It’s been a tough time for investors over the last few weeks. Geopolitical factors, rising energy costs, and the spectre of stagflation, have combined to knock investor confidence and share prices alike. Volatility is way up, and it appears set to stay for the foreseeable future.

At times like this, it is important to focus on investing in stocks that first and foremost have a solid underlying business with reliable earnings growth, but just as importantly, which also stand to benefit from any tailwinds the current volatile economic environment might provide.

One of the key beneficiaries of the current macroeconomic environment is the commodities sector. Rather than simply spout off another bunch of commodity stocks however, we thought we’d take a closer look at a company which is leveraged to the success of the broader sector. There’s an old saying about the best way to make money in a commodities boom…sell shovels!

The stock featured below appears to fit the bill outlined above. Solid underlying business, check. Reliable earnings growth, check. Tailwinds, check. Management has worked hard to stave off the negative impacts of the pandemic, and the business now appears to be hitting its straps just as the commodities boom is winding up.

SRG Global (SRG)

Rating: BUY, MODERATE RISK Price Target: $0.68 (+20%)

Business Overview

SRG is a skilled engineering and operational personnel company that aims to assist clients looking to undertake construction work. Their capabilities extend across the entire construction cycle, from engineering, to construction, to asset maintenance. The fact they are a one-stop-shop in the construction space is a significant comparative advantage.

Based in Western Australia, SRG has a major exposure the to the resources sector. It’s list of mining services clients includes the who’s who of Australian mining royalty, including BHP, Rio Tinto, Fortescue Metals Group, and Gina Rinehart’s Roy Hill in the iron ore space, and gold miners Northern Star, Silver Lake Resources, Red 5, and Evolution Mining. The list goes on outside iron ore and gold (think Iluka, South32, Woodside etc.).

SRG also provides construction engineering services to government-backed road authorities in NSW, Victoria and WA, and water authorities in NSW, Queensland, South Australia, and Western Australia. It also provides services to large private contractors to these and other public infrastructure bodies, such as Multiplex and Lend Lease.

SRG certainly has a diverse range of clients across a diverse range of industries. Importantly, it is leveraged to two key themes currently driving the local economy as we emerge from the pandemic, that is, the developing commodities boom, and the ongoing ramp up in infrastructure spending. Having said this, we acknowledge that a good portion of their business is cyclical, that is, it will ebb and flow with the commodity price cycle and the broader economic cycle. Typically, such exposure has pointed to elevated risks and therefore harsher discounting of future cashflows.

After reviewing SRG’s business model, we believe it deserves to be treated differently from many of its counterparts with respect to the cyclicality of its business. Firstly, SRG management have made great efforts over the last few years to transition much the company’s income from contract based (which is the norm in the industry) to annuity based. Indeed, approximately two-thirds of SRG’s contracts are annuity based which provides it with substantially predictable recurring revenue for the foreseeable future. Secondly, SRG runs a capital light investment profile. As an engineering-focussed business its main assets are its people rather than fleets of large construction equipment.

The latter could be a double-edged sword however, as we note that labour shortages, particularly in Western Australia are pushing up wage costs and delaying the delivery of services by business just like SRG. This is a concern for us, and it is the main reason we have gone with a MODERATE risk rating when considering the execution risk associated with our earnings and growth estimates for SRG below. One important point of comfort, however, arises from the fact that the majority of SRG’s contracts have mechanisms to recoup any increased costs it experiences. With no end to the current labour squeeze in sight, there’s a very good chance they’re going to need these clauses.

Broker Consensus & Financials

There’s just the one broker providing research on SRG at the moment. They are at a “Buy” with a price target of $0.75 which is approximately 32% above the current price.

(click to enlarge each image)

(click to enlarge each image)

