The buzz word in the financial press over the last couple of weeks is "inversion". More specifically, this word has been used with another word sure to get your attention: "recession". Of course, journalists love clickbait headlines (so do we!), but there's usually quite a bit of jargon used trying to explain why these two words have been linked. In this article we'll get to the bottom of what this inversion business is all about, and whether investors should be concerned about an impending recession.

Highlights:

- What are bonds and which factors impact their yields?

- What is a yield curve?

- What is yield curve inversion and why does it occur?

- Does a yield curve inversion cause a recession?

- What happens to stocks after yield curve inversion?

What is a yield curve anyway?

The current fuss is all about the inversion of the yield curve. The what I hear you say? Yes, I get it. It's not so much who cares about the yield curve, it's more what the hell is the yield curve in the first place!? Let's do a quick Fixed Interest 101 course. Real quick, I promise!

Fixed interest investing involves you lending your money to another investor for a fixed period. For the benefit of using your money (to do whatever they like) over that period, they agree to compensate you with and agreed amount of interest. In reality, "other investors" are banks (with respect to term deposits), the Australian government when referring to Australian Government Bonds or the US Government in the case of US Treasury Bills, Notes, and Bonds, and companies like Commonwealth Bank or Apple when referring to corporate bonds.

So, term deposits, bills, bonds, and notes (and a few more we won't go into today) are all forms of fixed interest assets. For simplicity, let's just collectively refer to bills, bonds, and notes simply as "bonds" (this is probably the more common term). Let's also drop term deposits from our discussion for two important reasons. Firstly, you can't trade term deposits. That is, you can't walk down to your your local bank branch and buy your next-door neighbour's term deposit (nor can they buy yours). Secondly (relates to the first), term deposits aren't 100% standardised with respect to their amounts, durations, and interest rates.

These two characteristics of transferability and standardisation makes bonds ultimately tradeable (fungible), and therefore an attractive asset class for investors to own. Each bond has a "principle", which is the starting amount of the loan, the minimum denomination for a US T-Note for example is US$1,000. Each bond has a "duration" which is simply the period of time the principle will be locked up for. Bond durations range from very short term (overnight, days, and weeks), to short term (up to around 2 years), to medium term (around 3-5 years), and long term (10 years and beyond). Each bond has a single, fixed interest rate over its entire duration. For bonds with durations greater than one year, interest payments are made periodically, typically semi-annually. These periodic interest payments are sometimes referred to a "coupon". For bonds with durations less than one year, the coupon tends to be paid on "maturity" (i.e., the final date, or "maturity" of the bond, when the principle is repaid).

Once a bond is created, it can be bought and sold among investors just like they might buy and sell shares in a company. The price of the bond will depend on what the market's expectations are of future interest rates. For example, if a bond had a coupon rate of 2 per cent per annum, and interest rates were expected to fall to 1 per cent next week, it would soon be offering a far superior yield. The price of the 2 per cent bond would likely be bid up. This is why we generally find bond prices tend to do better during periods when the market is expecting interest rates are going to fall. Conversely, if interest rates were expected to rise to 3 per cent next week, our same 2 per cent coupon rate wouldn't look so attractive anymore. Investors would prefer to sell the 2 per cent coupon rate bond and invest in the higher paying 3 per cent bond. This is why we generally find bond prices tend to suffer during periods when the market is expecting interest rates are going to rise.

This dynamic is important because it demonstrates a bond's price will change as expectations for future interest rates change. Because bonds have a fixed coupon, the only way to compensate a potential investor in the bond for higher interest rates down the track is to discount its price. The discount in price effectively boosts the yield on the bond to align it more closely with current market rates. Now, you generally need a bachelor's degree to do bond pricing, so we’re going to greatly simplify here. Using really round numbers, a bond which might initially have been issued for $1 with a 5 per cent yield, might now have to sell at 98 cents to compensate new investors for the fact market interest rates are now at 7 per cent.

