A snapshot of overnight moves and a look to the upcoming Australasian session for 21 September.

Market Moves

Wrap

US markets stumbled again as investors sold down key tech names like Apple Inc (-3.2%), Microsoft (-1.2%), Amazon (-1.8%), and Alphabet (-2.4%). Not even positive data on consumer sentiment (see Macro Economy) could stave off a third straight day, and a third straight week of losses.

The benchmark S&P500 fell 1.12%, whilst the tech-heavy NASDAQ was down 1.07%, and the blue chip-laden Dow Jones Industrial Index dipped 0.88%.

Metals prices on the LME ignored risk-off leads from stocks to close higher on the session. Zinc's gain of 1.34% was the best, whilst most other metals were up to 1% higher. Nickel was the only metal to miss out, it fell 1.73%. Copper also saw a 0.76% gain in New York.

Iron Ore prices continued to recover some of their lost ground for the week. The January contract on the Chinese Dalian Exchange is currently 1.24% higher in early Shanghai trading, whilst the Singapore-based US$ denominated September contract rose 0.54% to US$126.42/t.

Looking at precious metals, Spot Gold rose 0.18% to US$1949.50/oz, whilst Silver lost 1.43% to US$26.70/oz.

Energy commodities were mixed. West Texas Crude dipped 0.79% to US$40.73/barrel, Brent gained 0.25% to US$43.38/barrel, and Natural Gas rebounded 4.37% higher from Thursday's 14% fall.

In currency moves, the Australian Dollar retreated 0.33% to 0.7292 as the US Dollar Index edged 0.05% lower.

Interestingly, risk off bonds were also lower, with the yields on the US 10 year Treasury Notes rising 1bp to 0.701%.

So, with many risk on and risk off asset price movements at odds with traditional expectations, where did the ASX200 Share Price Index end up? Well, it had a lacklustre session, closing at 5836 compared to an overnight session high of 5882 and a low of 5802.

That's a 28.5 point discount to yesterday's ASX 200 close of 5864.5, and predictive of approximately a 0.5% fall at the open for the S&P ASX200.

AU Companies

Ex-Dividend Stocks

Adbri (ABC) $0.048 fully franked

Briscoe Group Australasia (BGP) $0.083 unfranked

Broker Moves

| Bluescope Steel |

BSL |

Citi raises Bluescope Steel (BSL) price target from $13.00 to $13.60. Retains neutral rating. Cites improving steel spreads in the US, upgrades Fy21 earnings forecasts by 19%. |

| City Chic Collective |

CCX |

EL&C Baillieu lowers City Chic Collective (CCX) price target from $3.70 to $3.50. Retains buy rating. Broker believes co. is well positioned to deliver strong growth in the medium term, but is disappointed by news it has missed out on Catherines acquisition. |

| Iluka Resources |

ILU |

Goldman Sachs lowers Iluka Resources (ILU) price target from $10.20 to $10.10. Retains buy rating. Blames delays in South Flank ramp up, says likely to have -13% impact on FY21 earnings. |

| James Hardie Industries |

JHX |

Goldman Sachs raises James Hardie Industries (JHX) price target from $37.23 to $37.35. Retains buy rating. Predicts earnings risks are skewed to the upside due to strong performance in US. |

| Nufarm |

NUF |

Citi retains buy rating on Nufarm (NUF). Retains $5.60 price target. Anticipates market will rerate European performance. |

Macro Economy

It will be a quiet day for economic data today, but later this evening, markets will focus on a speech from US Federal Reserve Chairman Jerome Powell.

Below is a summary of the key macroeconomic data releases from Friday's US trading session.

USA

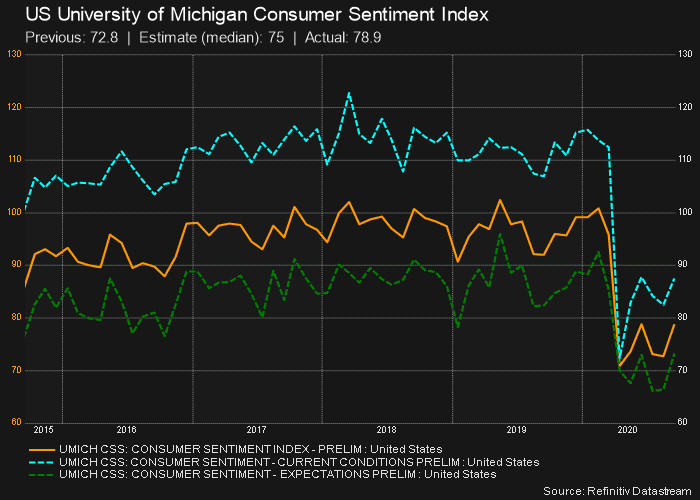

The University of Michigan’s consumer sentiment index rose to 78.9 in September from 74.1 in August. This was ahead of market expectations for a print of 75 points. It is the highest level for the index since March, but the index remains some 22 points below February's pre-pandemic high.

The Current Economic Conditions sub-index rose 4.6 points to 87.5, whilst the Consumer Expectations sub-index improved to 5 points to 73.5.

According to Richard Curtin, chief economist for the survey, the improvement in sentiment was primarily driven by consumers feeling more confident in their outlooks. He also noted that the upcoming US Presidential election was polarising confidence amongst respondents, with Democrats voters feeling more confident about their outlook than Republican voters.

Back