In this post, we’re going to discuss the Top 3 ASX Buy Now, Pay Later stocks. The Buy Now, Pay Later, or 'BNPL' sector, has certainly captured investors' attentions and imaginations over the last couple of years. This is due to the exponential growth rates in customers, transaction values, and of course, stellar share price appreciation!

More recently, the sector has been thrust back in the spotlight with the acquisition of local market leader Afterpay by US-based Square Inc. With this exciting development as a backdrop, let's see if we can find the Top 3 ASX Buy Now, Pay Later stocks!

Highlights:

- BNPL sector overview

- BNPL sector opportunity & growth

- BNPL stocks on the ASX

- Afterpay (APT)

- Zip Co (Z1P)

- Pushpay Holdings (PPH)

- Ratings & fair value targets wrap

What's all the hype about?

Let's kick off with a very quick overview of the concept, as most people are probably aware of the model, and perhaps even used it sometime in the recent past to make a purchase. In its most basic sense, BNPL is a payments system facilitating commerce between retailers and consumers.

Consumers can make an instant purchase whilst being able to spread the cost over an interest free period. The purchase price is generally broken up into instalments, which are usually due every few weeks or so. BNPL helps consumers better budget their purchases, and many also appreciate the interest free nature of the product.

Also helping some consumers, there are generally fewer credit checks, and it's less likely you're going to be hit with massive fees and interest rates if you don’t pay on time - although these are certainly part of the deal if you don't.

Merchants on the other hand, like the fact they get paid upfront for the purchase, minus some fees from the BNPL provider of course. And given so many consumers have embraced the concept, many merchants feel obligated to offer a range of BNPL options in order to attract and retain customers.

For the BNPL companies, there are fees to be earned from merchants, and also late fees from consumers who don’t pay on time. But, like any credit provider, there are significant risks in lending consumers money. Note though, defaults in the BNPL sector are the small minority of cases, with most providers seeing only a few percent of sales lost to non-payments. Interestingly, the sector generally doesn't chase up debtors, instead using the stick of permanent platform bans in these relatively rare cases.

So consumers like it, merchants like it, and the sector has been growing very quickly as a result.

That's a nice segue into my next slide about the opportunity in the BNPL sector. Currently, credit cards, BNPL's main competitor, account for just over 30 per cent of global retail sales. In comparison, BNPL has just 1.8 per cent of the global payments pie. So there's plenty of room for catch up.

Indeed, various think tanks expect the BNPL sector to more than double in size by as soon as 2025, and long term compound annual growth rate estimates range from around 20 per cent to as high as 45 per cent per annum.

There are few other sectors in the stock market at the moment that are experiencing such growth, or that have such a huge opportunity going forward. For this reason, we've seen an explosion in locally listed BNPL plays, many of which have added BNPL options to existing financial services businesses.

It's a BNPL gold rush!

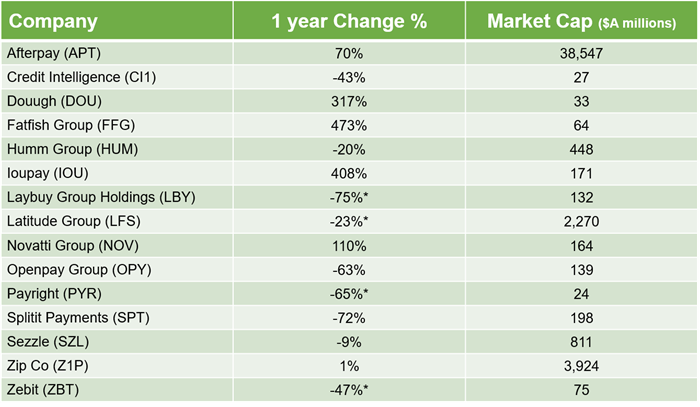

The table below shows all of the ASX listed BNPL players in alphabetical order. In the middle column, we can see that not all of these stocks have enjoyed the same growth in share price over the last 12 months. Many of the most recent entrants, like Laybuy Group, Latitude, Payright, and Zebit, have suffered substantial falls since their respective IPOs.

The biggest player, and by a long way, is Afterpay, at around $39 billion dollars in market capitalisation. It's nearly ten times bigger than nearest rival Zip, and there's daylight again to the next largest pure-BNPL play in Sezzle, which has a market cap of less than one billion dollars.

