This article is Part 2 of our four part look at the uranium market and the ASX uranium sector. In

Part 1: Uranium, the next big trend Stock Market trend? we provided an in-depth investigation of the key drivers impacting the demand and supply side of the global uranium market. This week and in future Parts, we are going to focus directly on each of the stocks which are prospective for uranium in the short-to-medium term.

With the help of my Twitter followers (thank you!), I have identified 30 ASX listed stocks which have uranium assets likely to receive some investment in the next 12 months. There are a handful of other aspirants which didn’t meet this criterion, and therefore were omitted. Perhaps they’ll make it into future uranium sector overviews! Clearly, with so many stocks to investigate, I will focus on those which are closest to either production or proving a commercially minable resource. I have provided only high-level analysis on the rest. The stocks are listed below in alphabetical order.

The Global X Uranium ETF (NYSE: URA) holds investments in a broad range of companies involved in uranium mining and in activities associated with the nuclear industry. Some of the companies I will cover are constituents of this index. For me, this demonstrates the company is at least on the radar of global investors seeking uranium exposure. In each company overview I will make note if the company is a “URA constituent”.

Companies List

Part 2 Uranium Companies: 92 Energy (92E), A-Cap Energy (ACB), Alligator Energy (AGE), Anson Resources (ASN), Aura Energy (AEE), Bannerman Energy (BMN), Berkeley Energia (BKY), Boss Energy (BOE), Deep Yellow (DYL), Devex Resources (DEV);

Part 3 Uranium Companies: Eclipse Metals (EPM), Elevate Uranium (EL8), Energy Metals (EME), Gladiator Resources (GLA), GTI Resources (GTR), Haranga Resources (HAR), Havilah Resources (HAV), Kopore Metals (KMT), Laramide Resources CDI 1:1 (LAM), Lotus Resources (LOT);

Part 4 Uranium Companies: Marmota (MEU), Nexgen Energy (Canada) CDI 1:1 (NXG), Okapi Resources (OKR), Paladin Energy (PDN), Peninsula Energy (PEN), Silex Systems (SLX), Thor Mining PLC CDI 1:1 (THR), Toro Energy (TOE), Valor Resources (VAL), Vimy Resources (VMY).

92 Energy (92E)

Last Price: $0.545 | Market Cap. $M: $38.5 million

Progress: No defined resource; Very early-stage exploration

URA constituent: No

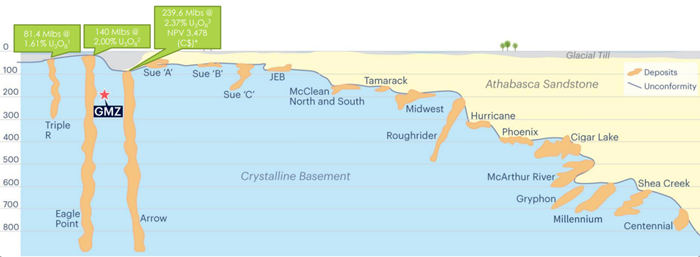

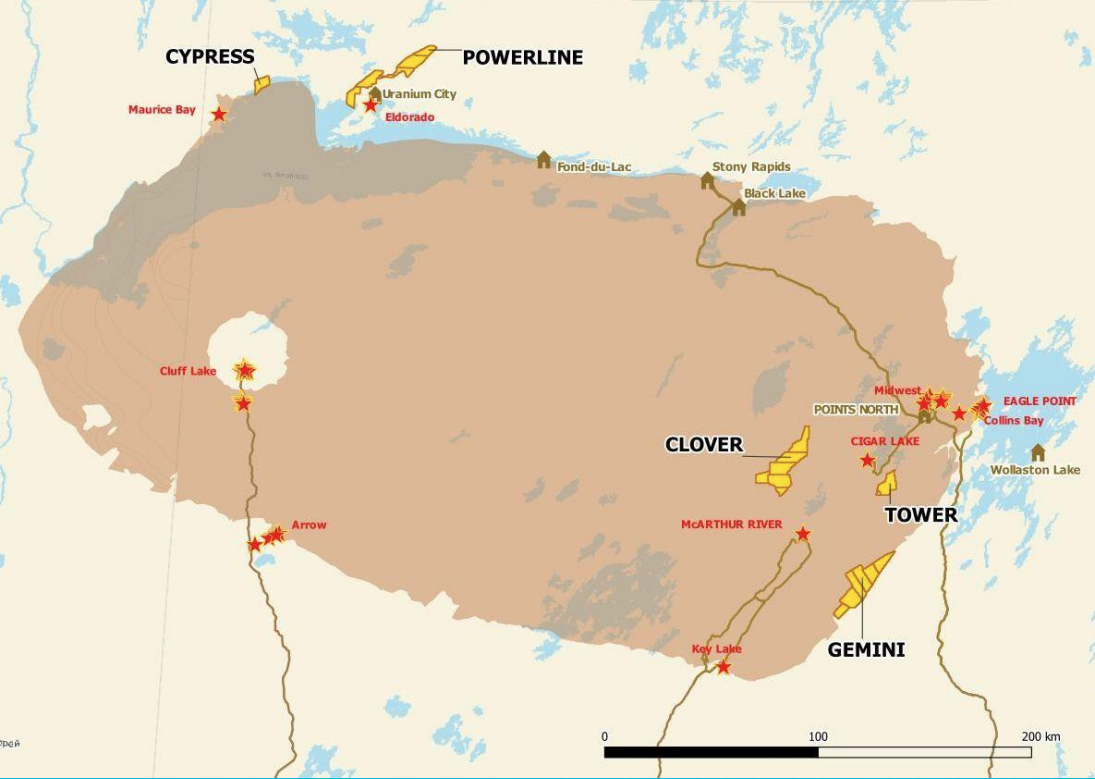

92 Energy is exploring for uranium in the Athabasca Basin, Canada. It is progressing five 100% owned projects within the area, but the company’s main focus is the Gemini Project (Gemini Mineralised Zone (GMZ)). Drilling at GMZ has returned anomalous radioactivity across 11 holes, with one of the holes returning 5.5m at 1200ppm U3O8 including 1.0m at 2800ppm U3O8. These are particularly high grade results. After receiving the results, 92 Energy pegged an additional 7 claims to expand the GMZ.

Schematic of Athabasca Basin uranium deposits, basement hosted versus unconformity, and position of Gemini Mineralised Zone (Source: 92 Energy)

Schematic of Athabasca Basin uranium deposits, basement hosted versus unconformity, and position of Gemini Mineralised Zone (Source: 92 Energy)

Elevated radioactivity at the GMZ has now been defined over a length of 230 metres in the northwest-southeast direction and 80 metres in the northeast-southwest direction. The best results are in a south-west direction and will be followed up with priority drilling in June 2022. The company believes potential exists for high-grade and volume upside.