Ok, I think we can finally get to the yield curve! It's simply a line chart representing the difference in interest rates across a related group of bonds with different maturities. We typically refer to the yield curve for say, Australian Government Bonds, or for US Treasuries. Why would bonds of different maturities have different interest rates? Note, the yields being tracked by the yield curve are the market-based yields we discussed earlier (i.e., not the original coupon yields). So, when we look at a yield curve, we are getting an overall view of how the market thinks it should be compensated for expected interest rates over the span of the curve. If we're talking about a group of assets as ubiquitous as US Treasuries, then when we look at the yield curve for these securities, we're kind of looking at how the world feels about interest rates over the next 30 years. Pretty neat, huh?

A typical yield curve is upward sloping, that is, it demonstrates interest rates are lower on bonds of shorter durations, and progressively higher on bonds of longer durations. This is due to the time value of money. We all know that a dollar today is worth more than a dollar you have to wait a year to get your hands on. This is because the stuff we want and need usually gets a bit more expensive over time. This is called "inflation". It's also because you could take that dollar today and buy an NFT of an ape in a sailor's hat and potentially quintuple your dollar by next year. This is called "opportunity cost". Investors want to be compensated for this as well. So, because of inflation and opportunity cost, the longer the duration of a bond, the greater the interest rate investors will demand as compensation (i.e., via either the coupon rate on a new bond, or by the market-based yield on an existing bond).

In certain, relatively rare circumstances, macroeconomic conditions conspire to drive bond investors to behave in ways we wouldn’t ordinarily expect. This behaviour can contort the yield curve in a way which is rather counterintuitive, and which has in the past been a very reliable indicator of nasty things to come for the global economy. Ok, newly anointed Bond Professors! It's time to talk yield curve inversion!

Waiter…there's an inversion in my yield curve!

About 95% of the time, the yield curve is upward sloping. As suggested above, occasionally we find short-term rates are higher than long-term rates. When this happens, we say the yield curve has "inverted". Yield curve "inversions", as they are commonly referred, are rather counterintuitive –after all, don’t' they imply longer term investors have forgotten about the time value of money?

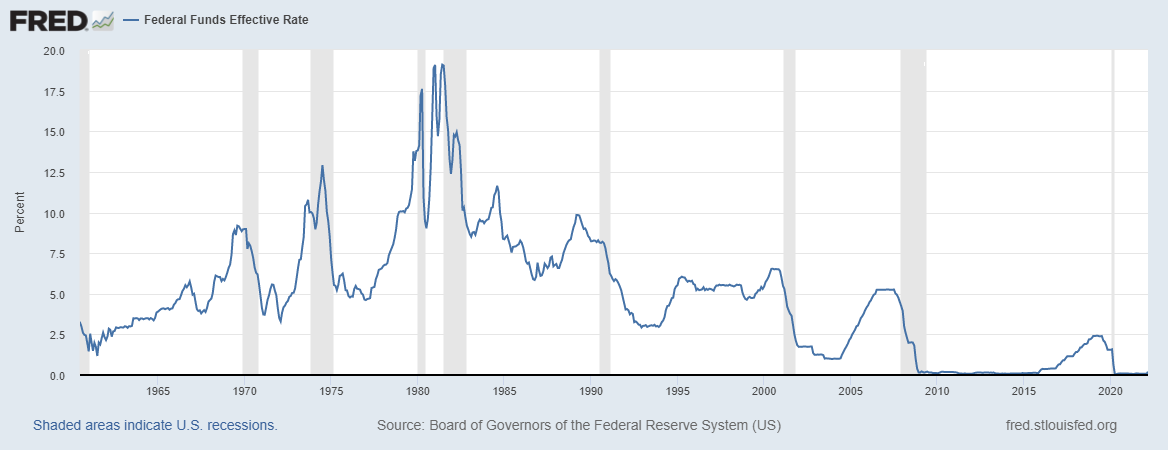

Not quite. Yield curve inversions have historically occurred when markets are expecting a substantial and rapid increase in short-term interest rates. Often, this scenario has coincided with central banks hiking official interest rates very quickly, generally in response to growing inflationary threats. This is largely the case with respect to the current yield curve inversion, but it was also the case which likely caused previous inversions in the 1970's and 1980's. What's different this time, is just how low shorter-term rates were before they started spiking.

