A snapshot of overnight moves and a look to the upcoming Australasian session for 25 September.

Market Moves

Wrap

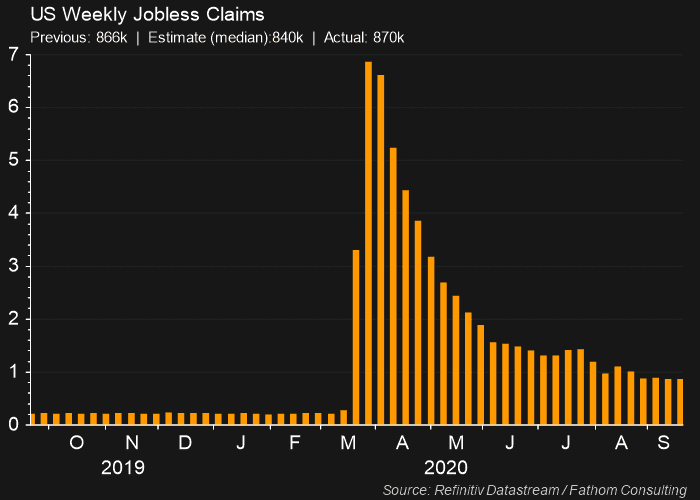

US markets edged higher as investors cheered better than expected news on the US housing market. The upside was tempered however, by a worse than expected report on weekly jobless claims.

The tech-heavy NASDAQ paced gains, it closed up 0.37%, while the benchmark S&P500 rose 0.30%, and the blue chip-laden Dow Jones Industrial Index gained 0.20%.

Metals prices on the LME were once again mixed. Aluminium, Copper, Lead and Nickel were each as much as 0.5% lower, whilst Tin dropped 1.49%, and Steel and Zinc eked out small gains. Copper saw a 0.87% gain in New York.

Iron Ore prices are 0.3% lower in early trading on the January 2021 contract on the Chinese Dalian Exchange, but are 0.5% higher on front the month contract. Data showed that Chinese steel production rose 8.4% in August, powering a global increase of 0.6%. Iron ore was 0.27% higher to US$123.29/t in the Singapore-based price.

Looking at precious metals, Spot Gold bounced 0.68% to US$1866.64/oz, whilst Silver gained 3.93% to US$23.15/oz.

Energy commodities were also higher. West Texas Crude added 1.96% to US$40.26/barrel, Brent gained 0.60% to US$42.46/barrel, whilst and Natural Gas was 0.23% higher.

In currency moves, the Australian Dollar retreated another 0.21% to 0.7052 as the US Dollar Index declined 0.04%.

Risk off bonds were slightly higher, with the yields on the US 10 year Treasury Notes falling 0.9bp to 0.669%.

So, with few clear leads in terms of risk on and risk off assets overnight, where did the ASX200 Share Price Index end up? Well, it had a comparatively robust session, closing at 5862 compared to an overnight session high of 5887 and a low of 5832.

That's a 13.9 point premium discount to yesterday's ASX 200 close of 5875.9, and predictive of approximately a 0.1% rise at the open for the S&P ASX200.

AU Companies

Ex-Dividend Stocks

Atlas Arteria (ALX) $0.11 unfranked.

Regis Resources (RRL) $0.08 fully franked.

Broker Moves

| AUB Group |

AUB |

Macquarie raises AUB Group (AUB) price target from $16.80 to $17.53. Retains outperform rating. Reacts positively to recent profit guidance by the co. |

| Brickworks |

BKW |

Citi raises Brickworks (BKW) price target from $20.95 to $19.00. Retains buy rating. |

| Brickworks |

BKW |

Macquarie raises Brickworks (BKW) price target from $17.80 to $18.80. Retains outperform rating. Broker is impressed with co's FY20 results. |

| Computershare |

CPU |

Citi retains sell rating on Computershare (CPU). Retains $12.00 price target. Anticipates lower margins due to the current low interest rate environment. Profits could drop by over 10% in FY21 before recovering strongly in FY22. |

| Insurance Australia Group |

IAG |

Morgan Stanley lowers Insurance Australia Group (IAG) price target from $6.65 to $6.50. Retains overweight rating. |

| Oceanagold Corporation |

OGC |

Macquarie lowers Oceanagold Corporation (OGC) price target from $3.90 to $2.80. Retains outperform rating. Blames higher than expected costs. |

Macro Economy

It's a quiet day on the local economic data front, but later this evening, we'll see data on US Durable Goods Orders.

Below is a summary of the key macroeconomic data releases from the past 24 hours.

USA

The weekly jobless claims report showed 4k more Americans claimed unemployment benefits last week. The total of 870k for the week of September 19 was significantly worse that expectations of a decline from the previous week's 866k to 840k.

On an encouraging note, continuing claims fell to 12.58m from 12.75m, but this was below expectations for a 12.28m print. Also, the total number of people claiming unemployment benefits dropped to 26.04m from 29.77m.

-United-States.png.aspx)

Newly built homes changed hands at their highest rate in 14 years in August, according to data from the National Homebuilders Association. 1.011m houses were sold, well up on the prior month's 965k sales, and well ahead of expectations of a print of 895k sales.

The increase in sales came as builders’ supply dropped to just 3.3 months’ sales, and sellers were offering around 400k fewer existing homes to the market.