(Source: 92 Energy)

(Source: 92 Energy)

In real estate, they say location, location, location. Firstly, GMZ is just 27km southeast of Cameco’s McArthur River Mine, which is considered by many to be the largest high-grade uranium deposit in the world. Then, consider 92 Energy is aiming to produce uranium from within North America. This is a major advantage over suppliers based outside of North America, potentially in less secure or less friendly (um, Russia!) jurisdictions. The U.S. is currently the world’s largest producer of nuclear power, and Canada also has considerable nuclear power production capabilities. Compare this to the U.S.’s uranium production – which is negligible. Therefore, if 92 Energy can prove an economically viable resource at any of their Athabasca Basin prospects, it would certainly be viewed as a strategically important resource by both the Canadian and US governments.

One fly in the ointment however is the company is running low on cash. Investors should note that as per its March quarterly update, 92 Energy had $6.5 million cash in the bank vs a cash burn of approximately $9 million per year – i.e., less than three quarters of cash remaining to fund its operations. So, expect a capital raising might be announced soon. On the plus side in the near term, 92 Energy is still awaiting the remaining chemical assays from its winter season drilling campaign. Ideally management would love to get the price up before doing a placement!

A-Cap. Energy (ACB)

Last Price: $0.089 | Market Cap. $M: $110 million

Progress: Defined resource; Very early mine feasibility

URA constituent: Yes

A-Cap’s flagship project is the Letlhakane Uranium Project in Botswana, host to one of the world’s top 10 undeveloped uranium deposits. A-Cap has idled the project for a number of years due to the low uranium price. Given the recent improvement in the uranium price, the company undertook a $10.7 million capital raising in February 2022 with a view to advancing the project.

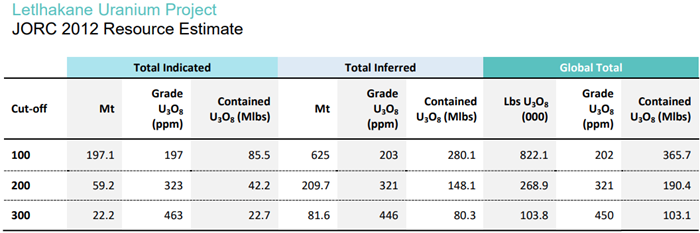

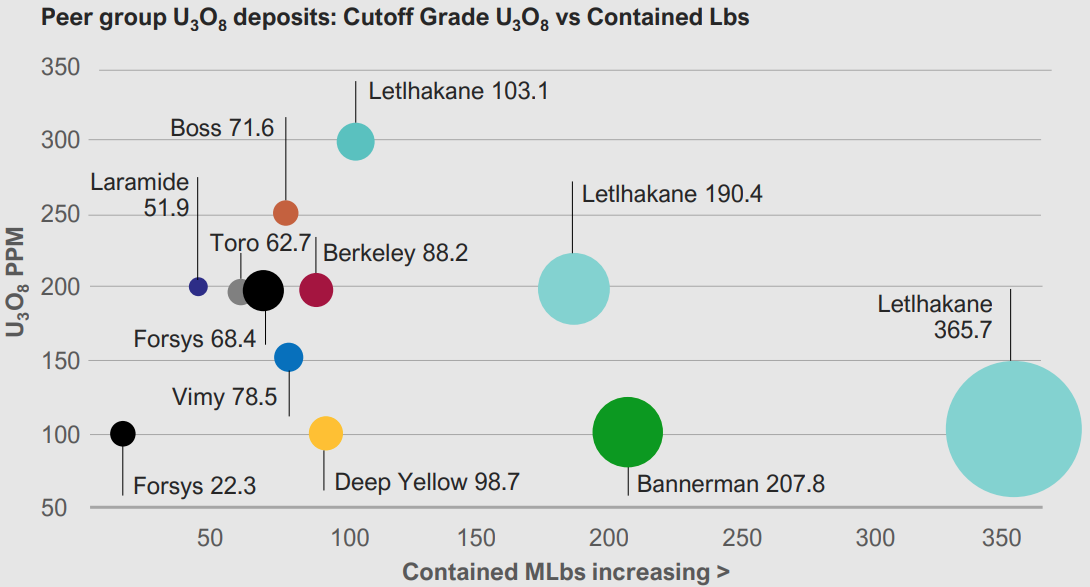

Botswana is a stable mining jurisdiction, arguably the most stable within Africa, with 40% of the country’s GDP derived from the resources sector. A-Cap hopes Letlhakane will become Botswana’s first producing uranium mine. It has a total JORC resource of 365.7 million pounds (822.1 Mt @ 202ppm U3O8 using a 100ppm cut-off grade). A Mining Licence was granted on 12 September 2016 and is valid for 22 years, and Letlhakane has environmental approval from the Botswana Department of Environmental Affairs. The proposed mine site is also within close proximity to major infrastructure including first class rail, roads, power and water.

Source: A-Cap Energy

Source: A-Cap Energy

The ore body at Letlhakane is flat, shallow, and is suited to low cost open pit mining using surface miners. A-Cap is presently devising a work program and budget which should be announced by the end of the June 2022 quarter. Apart from this, only very minor work is taking place, including ongoing water bore sampling and mining licence compliance. Further key personnel are being re-engaged to facilitate the restart of development activities on site.

Source: A-Cap Energy

Source: A-Cap Energy

A-Cap also has a nickel-cobalt project in Western Australia which contains a JORC total mineral resource of 660,000 tonnes of nickel and 46,400t of cobalt. The project appears to be of similar importance to the company as it’s uranium aspirations. As at March 31, A-Cap had $13 million cash in the bank vs a cash burn of approximately $1.3 million per year.

