications about the level of economic activity. As well as keeping a close eye on the headline PMI data, it is worth looking deeper into the reports to see if the indices for prices have accelerated further. As these sub-indices will provide strong indication about future inflation, we may well see a more significant market reaction in response. Further pickup in inflation momentum will make life very difficult for central banks. They will have to tighten their policies to prevent hyperinflation risks. This will not be good news, especially for growth stocks.