Federal Funds Effective Rate (Source: FRED)

Federal Funds Effective Rate (Source: FRED)

For pretty much all the other inversion-to-recession occurrences, rates started from relatively neutral settings at the time. I say, "relatively neutral" here, because the 6 per cent or so official interest rate preceding the 1988 inversion-recession might sound high to us today, but it was well down from the 19 per cent peak in 1981. This time it's different (heard that one before!). Just before the current inversion, official interest rates had a starting point of zero. Even more incredible, the market-based yield on some bonds, particularly those in Europe, are negative (there's still around US$2.5 trillion worth of bonds out there with a negative market-based yield!). A negative yield means you are paying someone to hold your money, knowing you're going to lose money over the duration of the bond. So, you could argue that the system was really broken before the current inversion.

Pandemic. The most acute recession ever. Unprecedented supply chain chaos. War. Energy price spike (remember the 1970's?). Worst inflation in two generations. The current macroeconomic situation has just about got it all! Each of these bits and bobs contributes to the two main ingredients of a yield curve inversion: 1. Official rates are starting off a low base (very low for us!); and 2. Central banks respond with a sudden and large increase in official interest rates. Funnily enough, this time, ingredient 2 hasn't even happened! The US Federal Reserve (the Fed) delivered its first official interest rate hike in March this year, increasing rates from a target range of 0%-0.25% to 0.25%-0.50%. Yet, if we look at bond markets this year, they have collapsed! The key bond indices are down around 11% over the last 12 months with around two-thirds of that loss occurring in just the last 3 months. Many media outlets are calling it an "unprecedented loss".