Aura Energy (AEE)

Last Price: $0.200 | Market Cap. $M: $96.4 million

Progress: Defined resource; Updated definitive feasibility study (DFS) complete; Potential production by 2024

URA constituent: Yes

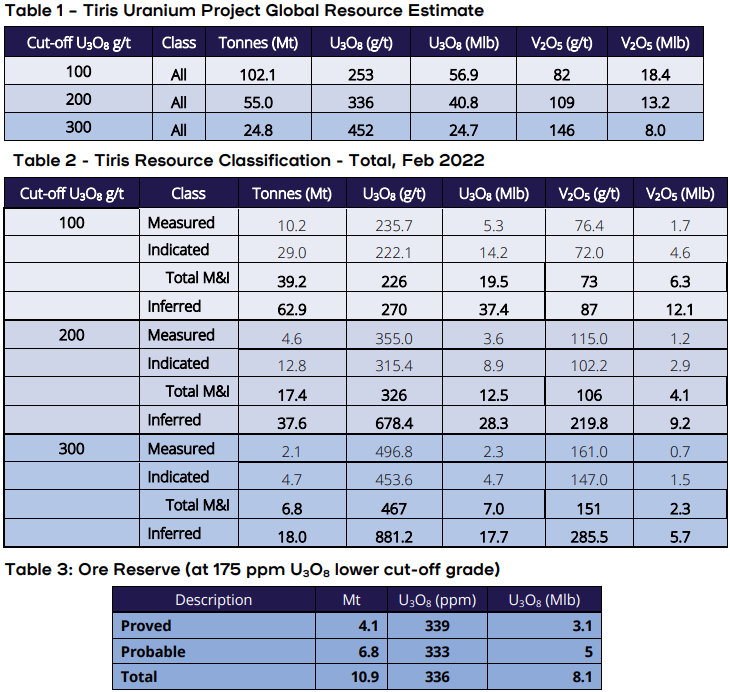

Aura is aiming to be in production at its flagship Tiris Uranium Project (85% owned) in Mauritania by 2024. Tiris contains a 56 million pound U3O8 resource (102.1Mt @ 253 ppm U3O8 using a 100 ppm cut-off grade), and as a kicker, it also contains 18.2 million pounds vanadium oxide (V2O5). Uranium and vanadium? Double rocket ship emojis 🚀🚀!

Source: Aura Energy

Source: Aura Energy

Mauritania is generally considered as a low-risk mining jurisdiction and hosts operations owned by major energy companies such as BP and Exxon Mobil. Tiris is within close proximity to existing infrastructure including ports, train lines, and direct road access.

Engineering studies have commenced at Tiris aiming to deliver a mine capable of producing of 800,000 pounds U3O8 in 2024, and then 1.25 million pounds per annum thereafter. The Tiris DFS published in 2019, and updated in 2021, proposed a 15 year life of mine (LOM) with an initial capital cost of $107 million to get to production, and a 4 year payback period. The ore body is extremely shallow (1-5 meters) which means only free digging is required to extract the ore (i.e., no drill and blast and no crushing or grinding). The C1 cash cost at Tiris is expected to be US$25.43/lb U3O8, for an All-In Sustaining Cost (AISC) of US$29.81/lb U3O8. This makes it a relatively low cost producer compared to the U.S. Energy Information Administration’s (EIA) most recent estimate of global uranium production costs of US$33.20 per pound.

Source: Aura Energy

Source: Aura Energy

There is potential to increase reserves and production at Tiris as the company is actively exploring areas where the mineralisation remains open. In April, Aura announced a programme which will re-evaluate exploration targets with the long-term goal of increasing both the uranium and vanadium Measured and Indicated Resource bases. An engineering study for vanadium production at the mine is occurring simultaneously with the uranium production works.

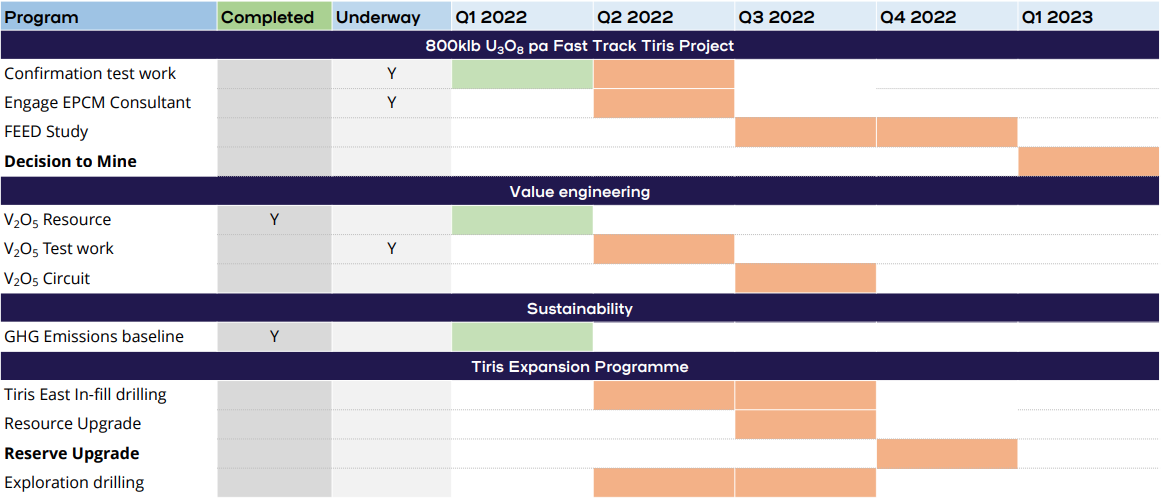

Tiris Uranium Project Timeline (Source: Aura Energy)

Tiris Uranium Project Timeline (Source: Aura Energy)

There’s plenty going on at Tiris at the moment, and it is reassuring Aura have a clear path to production. It’s also worth noting Aura has another uranium-vanadium project, the HÄGGÅN Project in Sweden, where they are at scoping study stage. It also owns a very early-stage gold project in Mauritania. As at March 31, Aura had $11 million cash in the bank vs a cash burn of approximately $2.5 million per year.

Alligator Energy (AGE)

Last Price: $0.068 | Market Cap. $M: $220 million

Progress: Defined resource; Scoping study/working towards pre-feasibility study (PFS)

URA constituent: Yes

Alligator has three uranium projects, two located in South Australia (Samphire Project and Big Lake Uranium Project), and the Alligator Rivers Uranium Province (ARUP) in the Northern Territory. The Samphire Project is the more progressed of the three, with only airborne electromagnetic (AEM) surveys conducted so far at Big Lake and ARUP. Alligator reports it has a 47 million pound inferred uranium resource (94.7 Mt @ 230ppm U3O8 using a 100ppm cut-off grade) at Samphrie spread across two deposits, Blackbush and Plumbush.

Source: Alligator Energy

Source: Alligator Energy

Assay results from the February drilling round are still trickling in and so far confirmed high-grade uranium over the anticipated intervals. The company will use these results to increase confidence in the re-estimation of the JORC compliant resource at Blackbush.

Both historical and recent drilling programs indicate the mineralisation at Blackbush is hosted within a geological zone amenable to in situ recovery (ISR). This is generally accepted to be a more cost effective and environmentally acceptable process of extracting the uranium compared to the traditional method of digging, crushing, dissolving and treating with chemicals.

Australian Nuclear Science and Technology Organisation (ANSTO) has commenced uranium leach and ion exchange (IX) extraction test work on the ISR-amenable uranium mineralisation from Blackbush. This work will broadly estimate expected extraction recovery. These results, in conjunction with a re-estimated JORC-compliant resource will form the basis for a Scoping Study Alligator expects to be completed by end of Q3, 2022.