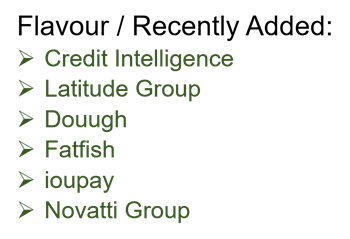

Before we look at the Top 3 BNPL picks, let’s quickly sort them into two groups. This group we've labelled "Flavour or Recently Added". This means that these stocks typically had other financial services businesses prior to adding a BNPL option. For many of these businesses, BNPL may not be the main focus of their activities.

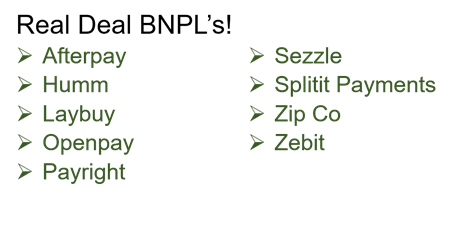

The companies in this list, are for the most part, BNPL specialists. This is not to say that they aren’t looking to go the other way and add more traditional financial services like Afterpay and Zip have already done, rather, for now, BNPL is their main source of revenue.

Bigger is better for Afterpay

First up, the market leader, Afterpay. And where better to start than with its acquisition by payments solutions provider, Square Inc. If you're an Afterpay shareholder, around the early part of 2022, your Afterpay shares are going to be converted into Square shares.

The good news is that both companies are growing very rapidly, and the combination of the two businesses will unlock significant synergies and cross-selling opportunities. For Afterpay, it gets instant access to Square's portfolio merchant customers which number in the millions. This is a major step up from Afterpay's existing merchant pool of around 100,000.

The businesses are very different, but complimentary, so for Afterpay shareholders, their investment becomes instantly more diversified than simply owning BNPL provider. Also, as APT will be part of a group which will be roughly 7 times bigger, it’ll have better access to funding options, and it’ll also enjoy better access to US capital markets due to its listing on the NYSE.

Let's have a quick look at Afterpay's main BNPL metrics. The company grew its active users to 16.2 million in FY21, up 63 per cent over the previous year. It now has access to 100,000 merchants, which made sales in excess of $22 billion in FY21. Afterpay is still heavily investing in marketing and growth, and therefore is yet to crack into operating cash flow positive territory.

We're going to see Zip's metrics in a second, but before we do, let's check out a couple of interesting stats from global BNPL leader, Sweden's Klarna. Klarna has reported similar stellar growth as our local hopefuls, but having been around substantially longer, and serving lager markets in Europe, it has grown to an impressive 90 million active customers, and boasts access to over 250,000 merchants. Klarna, along with Paypal's new Pay in 4, and Apple's immanent entrance to the space, certainly makes BNPL a hotly contested market. And it's impossible to ignore these risks when considering a potential investment in any of the local BNPL players.