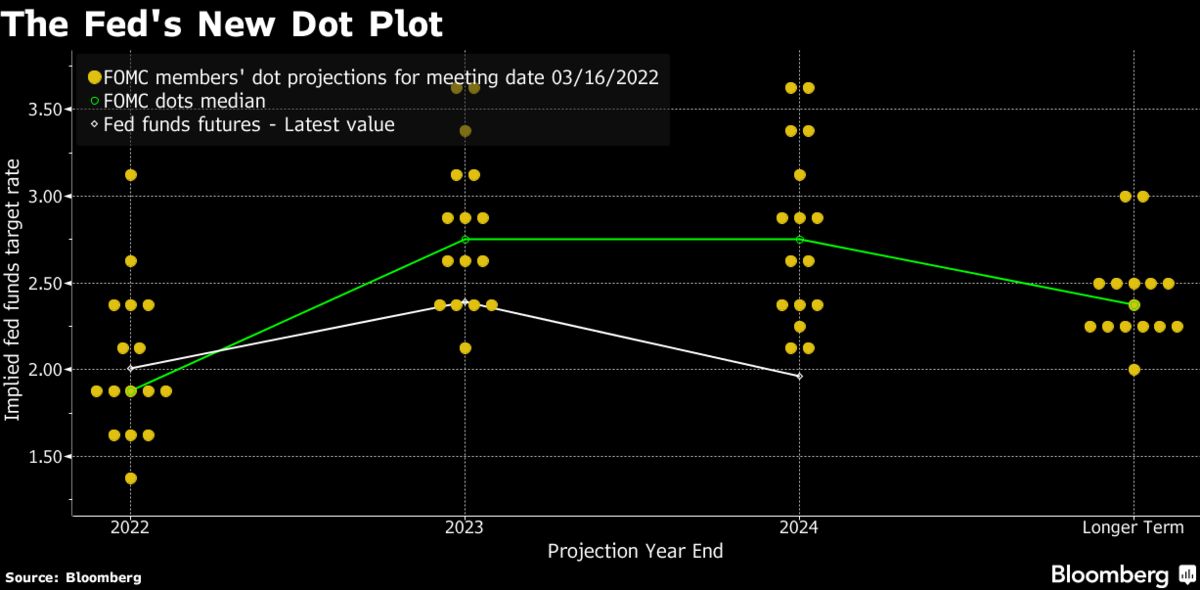

On the surface, the Fed's 0.25% rate hike didn't appear too shocking, yet since January the markets unravelled (including a significant wobble in the stock market). Why? Well, we must remember markets look forward, not backward. The 0.25% increase from March is just the first in what appears is going to be very aggressive rate hike cycle for the Fed. Looking at the "Dot Plot" from their last meeting, markets are now assuming official interest rates are probably going to rise to around 2% by the end of 2022, and then peak at around 2.75% by the end of 2023.

US Federal Reserve Dot Plot as after March 2022 meeting (Source: Bloomberg)

US Federal Reserve Dot Plot as after March 2022 meeting (Source: Bloomberg)

The Fed has made it clear it feels such rate increases are necessary to reset inflation expectations in the wake of the worst surge in US inflation we've seen since the early 1980's. Higher interest rates, we know, hurt bond prices, and they're not always so great for stock prices either (that's a topic for another day). So, it makes sense that bonds are down this year. What doesn’t make sense, is why bonds experienced such "unprecedented" falls.

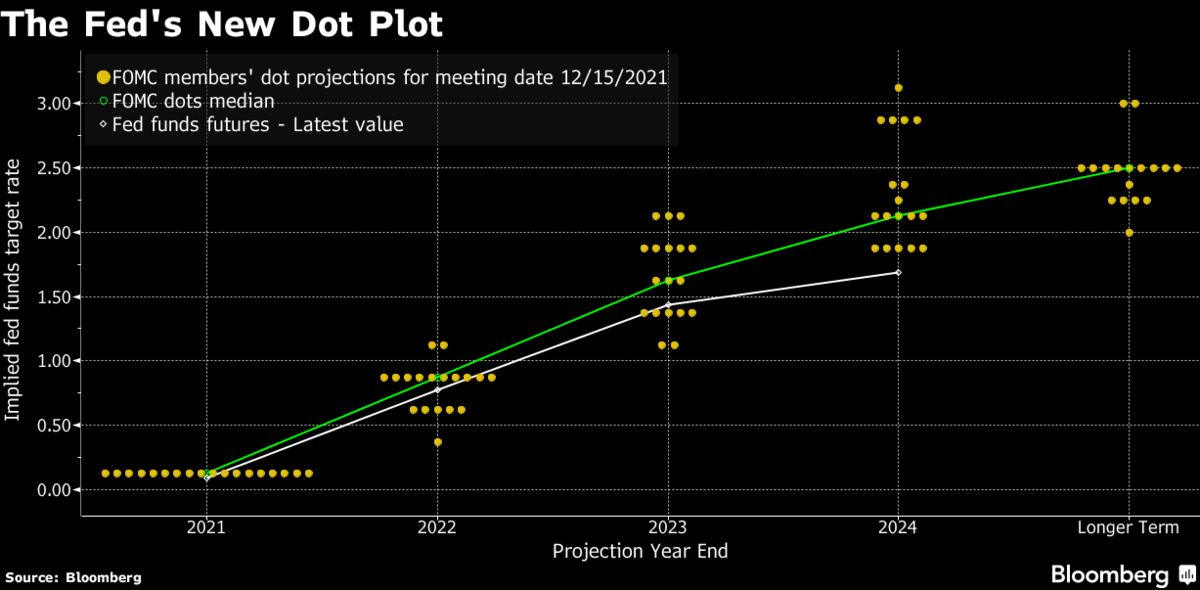

US Federal Reserve Dot Plot as after December 2021 meeting (Source: Bloomberg)