Source: Alligator Energy

Source: Alligator Energy

Catalysts for Alligator going forward include further success from the final batch of assay results due at Blackbush, and in the medium term, a resource upgrade. It is fair to say though, the company is in the very early stages of development. Even if they can show they have an economically viable resource at Samphire, Alligator is unlikely to commence mining within the next few years. Alligator is well funded for their exploration activities however, with over $27 million cash in the bank, versus a cash burn rate of approximately $2 million per year.

Anson Resources (ASN)

Last Price: $0.120 | Market Cap. $M: $121 million

Progress: No defined resource; Very early stages exploration

URA constituent: No

Looking through Anson’s website and recent ASX announcements, it becomes very clear very quickly its uranium aspirations take second place to its lithium aspirations. They even call their Paradox Brine Project located in Utah their “core” project.

But, about 40 kms down the road is Anson’s Yellow Cat Uranium Project. It’s very, very early stages here. The last major work they did on Yellow Cat was back in September 2021 when they reported results they described as “Exceptional high-grade Uranium & Vanadium assays”, including up to 10.33% U3O8 & 25.61% V2O5.

The September results samples were taken from outcrops, ore pads, and exposed mineralisation. This type of sampling is very preliminary, and Anson is currently conducting an environmental survey in advance of a submission of an application to conduct a more targeted drilling campaign.

Interestingly, the company notes historical drilling results at Yellow Cat (which Anson acquired in 2019) of up to 0.3 feet @ 37,500ppm U3O8 & 3.34% V2O5. It’s also worth noting the district within which Yellow Cat sits did produce substantial amounts of uranium between 1935 and 1954. It’s also within trucking distance of White Mesa Mill – the only conventional fully licensed and operational uranium-vanadium mill in the US.

Were getting a little off topic here, but should Anson (eventually, as in really, really eventually) manage to get a mine up and running at Yellow Cat, it will no doubt be considered an important strategic resource by the US government. The U.S. is currently the largest consumer of uranium, yet domestic production is almost non-existent. In March a group of US Senators lead by John Barrasso (R-WY) introduced the National Opportunity to Restore Uranium Supply Services In America (NO RUSSIA) Act of 2022 (notice the NO RUSSIA bit!). The goal here is to “establish a national strategic uranium reserve … to ensure existing U.S. nuclear reactors have sufficient fuel to continue operating.”

Anson is running low on cash. Investors should note that as per its March quarterly update, the company had $8 million cash in the bank vs a cash burn of approximately $6 million per year – i.e., roughly only five quarters of cash remaining to fund its operations. So, expect a capital raising is announced within the next 6-12 months.

Berkeley Energia (BKY)

Last Price: $0.370 | Market Cap. $M: $165 million

Progress: Defined resource; Definitive feasibility study completed; Regulatory issues preventing construction of mine

URA constituent: Yes

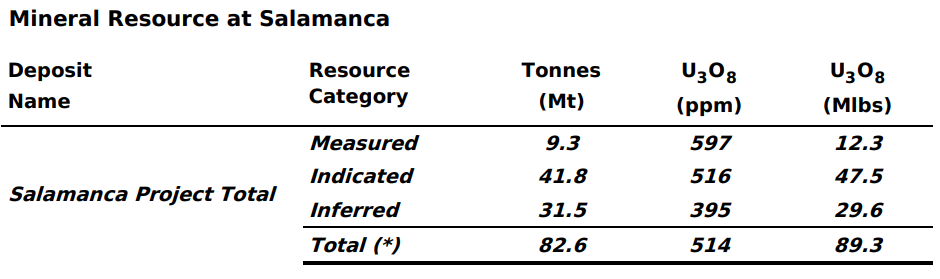

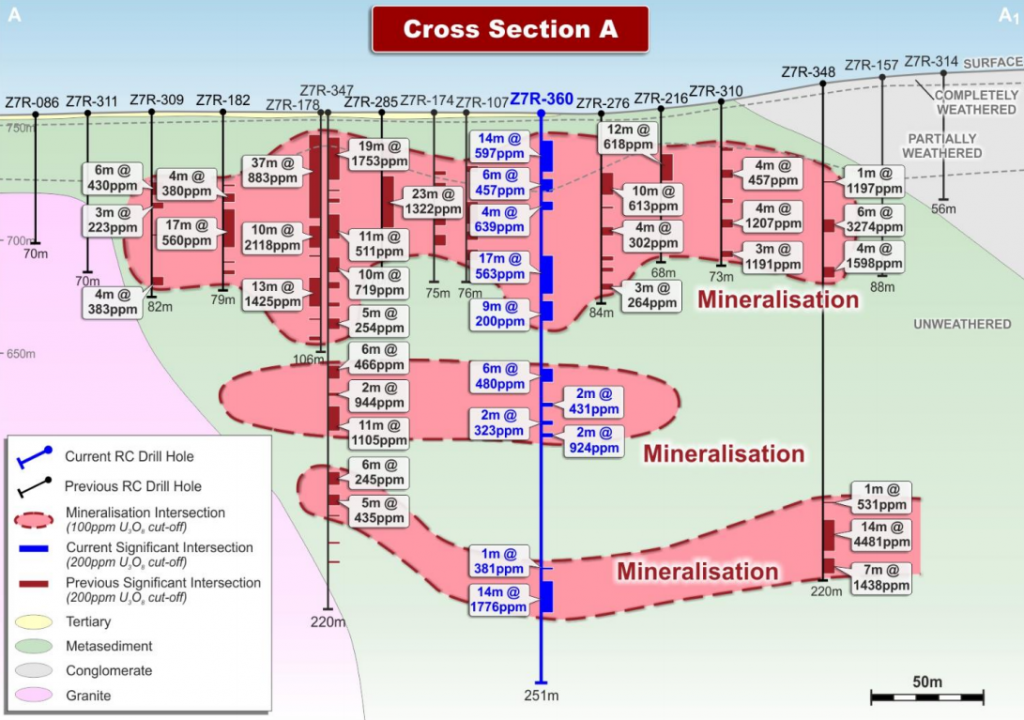

Unlike Anson, Berkley Energia is a uranium pure-play. They are in the process of developing their Salamanca Project in Western Spain, about three hours west of Madrid. Salamanca contains a mineral resource of 89.3 million pounds uranium (82.6 Mt @ 514 ppm U3O8). The project sits within an historic uranium mining area and is within close proximity to well established regional infrastructure.