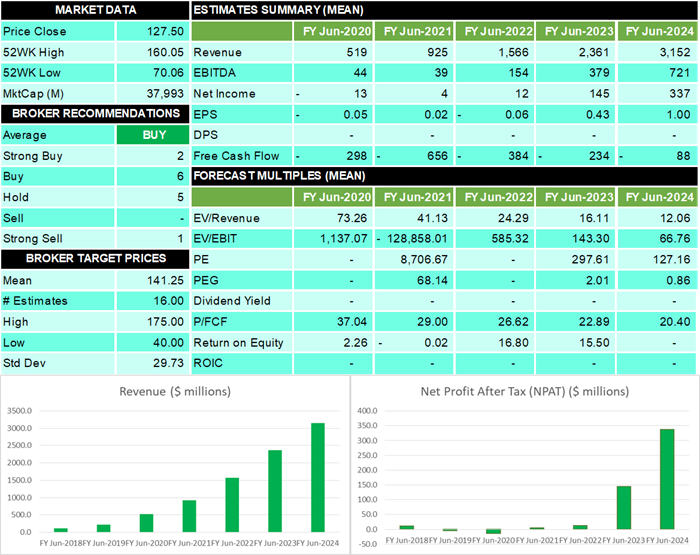

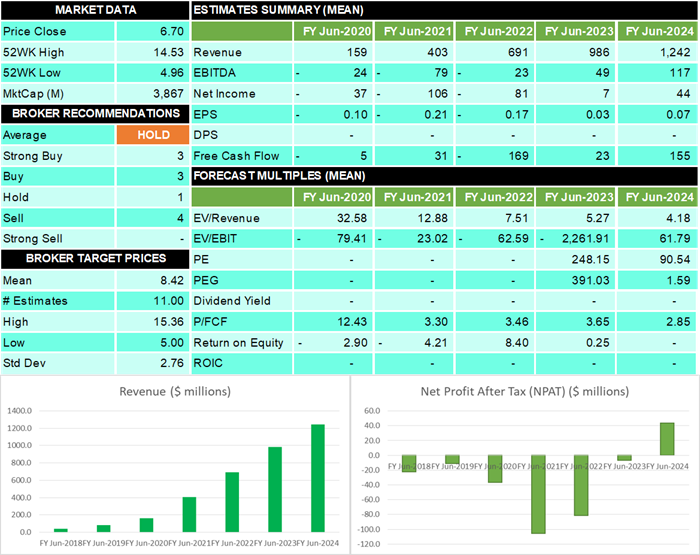

Let look at Afterpay's key numbers. Starting with broker consensus, we have an average rating of a buy with three strong buys, six buys, five holds and one strong sell. The brokers' average price target is $141.25 which provides approximately 10 per cent upside from the current price.

If we look at Afterpay's revenue growth over the last four years, it has been excellent, and looking forward, the brokers are expecting revenues to grow almost exponentially into FY24. Profits however have been elusive, with investors having to wait until FY23 to see substantial returns. But when we get there, profits are also expected to grow quickly. And you're paying a high price for that growth, we can see that Afterpay is trading on an eye-watering 298 times FY23 earnings. Due to the rapid growth in earnings, this will fall quickly, but we're still talking 127 times FY24 earnings and it’ll still be in the low triple digits in FY25.

The question is whether there's enough growth to justify the valuation, and the PEG would suggest not, at least not until FY24. Ideally, we'd like to see the PEG value less than one, so FY23's 2 is disappointing but Fy24’s 0.86 is attractive.

To buy Afterpay and back this incredible growth story, you really need to be comfortable with two things. First, paying 100 times earnings two years from now, and two, the possibility those earnings don't materialise, or at least not to the degree predicted. We call this second concept 'execution risk', and given the competition in the sector, we rate this as very high.

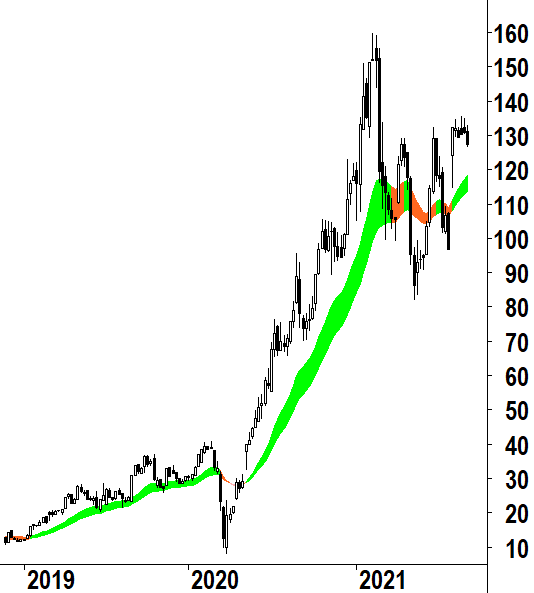

The Afterpay weekly chart was looking solid up until this week, and that’s possibly a reflection of the positive broker consensus and the degree of buffer in the average target price. We can see a strong long term uptrend, which was helped a great deal by the Square news. Recent weeks’ candles indicate the possibility of a pullback however, which could target the dynamic short term trend zone, that’s the light green zone, which typically acts as an area of support. This is going to be in the low $120’s and we’d want to see how the price action behaves there before calling Afterpay a technical buy.