US Federal Reserve Dot Plot as after December 2021 meeting (Source: Bloomberg)

Much of the confusion in the bond market can be attributed to this second Dot Plot above, the one from the Fed's December 2021 meeting. Yep, a bit different huh? Just three months prior to the March plot, and they were only indicating 0.75% by the end of 2022, and just 1.5% by the end of 2023. Oops, that's big shift in a very short space of time for something that doesn't often move very much – if at all. And that's why markets spat the dummy and threw all their toys out the pram! Hmmm…Thanks Fed!

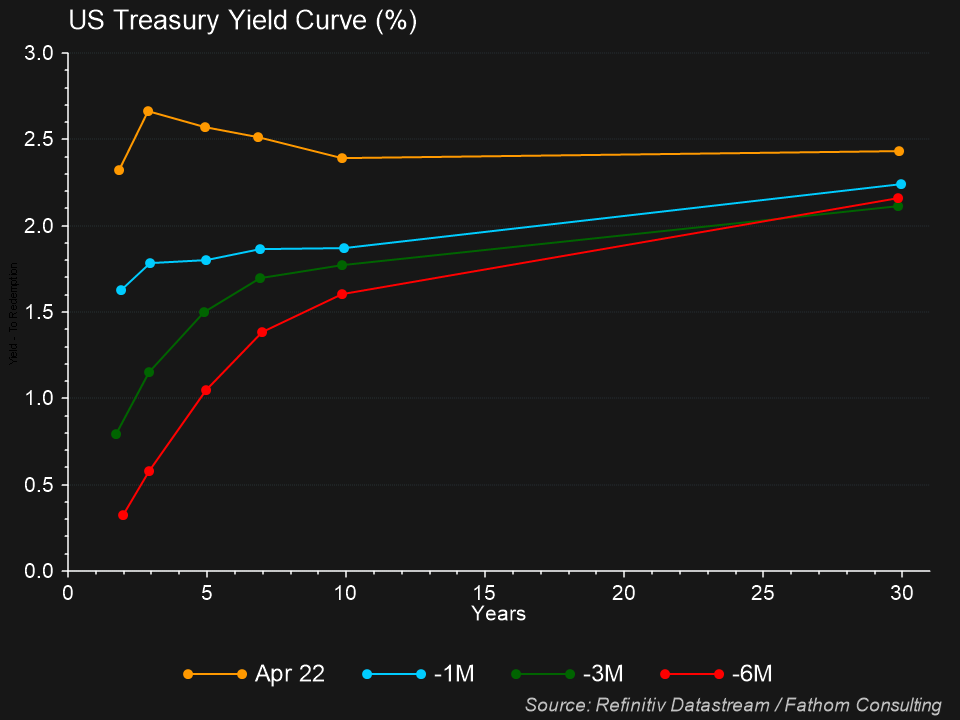

Current, 1 month, 3 months, 6 months US Treasury yield curves comparison (Source: Refinitiv Eikon)

Current, 1 month, 3 months, 6 months US Treasury yield curves comparison (Source: Refinitiv Eikon)

In the yield curve charts above, we can see how the US Treasury yield curve has evolved over the last 6 months. The red line, which represents 6 months ago, is a plain vanilla upward sloping yield curve. So too is the green line from 3 months ago, just after the December meeting and before Fed Chairman Jerome Powell's pivotal speech on January 26. In this speech, which followed the Fed's January monetary policy meeting, Mr Powell warned markets for the first time the Fed would commence tightening in March and continue to do so at much faster pace than previously indicated. Over the course of the next week, stock and bond markets tanked. The blue line from 1 month ago is what bond traders call a "flat" curve, yes there's still a little upward slope there, but we can see how much the shorter end of the curve has risen against the longer end. And the orange line is April 1, inverted all the way from 2 years to 10 years. Quite incredible!