Source: Berkeley Energia

Source: Berkeley Energia

Let’s consider Berkey Energia’s pros and cons:

Pro: The company’s 2016 Definitive-Feasibility Study showed Salamanca could be one of the world’s lowest cost producers, capable of producing an average of 4.4 million pounds of uranium per year at a total cash cost of US$15.06 per pound. At the time, they suggested the project had a net present value (NPV) of US$531 million with an internal rate of return of 60% based on a discount rate of 8%, and this assumed a uranium spot price of just US$20 per pound (and term contract price of US$41 per pound).

Pro: The project benefits greatly from the well-established EU funded infrastructure in the region, and has a low initial capital cost of only US$93.8 million (so far only very preliminary works have been undertaken and main construction is yet to occur).

Pro: The Company has $75 million in cash reserves as at the end of the March quarter vs a cash burn rate of approximately $5 million per annum, and no debt.

Pro: According to Berkely Energia, “Salamanca is being developed to the highest international standards and the Company's commitment to health, safety and the environment is a priority. The Company currently holds certificates in Sustainable Mining (UNE 22470-80), Environmental Management (ISO 14001), and Health and Safety (ISO 45001) which were awarded by AENOR, an independent Spanish government agency.”

Con: In 2021, the Company received formal notification from the Ministry for Ecological Transition and the Demographic Challenge ("MITECO") in Spain that it had rejected the Authorisation for Construction for the uranium plant as a radioactive facility ("NSC II") application at Salamanca. This decision followed the unfavourable NSC II report issued by the Nuclear Safety Council ("NSC") in July 2021.

Result: the project sits in limbo as Berkely Energia appeals the decision under Spanish Law. Just…one…permit…away…Messy, messy, messy!

Perhaps though, recent events in Ukraine might work in Berkeley Energia’s favour. Salamanca is on the doorstep of Europe’s nuclear reactor fleet, and like the U.S., the EU doesn’t have any uranium supply of its own. Worse still, most their current requirements are imported from Kazakhstan, and you guessed it, Russia! With gas and coal prices soaring across the Continent, causing a number of EU countries to rethink their post-Fukushima pivot away from nuclear, and with energy security now a top priority for governments, Salamanca is potentially in the right place at the right time.

Salamanca Project Cross Section (Source: Berkeley Energia)

Salamanca Project Cross Section (Source: Berkeley Energia)

Assuming Berkely Energia can sort the mess out, the company indicates their next steps are:

• Advance the Salamanca mine through the development phase into the main construction phase and then into production;

• Progress with seeking further offtake partners. Berkely Energia has maintained its preference to combine fixed and market related pricing across its contracts in order to secure positive margins in the early years of production whilst ensuring the Company remains exposed to potentially higher prices in the future; and

• Assess other mine development opportunities at Salamanca

As at March 31, Berkeley Energia had $75 million cash in the bank vs a cash burn of approximately $5.5 million per year. So, even if they get past their (looks to me substantial!) regulatory hurdles, they’re not going to have enough capital to fund the construction at Salamanca from cash. This means a modest capital raising or a debt undertaking (or a combination of both) somewhere down the track.

Still, the NPV stated in that 2016 DFS looks interesting, especially considering current spot prices are more than double the spot priced used in the calculations. Compare the NPV estimate of US$531 million to the company’s enterprise value (i.e., market cap plus debt, minus cash) of roughly $100 million, and potentially there’s an opportunity here. But, if there’s never going to be a mine at Salamanca…then what!?

Bannerman Energy (BMN)