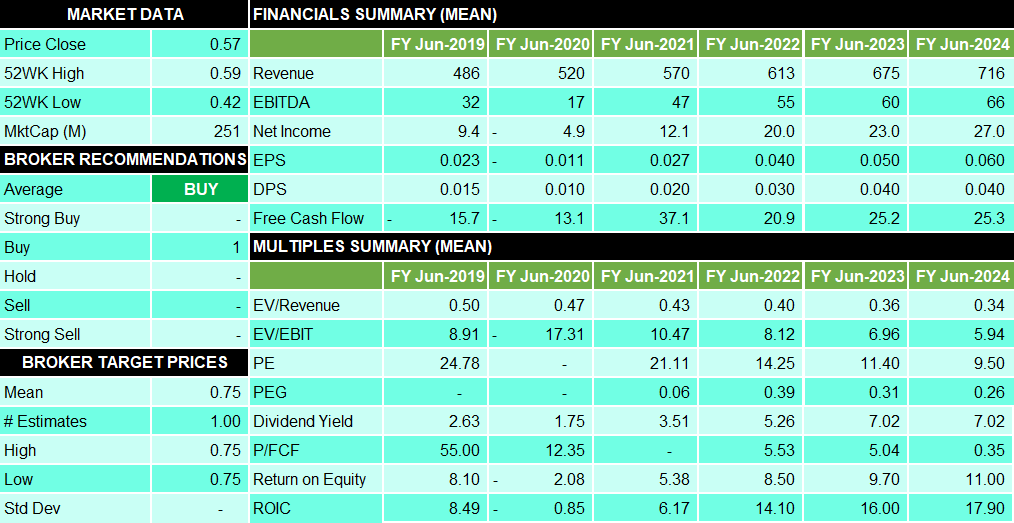

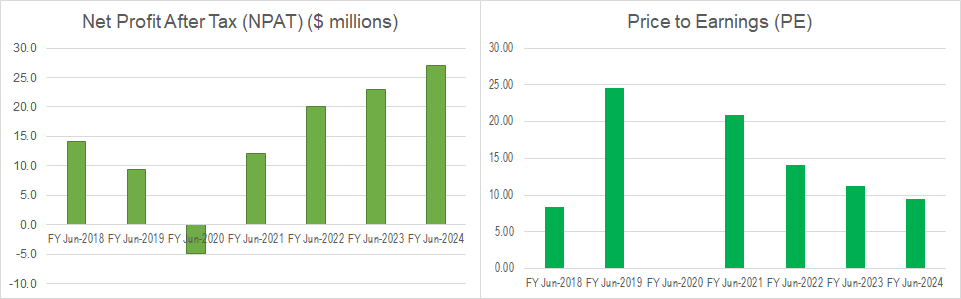

The SRG financials show that the pandemic drove a truck through FY20 earnings as the company slipped into negative EPS. The bounce back since then, as commodity prices and mining activity have both spiked, is impressive. FY21 saw EPS back in the black with $0.027 cents per share (ahead of FY19’s pre-pandemic $0.023), and we’re looking for EPS of $0.04 for FY22, $0.05 in FY23, and $0.06 for FY24. This demonstrates an impressive average growth rate of just over 20 per annum over the outlook period.

The forecast earnings growth should drive SRG's PE ratio down from the current 14 times FY22 earnings to a very attractive 9.4 times FY24 earnings. This compares favourably to the broader Australian share market average of approximately 16. The combination of strong earnings growth and a reasonable valuation bears out in the PEG, which is a guide to whether earnings growth is sufficient to justify a company’s valuation. Typically, we prefer companies with a PEG of less than 1 which signifies that its earnings growth rate is greater than its PE. SRG’s PEG of around 0.32 for FY22-24 is particularly impressive.

Also impressive, is SRG’s dividend yield, which is expected to average around 6% over this time. Even better for self-managed superannuation funds — it’s fully franked. The rest of SRG’s numbers look solid, other valuation measures such as EV/Revenue, Price/Cashflow and ROIC are each well above broader market averages.

Technical Analysis

(click to enlarge image)

(click to enlarge image)