The sudden spike in the expected path of official interest rates explains why the shorter end of the yield curve broker higher, as short-term yields tend to move very closely with official rates. The front end of the curve up to 3 years increased by similar amounts to the Dot Plot shock – around 1.5%. But for the yield curve to flatten and eventually invert, it means longer term rates went up relatively less, or not at all. Market expectations are: "Rates are going up, big, fast!". Surely then, longer-term investors must demand

even higher interest rates than shorter term investors as compensation? Not always!

The clearest explanation for this phenomenon is the market may believe central banks are going to make a mistake, that is, they are raising rates too quickly and this will most likely trigger an economic slowdown much further down the track. A quick note on the relationship between bond prices and bond yields here. Based upon our definitions above, we determined that if higher market-based yields are required, lower bond prices are the only way to get them. So, when we say shorter-term bond yields have risen more sharply than longer-term bond yields (causing the inversion), we are also saying shorter-term bond prices have

fallen more sharply than longer-term bond prices.

There's a couple of good reasons why longer-term bond prices may remain robust compared to their short-term counterparts. Firstly, long-term bonds, particularly high-quality sovereign issues such as US Treasuries, are often considered to be good assets to hold in times of uncertainty. If the central bank, in this case the Fed, does make a policy mistake and crash the economy, then safe-haven long-term US Treasury bonds are usually a good place to hide. Further, if there is an economic recession down the track, the Fed is probably going to have to cut rates just as dramatically as they're increasing them now to deal with it. So, if rates "quite a bit down the track" are going to be roughly the same, or potentially lower, why sell off your long-term bonds now just because short-term rates are spiking? For many investors, the answer is: "

You don't".

100% record, including predicting the COVID-19 pandemic!

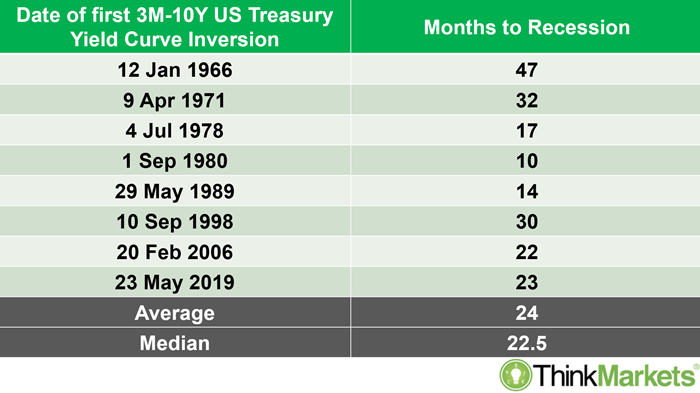

Ok, we've discussed what the yield curve is and why it happens. The big explanation for all the fuss in the media recently is to do with the fact that every single time the yield curve inverted since the 1960's, a recession ensued somewhere between a few months and few years later. Every time, without fail! Sounds bad, doesn't it? Well, we're not talking a huge sample size here – there have been a grand total of 8 yield curve inversions since 1966 for 8 recessions. We can say that at least one of those was a fluke – there's no way the last yield curve inversion in 2019 predicted the recession caused by the COVID-19 pandemic! Some might argue, sans pandemic, it might have happened anyway, but we'll never know!

3-month vs 10-year US Treasury yield curve inversions and time until subsequent recession (Source: ABN Amro, Strategy & Quantitative Research Yield Curve Inversion: the long short, April 2019, with additional data provided by Author)

3-month vs 10-year US Treasury yield curve inversions and time until subsequent recession (Source: ABN Amro, Strategy & Quantitative Research Yield Curve Inversion: the long short, April 2019, with additional data provided by Author)

The table above shows each time the yield curve inverted for the 3-month and 10-year US Treasury bond since 1966. Note, the average time between inversions was 24 months with a median of 22.5 months. There is a wide spread of delays however, from as low as 10 months in 1980, to as high as a whopping 47 months for the 1966 inversion. Each scenario was different, each with its own set of unique challenges and solutions – for better or worse. Personally, I'm not sure how much confidence we can take from such a small data set, and given such a wide range of delays until a recession. In particular, when considering those instances with longer delays, did the reason which caused the inversion really contribute to the recession, or was something else responsible by then?