Last Price: $0.190 | Market Cap. $M: $283 million

Progress: Defined resource; Aiming to complete DFS in Q3 2022

URA Constituent: Yes

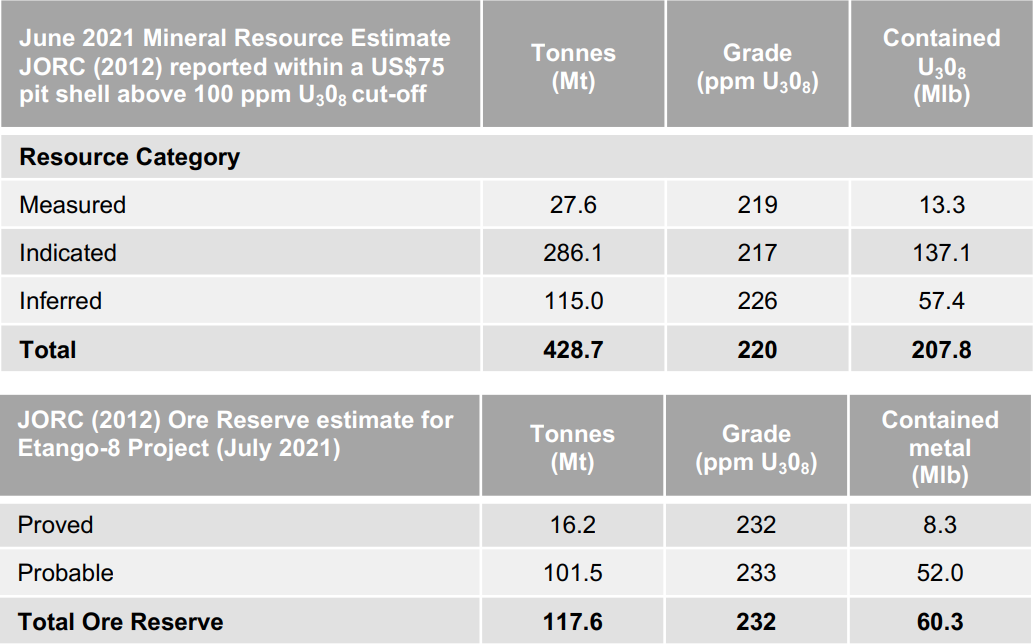

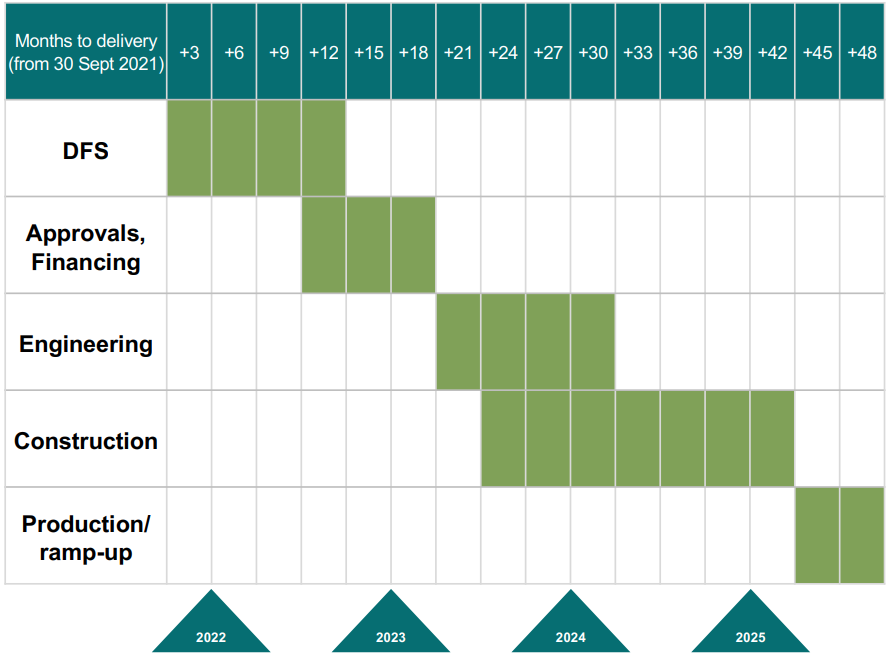

Bannerman Energy is working towards completion of a Definitive Feasibility Study (DFS) at their Etango-8 project in Namibia. The DFS will draw upon extensive work the company has done at the project over the last 15 years, and the 2021 Pre Feasibility Study (PFS). It will include designs for the process plant and related infrastructure, along with plant capital and operating cost estimates. The company expects the DFS will be completed by the September quarter, but is also progressing Front-End Engineering and Design (FEED) and detailed design, product marketing, and project financing activities.

Bannerman claims the Etango Project is “one of the world’s largest undeveloped uranium deposits”. It is located in the Erongo uranium mining region of Namibia which hosts a number of large uranium mines including Rössing, and Langer-Heinrich (Paladin Energy). Etango is very close to sound infrastructure including road, rail, electricity, water, and one of southern Africa’s busiest deep-water ports through which uranium has been exported for over 40 years.

Etango-8 is part of the broader Etango project which (according to the PFS) contains 207.8 million pounds uranium (428.7 Mt @ 220 ppm U3O8 with a cut-off grade of 100ppm). The company sees Etango-8 at the quickest path to production, with scalability options down the track. The initial goal of 3.5 million pounds production from Etango-8 could potentially be scaled to 7.2 million pounds in the future.

Etango (top) and Etango-8 (bottom) Resources and Reserves (Source: Bannerman Energy)

Etango (top) and Etango-8 (bottom) Resources and Reserves (Source: Bannerman Energy)

According to the PFS, Etango-8 contains 60.3 million pounds uranium (117.6 Mt @ 232 ppm U3O8 with a cut-off grade of 100ppm). At the initial production goal of 3.5 million pounds per annum Bannerman expects a 15 year mine life. The mining method is conventional, and therefore has low technical risk. The PFS claims a NPV of US$222 million for Etango-8, but this assumes a uranium price of US$65 per pound over the life of the mine – a pretty big assumption considering where the price is now! Having said this, Bannerman predicts that the project will be highly leveraged to the uranium price, with a 10% increase yielding a 47% increase in the NPV.

Etango-8 Project Timeline (Source: Bannerman Energy)

Etango-8 Project Timeline (Source: Bannerman Energy)

Just checking on the company’s current cash balance, adding in the recent capital raising it had around $61 million cash in the bank at the end of the March quarter, versus a cash burn rate of approximately $2.5 million per year. So, whilst Bannerman has plenty of funding to get to a Final Investment Decision (FID) (i.e., go-no-go) at Etango-8, given the PFS estimate of US$274 million for pre-production capital expenditure (“capex”), it will need to secure substantial additional funding to get to mine. FYI, the PFS suggests a payback period of 3.8 years.

Boss Energy (BOE)

Last Price: $2.12 | Market Cap. $M: $748 million

Progress: Defined resource; Enhanced feasibility study (EFS) complete, now awaiting final investment decision; Production expected approx. 2024

URA Constituent: Yes

Boss is aiming to become Australia’s next uranium producer at its flagship Honeymoon Uranium Project in South Australia. Boss acquired Honeymoon in 2015 as a brownfield project which at the time was on care and maintenance due to the low uranium price.

The company has just completed a FEED study which confirmed the cost estimates in the Enhanced Feasibility Study (EFS). This is all just jargon for “Boss is a long ways down the track and not kicking over rocks in the desert anymore!”. Boss will get to mine (uranium price permitting!), it’s just a matter of when. The “when” will be determined by the FID, which the company indicated in its ASX release on 31 March would occur: “after completion of the Tranche 2 Placement on or around 5 May 2022, whereupon the company will immediately commence with detailed engineering, procurement and construction works.” At the time of writing, whilst the Tranche 2 placement is completed, there hasn’t been an announcement regarding the FID. We are going to assume this is not because of the recent dip in the uranium price, and a FID remains a mere formality!

Post-FID, the next step is to secure long term binding offtake agreements. This should be made easier given Honeymoon is located in Australia which is considered to be stabile jurisdiction with excellent access to secure and reliable transportation. These factors are particularly attractive to nuclear power utilities who value reliability of supply.

Honeymoon Resource Lower Cut-Off 250ppm (Source: Boss Energy)

Honeymoon Resource Lower Cut-Off 250ppm (Source: Boss Energy)

