Weak macro pointers from the UK and Eurozone added to concerns over the rollback of reopening measures in the US, raising serious question marks over a swift global recovery.

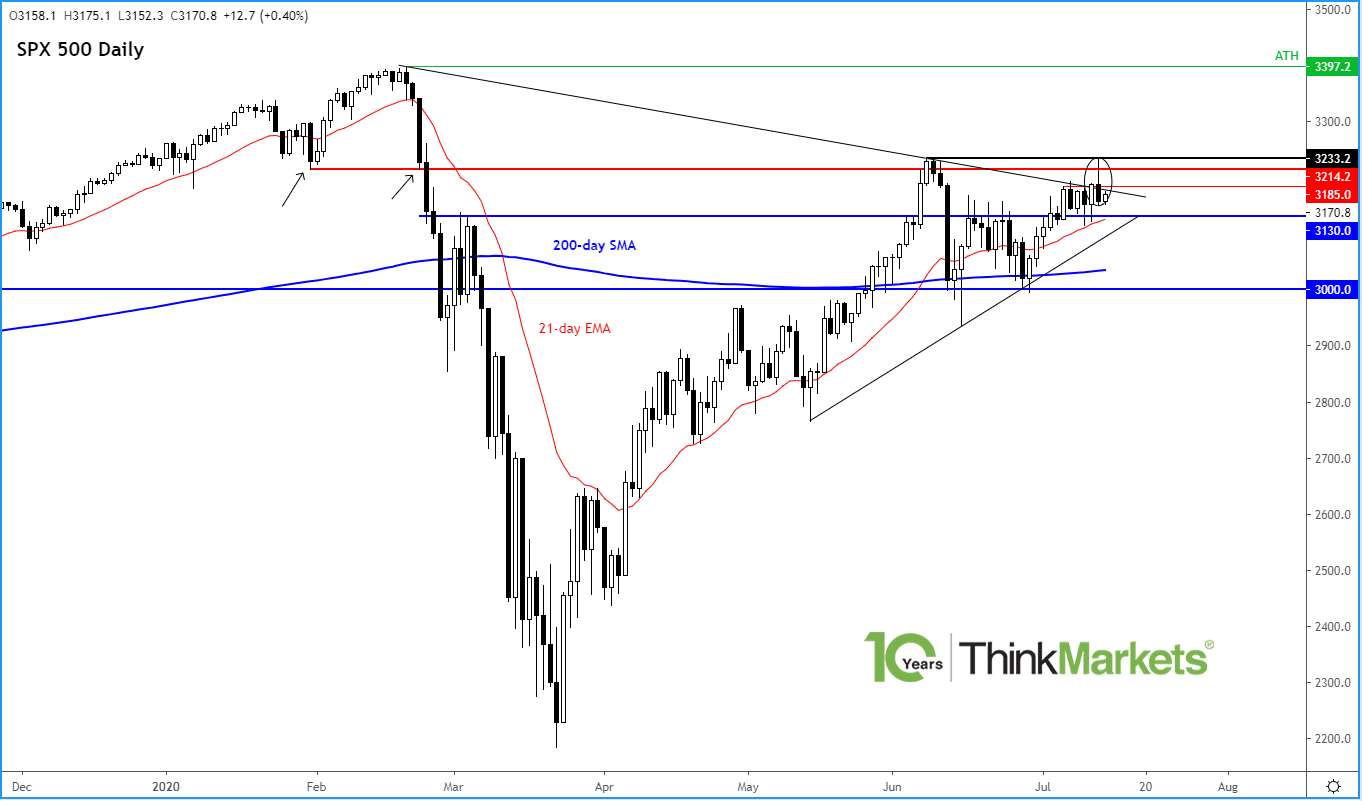

The key question today is whether there will be follow-through after Monday's sharp reversal on Wall Street where technology companies in particular took a big hit after the Nasdaq had hit a fresh record high earlier in the day. By midday in Europe, the likes of the FTSE and DAX were holding their own relatively well as investors considered the risks of upcoming corporate earnings and the economic impact of rising coronavirus cases against more stimulus. US index futures had stabilised just above Monday’s lows with investors digesting the first batch of US bank earnings results.

Sentiment was cagey though after a turbulent session on Wall Street on Monday. Weak macro pointers from the UK and Eurozone added to concerns over the rollback of reopening measures in the US, raising serious question marks over a swift global recovery. There is so much uncertainty and following Monday’s sharp reversal in the US, some investors will be wondering whether it is now time to bank profit and get out of equities. If stock indices do break lower again today and hold below Monday’s lows then more and more longs could exit, potentially resulting in a sharp sell-off as the week progresses.

In the US, several states have now reversed their opening plans. California has closed all its bars, while indoor business has stopped for restaurants, movie theatres and museums. Texas, Arizona and Florida have also reversed easing of lockdown. Elsewhere around the world, Iran’s capital, Tehran, has shut some public places and businesses for at least a week after a spike in Covid-related deaths, while Hong Kong has also shut down schools and cinemas.

US banks will be busy reporting their quarterly results this week. JP Morgan reported earlier and Wells Fargo and Citgroup were due to publish their results shortly.

JP Morgan reported an EPS of $1.32 vs. $1.01 estimate, on revenue of $33 billion vs $30.3 billion eyed. Provision for credit losses were slightly higher than expected at $10.47 billion, while sales and trading revenue exceeded expectations. Overall, not a bad quarter you have to say for JPM but it remains to be seen how the bank fares in the coming months as low rates should weigh on profitability while the risk of borrower defaults will be another key risk to take into account.

Meanwhile in FX, the pound was one of the worst performers on the day as fresh data dashed hopes over a swift, V-shaped, recovery. After the record 20.3% slump in April, UK GDP was expected to rebound by 5.5% in May as lockdown slowly eased. However, output only rebounded by 1.8% on the month, disappointing even the most pessimistic of forecasts. All other UK macro numbers disappointed expectations, too. Industrial production rose 6.0% m/m vs. 6.2%; construction output rebounded by 8.2% m/m vs. 15.0%, and the 3-month moving average of services index slumped 18.9% in May vs. -16.9% expected.

Eurozone data also disappointed expectations following the poor UK numbers that were released earlier. Her is today’s data recap so far:

- Eurozone data

- German July ZEW expectations survey printed 59.3 vs. 63.4 last (but in line), while the current situation survey printed -80.9 vs -65.0 expected

- Eurozone May industrial production +12.4% vs +15.0% m/m expected

- UK data:

- UK GDP growth in the month of May was expected to be +5.5% but was far lower at +1.8%.

- The construction industry saw far poorer growth of +8.2% than the expected +14.2%.

- The Index of Services saw a record low -18.9% in the 3 months to May, lower than the expected -16.9% reading. This was the largest contraction in three-monthly movements since records began in January 1997.

- Industrial production saw slightly lower-than-expected growth at +6.0% instead of the expected +6.2%. Manufacturing production exceeded expectations, with output rising 8.4% in May compared with 7.5% expected (your version made perfect sense but a bit broken for a sentence)

Coming up:

- US CPI

- Earnings from Wells Fargo and Citi

Source: TradingView.com and ThinkMarkets