Given the long term trend is still up, and given the room to our fair value target of $143.80, about 12% at current prices, we’re going with a hold rating, high risk if you've got it, but a watch for an appropriate buy signal at technical support if you don’t.

Um…hey, what's that elephant doing there?

Next up is Zip, Afterpay's distant second. The elephant in the room is whether this is the next obvious takeover target? Certainly, there are a number of elephants in the room which could do the job, ranging from other large and mid-tier players, to larger financial institutions which feel they've missed the boat on BNPL, and want a Zip-sized running start.

One can't help but feel, with the scale of the competition out there, this might well be the best Zip’s best outcome. But, corporate action aside, there is a great deal to like about the company, including its 7.3 million active customers, 4.4 million of which are in the US. Those US customers are particularly sticky, and very active, transacting at over 30 times per annum, one of the best stats in the industry.

Like Afterpay, Zip's growth numbers are spectacular, but investors are still waiting for a profit as the company continues to invest heavily in its growth. But, unlike Afterpay, which had around a half-billion dollar operating cashflow deficit, Zip has gone operating cash flow positive two years in a row now, and nicely so in FY21 to the tune of $44 million dollars. The other key comparison which demonstrates Zip's relative attractiveness to Afterpay is the fact its enterprise value to revenue, or EV to R is around one-third of Afterpay's. EV to R is a handy valuation tool for companies that don't yet have a PE Ratio, we're basically measuring how much we're paying for the company's revenues, so lesser is better.

The jump in EPS isn't expected until FY24 when we drop to a PE ratio of 90 times, sure this is high for say ANZ Bank, but it compares favourably to Afterpay's 127 times FY24 earnings. The PEG could be better at 1.6 for FY24 though.

As for the brokers, they're a little more circumspect on Zip than Afterpay, despite the more attractive valuation metrics. We're looking at an average recommendation of a hold, with three strong buys, three buys, one hold, and very interestingly, four sells.

We can perhaps see the benefit of size and scale for Afterpay, and the penalty applied to Zip for not having it. The broker's price target is relatively bullish however, at $8.42, it allows for just over 25 per cent upside from current prices.

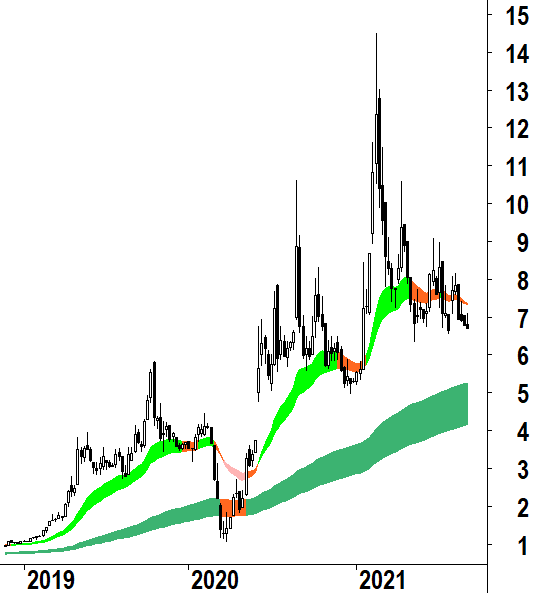

The weekly chart looks shaky in the short-to-medium term with the short term EMA's threating to cross down and signal an official short term downtrend. The price action shows well entrenched lower peaks, which demonstrates increasing supply. On the other hand, the troughs are hanging in there, indicating demand is working around that $6.50 to $7.00 zone, but it's far from convincing. A break of $6.50 is a real danger here, and that could see a quick drop to around the long term uptrend zone and the December 2020 low of $4.96.

Based upon our earnings and growth rate assumptions, we have calculated a fair value target of $8.82 for Zip, which is a touch better than the brokers, allowing for around 31 per cent upside. But, given the uncertain technical picture, and the uncertainty in general about Zip delivering on its growth aspirations, the best we can do is a hold if you've got it, and a high risk rating. If you don't currently have Zip shares, there's little reason to do anything right now apart from watch and wait for the chart situation to improve.

BNPL? Nope, but even better

Ok, you got me, whilst Pushpay sounds like a Buy Now, Pay Later stock, it's far from it. Pushpay is in the payments facilitation sector though, and like the BNPL's, it brings together consumers and organisations, making it easier for both parties to get what they want out of a transaction.

