A snapshot of overnight moves and a look to the upcoming Australasian session for 18 September.

Market Moves

Wrap

US markets rose stumbled again as tech stocks faltered, and investors reacted negatively to a number of key economic data releases.

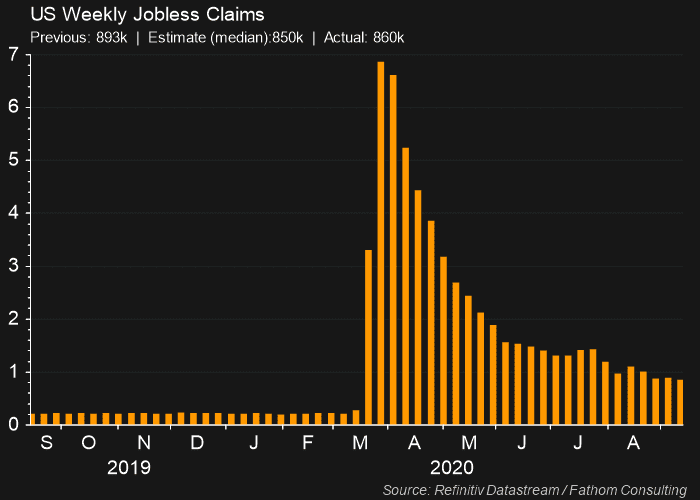

Weekly jobless claims showed that the number of Americans filing for unemployment benefits continues to remain at disturbingly high levels. Additionally, other data showed a slowing in recent strength in the US housing sector and US business activity.

The generally negative sentiment saw the tech-heavy NASDAQ pace losses, it closed down 1.27%, while the benchmark S&P500 fell 0.84%, and the blue chip-laden Dow Jones Industrial Index lost 0.47%.

Metals prices on the LME were mixed. Copper and Lead eked out small gains, whilst the rest were as much as 1% lower. Copper also saw a 0.48% gain in New York.

Iron Ore prices are 1.32% higher in early trading on the Chinese Dalian Exchange, as prices recovered tentatively from their largest 2-day plunge this year. Iron ore was 0.19% higher in the Singapore-based $US price.

Looking at precious metals, Spot Gold had a weaker session. It fell 0.67% to US$1945.60/oz, whilst Silver lost 0.50% to US$27.07/oz.

Crude oil commodities were once again the super stars of the trading session. West Texas Crude added 1.85% to US$41.03/barrel and Brent gained 2.20% to US$43.77/barrel. Elsewhere though, Natural Gas tumbled 14.63%.

In currency moves, the Australian Dollar improved 0.16% to 0.7317 as the US Dollar Index declined 0.26%.

Risk off bonds were higher, with the yields on the US 10 year Treasury Notes falling 1.5bp to 0.693%.

So, with few clear leads in terms of risk on and risk off assets overnight, where did the ASX200 Share Price Index end up? Well, it had a reasonably robust session, closing at 5880 compared to an overnight session high of 5898 and a low of 5838.

That's a 3.2 point discount to yesterday's ASX 200 close of 5883.2, and predictive of approximately a 0.1% rise at the open for the S&P ASX200.

AU Companies

Clover Corporation (CLV)

This morning the company reported that net profit after tax improved 15% to $88.3m on a 23.6% increase in revenues. Sales of new products were the key driver of profit growth as shoppers stockpiled groceries during and after the Covid-19 pandemic.

Clover noted that all markets and segments saw growth, particularly infant formula. They warned that the ongoing impact of the pandemic was uncertain, but the company continued to work through near and long term issues and remained well placed for continued growth.

Ex-Dividend Stocks

AMP (AMP) $0.10 fully franked.

Base Resources (BSE) $0.035 unfranked.

Qube Holdings (QUB) $0.023 fully franked.

Broker Moves

| Nanosonics |

NAN |

Goldman Sachs initiates neutral rating on Nanosonics (NAN). Initiates $5.50 price target. |

| News Corporation |

NWS |

Goldman Sachs retains buy rating on News Corporation (NWS). Retains buy rating. |

| RIO Tinto |

RIO |

JP Morgan upgrades RIO Tinto (RIO) rating from neutral to overweight. |

| RIO Tinto |

RIO |

Barclays upgrades RIO Tinto (RIO) rating from underweight to equalweight. |

Macro Economy

It is a quiet day for local and Asian economic data, but later this evening, we'll see data on the US current account, US leading indicators, and the University of Michigan Consumer Sentiment Survey.

Below is a summary of the key macroeconomic data releases from the past 24 hours.

USA

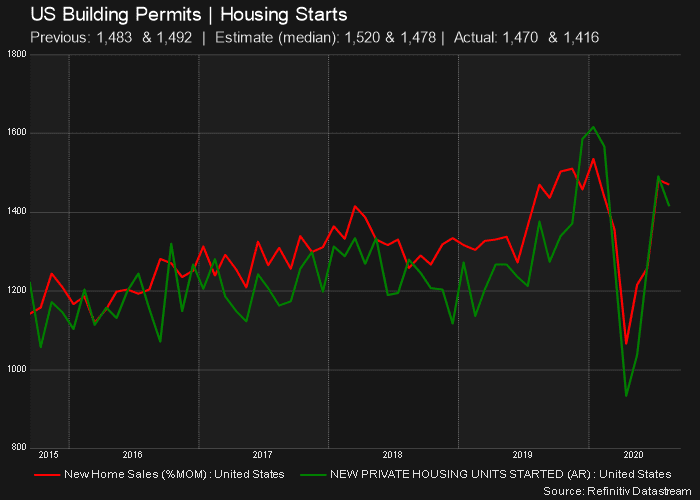

Housing building permits and starts both grew at a slower rate in August compared to July. Markets were expecting another solid gain for permits, and a small decline in starts. The actual numbers missed on both counts.

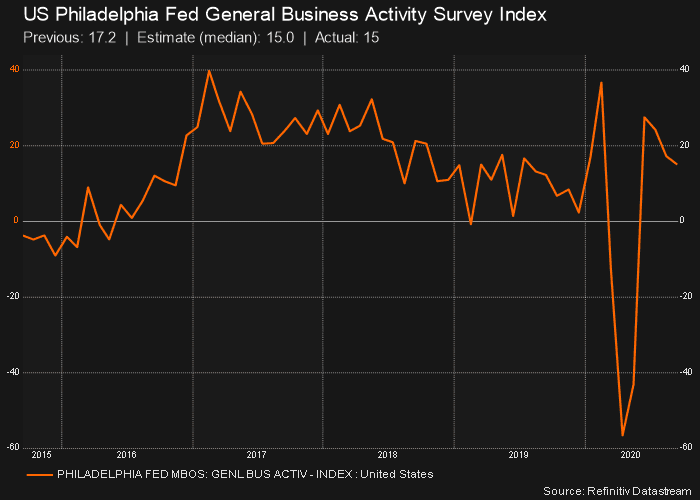

Philidelphia Fed business activity survey declined slightly in August from July, but remained in positive territory.

Weekly unemployment claims remained stubbornly high, and missed expectations slightly.