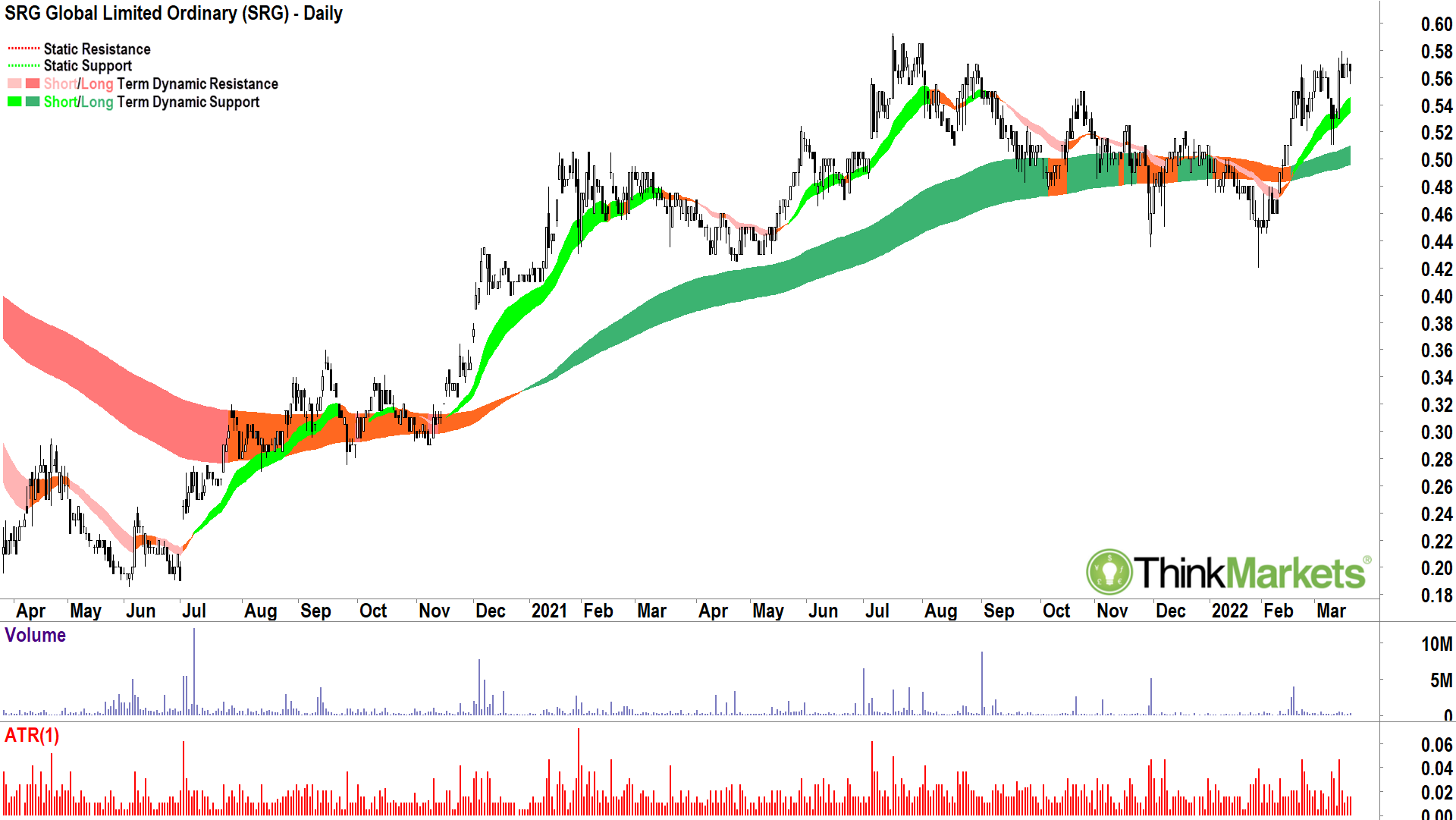

The SRG chart looks very solid. It has a well-established long-term uptrend, and it has recently resumed a short-term uptrend. The short-term uptrend appears to be gaining strength (steepening), and more importantly, appears to be offering some dynamic support to prices. There's nothing sinister in the candles, volume, or volatility indicators to suggest that either the short-term or long-term uptrends can't continue.

The short-term price action is good, not great. We can see higher peaks, but lower troughs. Ideally, we’d prefer higher peaks and higher troughs. However, we note that the last trough was impacted by SRG going ex-dividend by 1.5 cents fully franked on March 9, 2022. Accounting for this, we would expect that the price action would indeed have logged higher peaks and higher troughs.

More broadly, the price action appears to be consolidating in a sideways zone between $0.42 and $0.595. Such consolidation zones often provide major support to any eventual move higher. We view as attractive the fact price action is probing supply at the top end of this zone. It may take a couple of attempts to clear the dead wood waiting to take profits here — but an eventual breakout could bump prices nicely higher towards our valuation target of $0.68 (see below).

In summary, this is a solid chart. There are some issues as we've identified, but these are not enough to dissuade us from going with a BUY rating for SRG from a technical perspective.

Valuation & Rating

SRG’s recent interim results demonstrated that its near-term future is underpinned by new contract wins, strong operating cashflows and continued margin improvement. Longer term, we take confidence in its diverse and blue-chip client base, and its exposure to the substantial tailwinds in the mining and infrastructure sectors. Its strong balance sheet will allow it to capitalise on opportunistic acquisitions, or to continue to provide excellent capital returns to shareholders.

We have balanced the positives against the risks of continued volatility in the global macroeconomic environment, and closer to home, with respect to acute shortages in skilled labour. Whilst we feel the company has in place mechanisms to deal with the latter item from a costs standpoint, but it may still result in delays in delivering services to clients. Further, volatility in the global economy may adversely impact commodities prices, and therefore the demand for mining services and mining-related construction.

Based upon our earnings and growth rate assumptions and a target PE of 11.3 times earnings, our fair value target for SRG is $0.68. The fair value target allows for approximately 20% upside from the current price. Along with the expected dividend yield, this implies an attractive potential total shareholder return. Given its valuation, its risk profile, and its current technical picture, we are comfortable with a BUY, MODERATE RISK rating for SRG.

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.