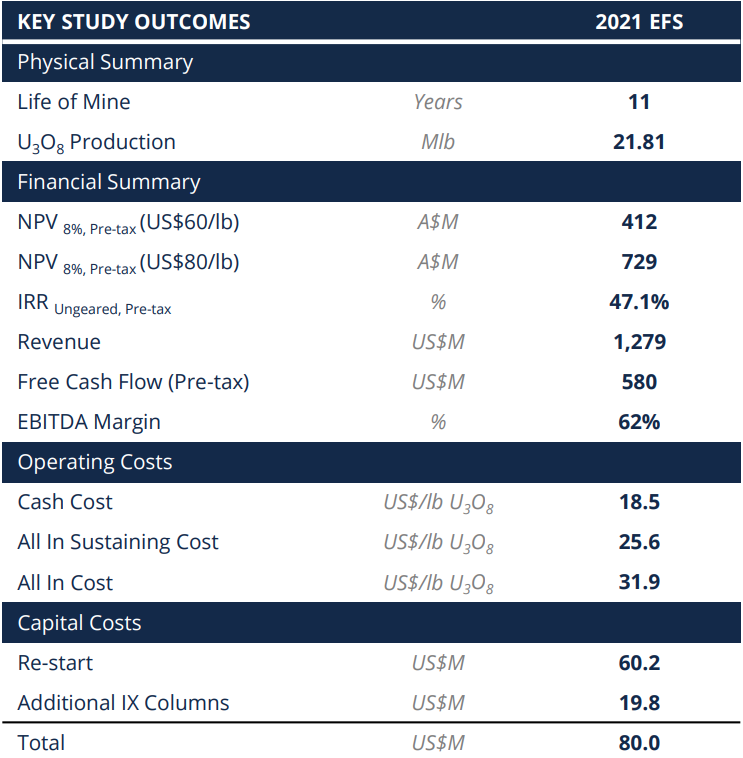

Honeymoon contains 71.6 million pounds of uranium (52.4 Mt @ 620ppm U3O8 with a cut-off grade of 250ppm) which means it’s relatively small compared to some of the deposits we’re going to discuss – but it is very high grade. Boss’s goal is to produce 2.5 million pounds U3O8 per annum within 3-4 years. They plan to use the ISR mining method which is expected keep operating costs towards the bottom end of the current global production price range. To put it into perspective, Honeymoon’s LOM average AISC is expected to be US$25.60 per pound compared to the U.S. Energy Information Administration’s most recent estimate of global uranium production costs of US$33.20 per pound. There is significant upside potential beyond the expected initial 11-year mine life, with approximately 50% of the Honeymoon resource yet to be incorporated.

Honeymoon EFS Financial Highlights (Source: Boss Energy)

Honeymoon EFS Financial Highlights (Source: Boss Energy)

Boss estimates that Honeymoon will cost US$80 million to construct and could be up and running within 18 months from commencement. So, assuming we get that FID soon, we’re talking 2024 as the earliest for production and subsequent cashflow. Note however, Boss is fully funded and permitted through to this point (compare to others in this list!) – and this is a major positive for shareholders. Also, watch out for those NPV’s. Similar to Bannerman, there’s quite a bit of upside assumed in the uranium price, but also substantial leverage if it really gets going.

In terms of cashflow, this in theory could occur earlier if Boss decides to capitalise on its 1.25 million pound stash of U308 which acquired in March 2021 when the uranium price was in the doldrums. This as it turns out was a wise and prophetic purchase! The value of Boss’s uranium holdings has since doubled to US$95 million.

As mentioned above, Boss also has significant potential to expand the resource base at Honeymoon via exploration. But, there’s also potential to incorporate existing Resources at nearby Gould’s Dam 25 million pounds (22.1 Mt @ 514ppm U3O8) and Jason’s 11Mlb (6.2Mt @ 790ppm U3O8) deposits into a LOM extension. Both projects are within pumping distance of Honeymoon’s processing infrastructure. In terms of exploration, based upon other targets identified within the Honeymoon Project area, Boss believes they could unlock anywhere between 58 – 190 million pounds of extra uranium resources at grades up to 1,080ppm.

As at March 31, Boss had $106 million cash in the bank with a further $28 million due from a recent placement in April. This compares to a cash burn of approximately $5 million per year.

Devex Resources (DEV)

Last Price: $0.385 | Market Cap. $M: $121 million

Progress: No defined resource; Very early stages exploration

URA constituent: No

Devex has a few irons in the fire, of which the Nabarlek Uranium Project in the Northern Territory is one of them. However, I’m not sure how high up the list its uranium aspirations are. Certainly, looking at the last few Devex quarterly activity reports, their Sovereign Nickel-Copper-PGE Project in Western Australia and their Junee Copper-Gold Project in NSW, appear to be where their focus is in the short term at least.

The Nabarlek Uranium Project is based upon the historical Nabarlek mine which operated for a short period in the late 1970’s and early 1980’s. It produced 24 million pounds at a grade of 1.84% U3O8. Eventually, the resource was exhausted, and mining ceased.

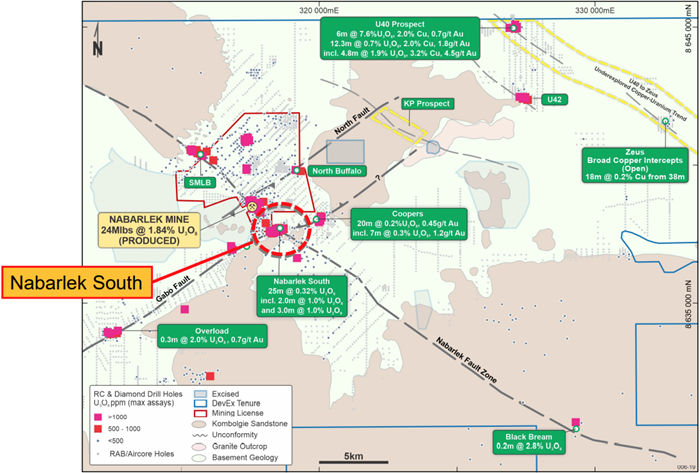

Nabarlek Uranium Project (Source: Devex Resources)

Nabarlek Uranium Project (Source: Devex Resources)

Devex intends to explore a number of untested radiometric anomalies adjacent to, and in the area surrounding, the historic mine. The Nabarlek South Prospect 1 km to the south of the old pit is of particular interest, as historic drilling identified a cluster of high-grade uranium intercepts which Devex believes could define “a north-east plunging uranium shoot”. Devex has identified Nabarlek South as a “priority drill target”, along with targets around the old pit edge, and the Zeus and U40 prospects to the north east.

The company’s March update indicates 18,000m of RC and diamond drilling is planned at Nabarlek to test such targets, and a drilling contractor has been secured with a rig expected to be mobilised in late June/July.

Devex claims a “Highly credentialed team assembled with real uranium exploration and development experience”. Perhaps! But one name on the Devex bench which might catch your attention is WA mining royalty Tim Goyder (Chalice Gold Mines (CHN), Liontown Resources (LTR), and Strike Energy (STK) among others). Even more interesting, in April, Mr Goyder purchased 1 million Devex shares for a consideration of $472,424. Yes, that’s only pocket money for him, but it’s always nice to see a director buying shares. It's even better when more than one director buys. Two other non-executive directors purchased approximately $200,000 between them around the time of Mr Goyder’s purchase.

Devex is another company which appears to be running low on cash however. As at March 31, it had $10 million cash in the bank vs a cash burn of approximately $10 million per year. Thus, expect a capital raising is announced within the next 6 months!

Deep Yellow (DYL)

Last Price: $0.71 | Market Cap. $M: $275 million

Progress: Defined resource; PFS complete; Working towards DFS due late 2022

URA constituent: Yes

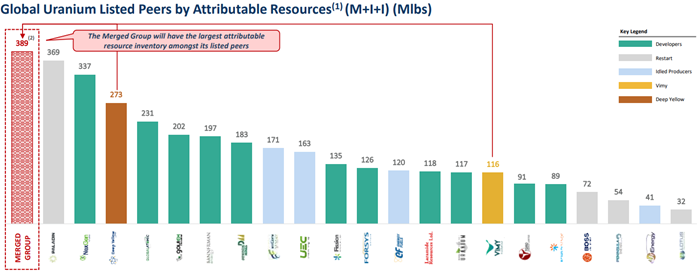

One can’t discuss Deep Yellow without first addressing its proposed merger with fellow uranium hopeful Vimy Resources (VMY). In March, the two companies agreed to a $658 million merger by scheme of arrangement under which Deep Yellow will acquire 100% of Vimy’s shares on issue. According to the marketing, the combined entity will have the largest resource base of any ASX listed uranium pure-play.