In this case though, the consumers are members of various faith congregations and other not-for-profits, and the organisations are seeking donations. The COVID pandemic has changed the way these organisations raise money from donors forever. Gone is unhygienic cash and coins, and in is a totally digital, secure, and easy to track and manage software based application.

And Pushpay is the leader in the industry with over 11,000 organisations on its customer list. It handled an impressive $7 billion dollars worth of transactions in FY21, and derived just over $41 million in net profits from the fees it charges for its software and services.

Other key stats we really like about Pushpay is its strong and growing operating cashflows, that means it's self-sustaining in terms of investing for growth, and it also increases the likelihood of dividends in the near future. Finally, because Pushpay has adopted a software as a service, or 'SaaS' model, it has excellent margins.

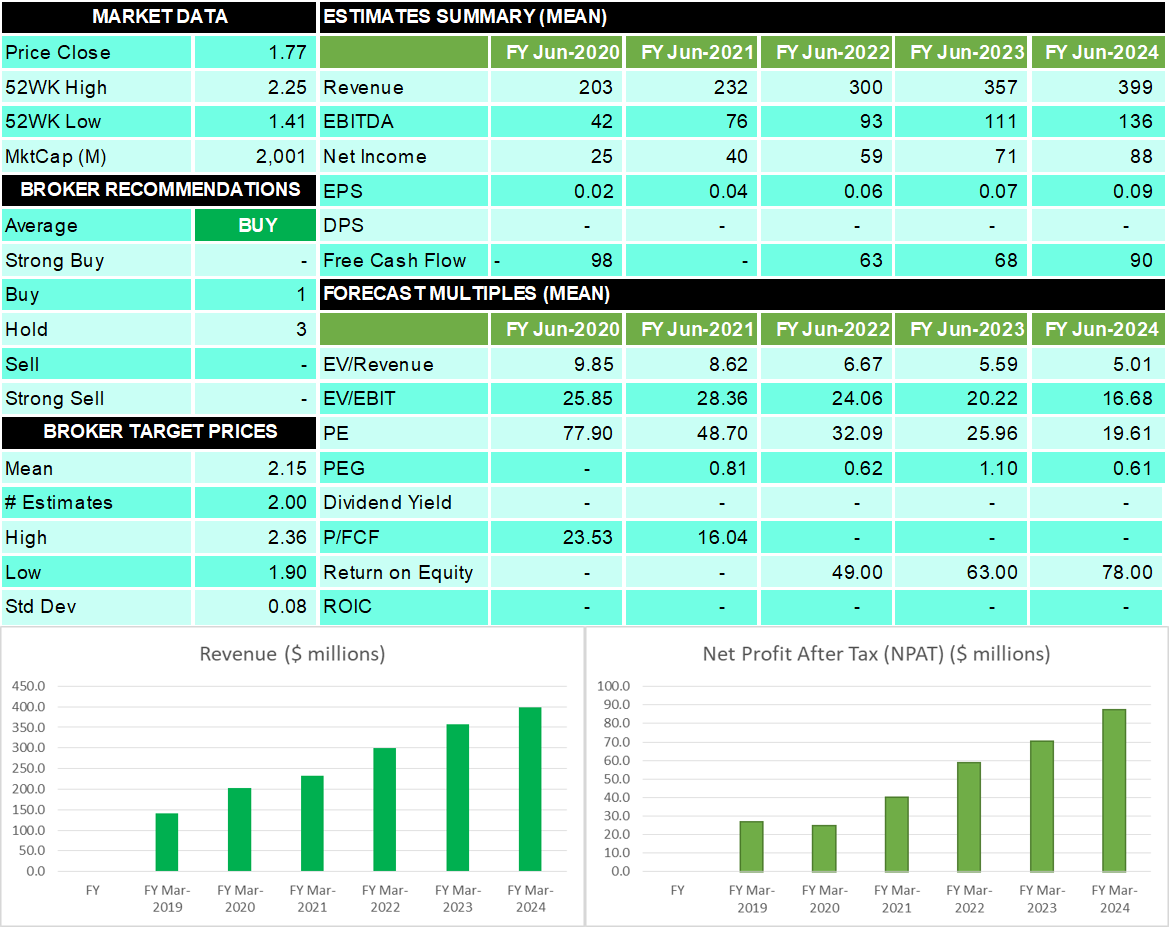

Looking at the numbers for Pushpay, we can see that the brokers are at an average rating of a buy, but only just, with the one buy and three holds. They have an average price target of $2.15 which allows for around 21 per cent upside from the current price.