Yield curve inversion vs the stock market

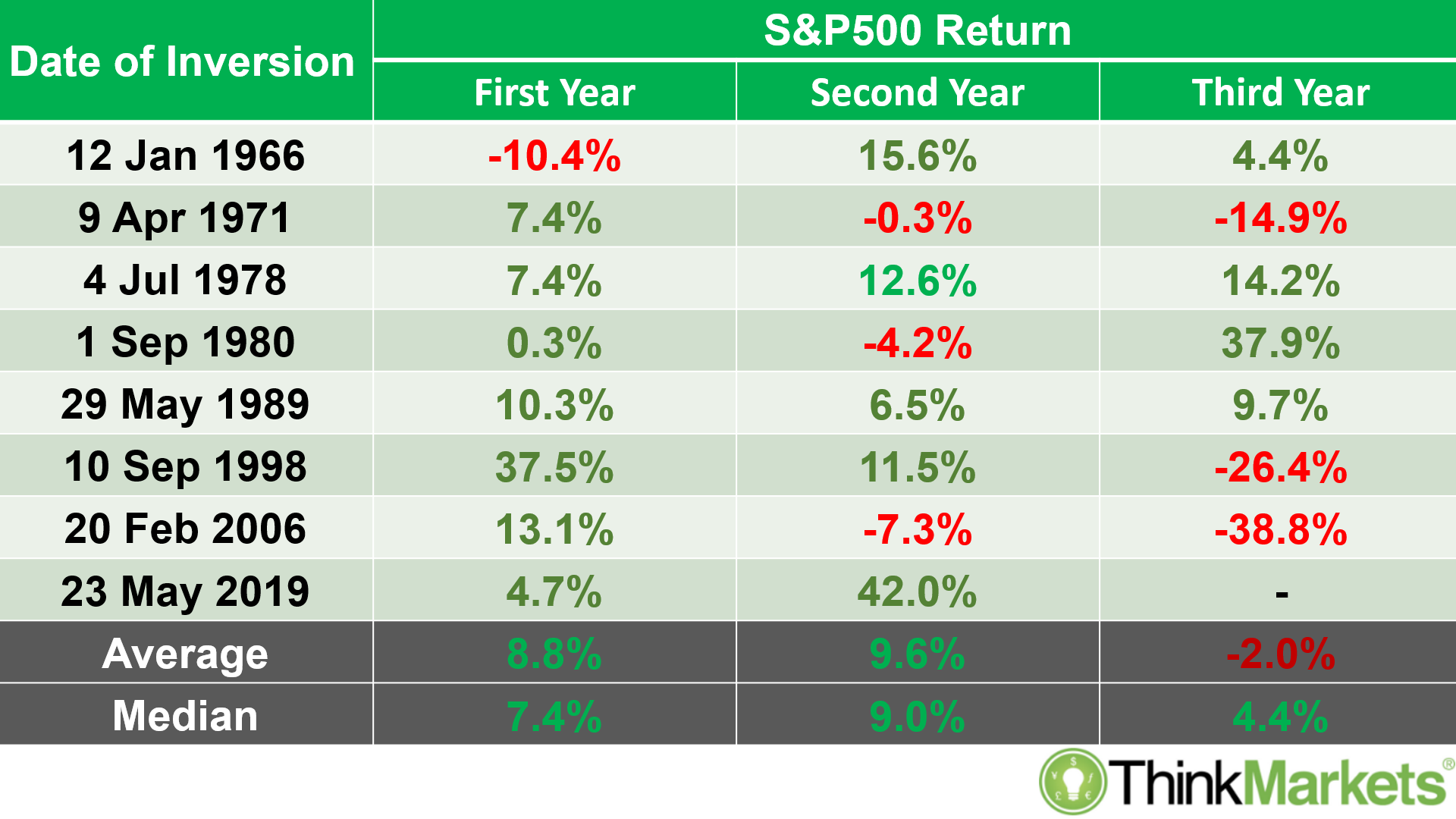

The next big question for investors, is what happens to stocks when the yield curve inverts? You might expect they've done very poorly – after all, if "inversion spells recession", surely it means stocks suffered? Nope. The opposite, actually!