Source: Deep Yellow

Source: Deep Yellow

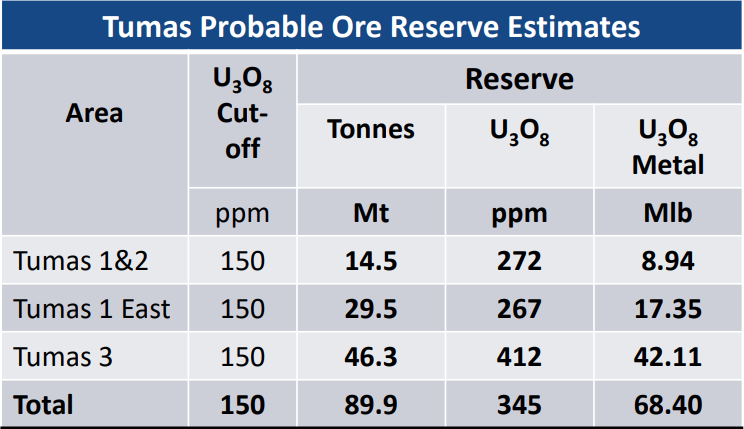

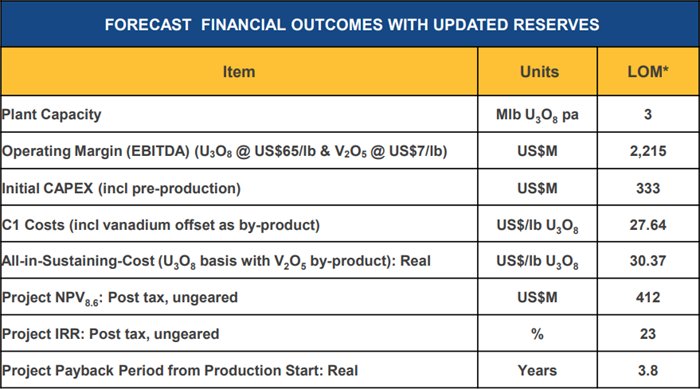

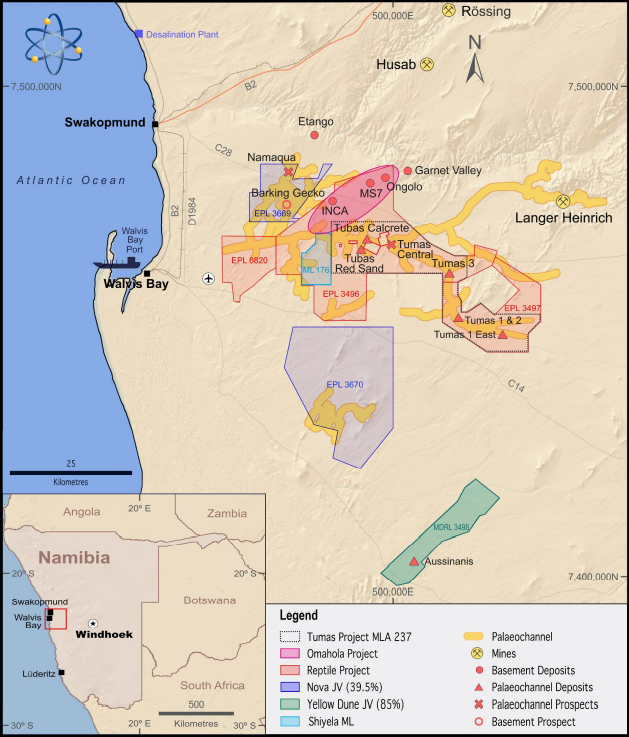

Deep Yellow’s flagship project is the 68.4 million pound reserve (89.8 Mt @ 345ppm U3O8 using a 150ppm cut-off grade) Tumas Project in Namibia. The company notes 40% of the Tumas paleochannel remains to be tested, which it expects allows for potential future upgrades of the resource base. Target production at Tumas is 3 million pounds per annum over a 26 year mine life at an AISC of US$30.37. The NPV of the project assuming a uranium price of US$65 per pound is US$412 million.

In its March quarterly update, Deep Yellow proposed the Tumas DFS is “firmly on track”. In it, the company aims to improve upon the PFS assumptions and solidly upgrade the economics of Tumas with a view to progressing the project towards production. Deep Yellow expects to complete the DFS in the 2022 December quarter. Thus far, the company expects a mine at Tumas will cost around $US320 million, which equates to a payback period of approximately 4 years.

Source: Deep Yellow

Source: Deep Yellow

Deep Yellow’s Tumas Project staff are largely picked from Paladin Energy’s Langer Heinrich mine team which got that mine up and running pre-Fukushima. Indeed, Deep Yellow notes that the Tumas deposit is very similar to nearby Langer Heinrich, and therefore is well understood by their current team.

Deep Yellow’s next major uranium asset is the Omahola Basement Project, also in Namibia. It has a measured, indicated and inferred resource base of 125 million pounds (298 Mt @ 190ppm U3O8 with a cut-off grade of 100ppm). Omohola sits within a prospective zone of 50km of folded strike length, of which only 15km has been adequately tested. A recent drilling campaign identified three highly promising targets, each marked for follow up drilling later this year.

Source: Deep Yellow

Source: Deep Yellow

We’ll discuss Vimy’s major contributions to the merger, including their flagship Mulga Rock Project near Kalgoorlie and their Alligator River Project in the Northern Territory in a later Part of this article. For now, it’s worth noting Mulga Rocks is a 90.1 million pound (71.2 Mt @ 570ppm U3O8 using a cut-off grade of 150ppm) resource. Vimy is well advanced on the project, working on a revised DFS/Bankable Feasibility Study (BFS) with scopes of work and recruitment of key project personnel proceeding. Production is expected by 2025.

Source: Deep Yellow

Source: Deep Yellow

According to Deep Yellow and Vimy, combining the two companies puts them at the top of the heap in terms of attributable resources compared to their peers. Note, by “peers” they mean everyone except mega producers “such as Cameco and Kazatomprom”!

As at March 31, Deep Yellow had $69 million cash in the bank vs a cash burn of approximately $2.2 million per year.

Learn More, Earn More!

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.