Revenue growth and NPAT charts look impressive with the strong track record of growth in each set to continue through to FY24. The valuation of 32 times current FY's earnings is quite reasonable, especially when considering an average growth rate in the low 20 per cent range for the next 3 years. This brings the PE down quickly to an attractive 19 times earnings by FY24. The PEG is solid, hovering around and below the important one level, so we're not overpaying for the growth in this business.

Return on equity, which is a measure of business efficiency, is typically good for companies with a software as a service model. But, the 49 per cent this financial year, rising to 78 per cent in FY24, is outstanding.

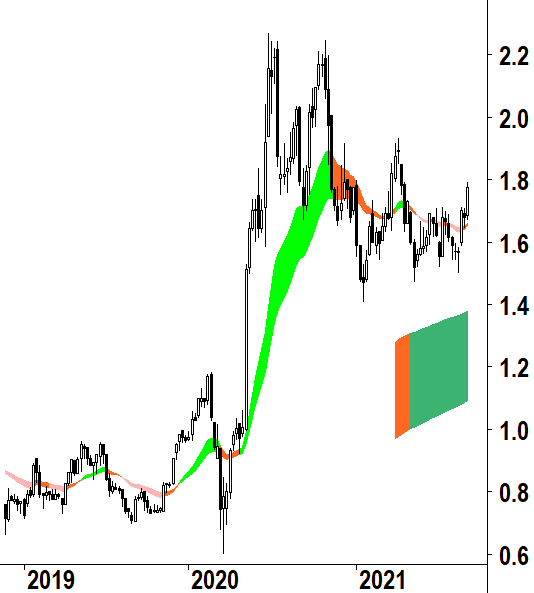

The chart looks very constructive with an extended period of consolidation around the $1.50-$1.70 level looking like it's now breaking to the upside. We like the prevalence of white candles more recently, and this week's break above the peaks set in July is very encouraging. Altogether, it's looking increasingly likely the supply overhang from the big run up in 2020 is finally taken care of.

Based upon our earnings and growth estimates for Pushpay, our fair value target is a couple of pips better than the brokers at $2.17, which allows for around 22 per cent upside. We think the execution risk is low on this one, and adding in the attractive valuation and the chart, we've gone with a buy, low risk rating.

I'll take it…wrap it up!

Let's wrap up our look at the Top 3 ASX BNPL Stocks. Well, at least 2 BNPL's and one payments software innovator!

Firstly, the biggest and the best, at least of the local players, and to be fair, potentially now a serious global contender given the massive bump in scale and scope it's going to enjoy from the Square acquisition. We like the deal, and the chart, but the valuation upside is just a little too thin. Square has certainly de-risked Afterpay as an investment option, but not quite enough for us to go any better than high risk, and that's on a hold rating with a fair value target of $143.80.

Next up, Zip. A conundrum wrapped in a riddle. There's plenty to like here, not least it's superiority to Afterpay on a valuation basis. But, that discount is probably there for a very good reason, and the chart appears to back this up. It doesn't look like the big brokers see the blue sky that many smaller investors frothed over at the start of this year. We're a hold at best, but even that's on shaky ground with one look at the chart. Its high risk rating is obvious, and the very attractive fair value target of $8.82 is not enough to entice us in, at least not at the moment.

Finally, Pushpay, the impostor in this video, but a payments provider nonetheless. It’s certainly an innovative and exciting business with great growth, great operating cashflows and excellent and growing margins. The chart is turning up and the valuation looks attractive. We're confident it's going to at least meet our earnings and growth targets. For this reason, we're a low risk buy on this one with a fair value target of $2.17, allowing for around 24% upside.

That's it for me this time! I trust you enjoyed this look at the Top 3 ASX Buy Now, Pay Later stocks. All the best for your trading until we catch up again.

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.