S&P500 returns after 3-month vs 10-year Treasury yield curve inversion (Source: ABN Amro, Strategy & Quantitative Research Yield Curve Inversion: the long short, April 2019, with additional data provided by Author)

S&P500 returns after 3-month vs 10-year Treasury yield curve inversion (Source: ABN Amro, Strategy & Quantitative Research Yield Curve Inversion: the long short, April 2019, with additional data provided by Author)

The table above shows the returns for the S&P500 benchmark index of USA companies after each yield curve inversion since 1966. Again, there were plenty of other mitigating factors determining stock returns over this period, but the averages suggest stocks don't immediately suffer simply because the yield curve inverts. In the year immediately following an inversion, stocks showed a very robust average return of 8.8%, and in the next year after that, they returned an even better 9.6%. It's not until the third year after a yield curve inversion it appears stocks began to suffer, and even then, by a very mild average return of just -2% (but with a median

increase of 4.4%). The third-year performance makes more sense when you consider that the average recession is probably impacting the market by then. Prior to that, stocks tend to do what they usually do when there isn’t a recession – go up!

The data suggests the current yield curve inversion is nothing to fear for the time being. In fact, working the averages, you can continue to hold stocks for approximately another two years. I suggest however, it's dangerous to stake your portfolio simply on data of this nature. The best takeaway is to note an inversion has occurred, note its relevance in history, and therefore be attentive to any warning signs the global economy is beginning to turn south. Inversion or not – an economic downturn is rarely good for stocks!

Conclusion

And that's a nice segue into my conclusion. It's important to remember a yield curve doesn't cause a recession, and despite its impeccable track record, it doesn't necessarily guarantee one either. Further, in doing the research for this article, it became clear there's not a great deal of agreement among economists as to what exactly constitutes an inversion of the yield curve in the first place. This is because the following items are contentious: 1. Which parts of the yield curve inverting are relevant? (E.g., 3-months vs 10-years 2-years vs 10-years, 3-years vs 10-years, or 5-years vs 30-years are each popular indicators); and 2. How long must the yield curve be inverted for? (Some researchers based their findings upon the first occurrence of their chosen yield curve inversion, and others used rules like "the yield curve must be inverted for at least a quarter"). The various definitions of these items impact the start time of an inversion, and therefore the calculation of the length of time until the subsequent recession (I read one study which quote an average time of just 14 months). So, we must consider statistics related to time between yield curve inversion and recession with some caution.

What I can say with utmost confidence though, is when we've seen a yield curve inversion, there has always been a major dislocation in the global economy. This dislocation caused central bankers to take drastic actions to rectify it. The more drastic the action taken, the greater the risk they made a mistake, and therefore the greater the risk of one possible outcome of that mistake – a recession. Just looking at the current macroeconomic situation, it does appear to fit the mould for a fairly typical yield curve inversion-to-recession scenario.

One thing is clear, however, there has always been a delay between yield curve inversion and recession. This is fantastic because it gives investors time to prepare for the worst should they wish to, and for central bankers to try their darndest not to get us there! To get to a recession from here, we must assume the Fed fully intends to make a great big policy mistake like many of their predecessors! Surely Chairman Jerome Powell and all his buddies at the Fed are also aware of the old "yield curve inversion equals recession chestnut"? They wouldn't walk us into another crisis, would they!?

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.