Risk appetite turned sour Thursday morning as investors dumped European stocks, crude oil and bought the US dollar, although the greenback started to ease off its highs by mid-morning which saw the GBP/USD test the 1.30 handle again.

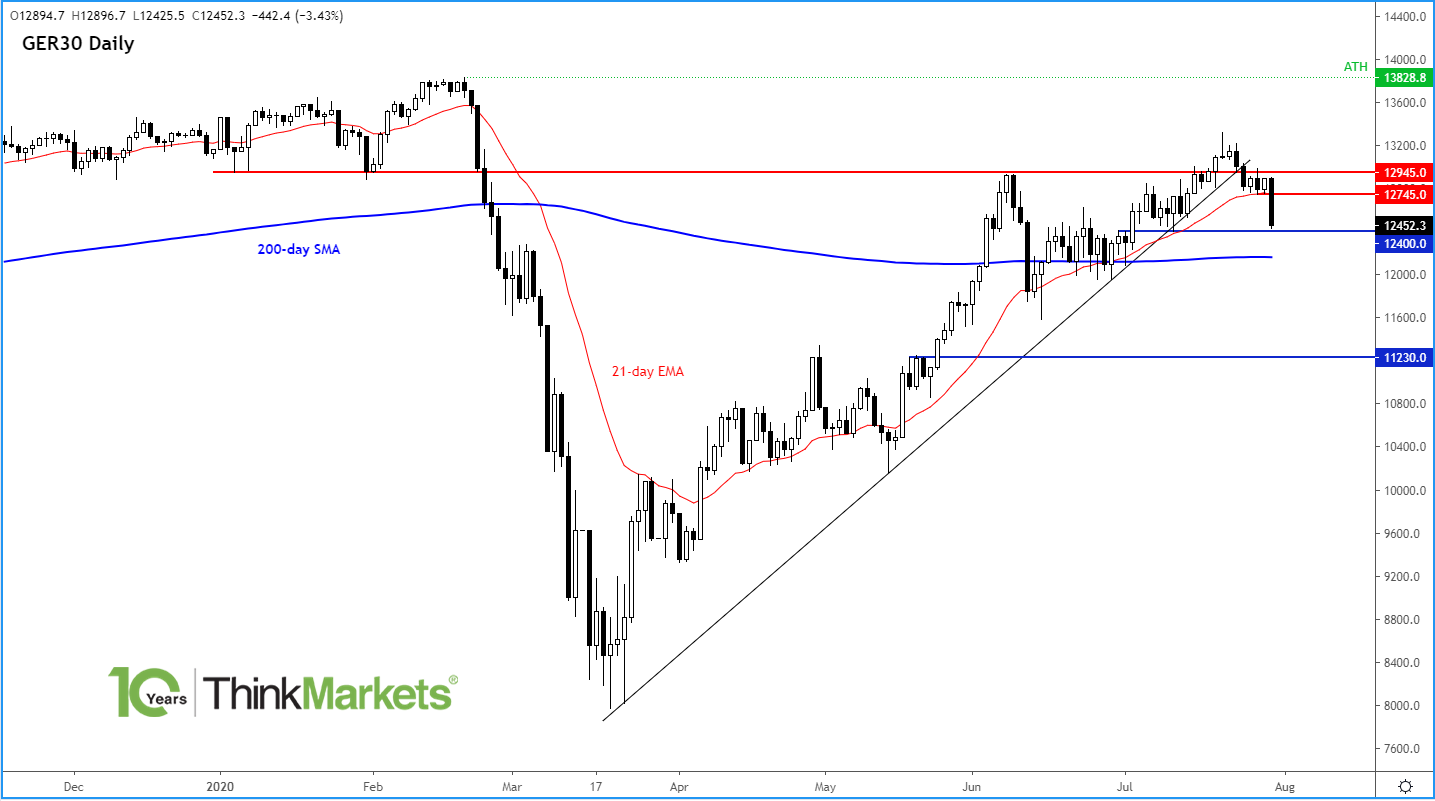

European indices were down between 1.0 to 2.5 percent, with the German DAX taking the brunt of the sell-off following a worse-than-expected drop in German GDP and as Volkswagen unveiled a first-half operating loss and slashed its dividend. However, it remained to be seen how deep the selling would get and whether there will be any downside follow-though in the days ahead, with the prospect of more stimulus and optimism over a vaccine for coronavirus likely to limit the potential downside.

- Undoubtedly, the downbeat sentiment was driven in part by growing concerns over the pace of the global recovery as coronavirus cases continue to rise globally and weigh down on economic activity. The impact of the virus turned out to be more severe for the German economy than analysts had predicted, with GDP showing the European economic powerhouse contracted by more than 10% in Q2. Analysts are also pessimistic about the performance of the world’s largest economy, with US GDP expected to drop by a whopping 34.5% in an annualized format (quarterly change x4) in Q2 following a 5.0% decline in Q1. If the downturn turns out to be more severe than expected, then this should weigh further on risk assets when the data is released at 13:30 BST, when we will also have the more forward-looking jobless claims data. With coronavirus halting the re-opining plans for some large US states in July, the third quarter GDP is unlikely to show a significant rebound either as we will surely find out in a couple of months’ time.

- New daily records for virus cases were reported in the most populous US states of California, Texas and Florida, as well as in Tokyo and Australia, with cases continuing to rise alarmingly in Victoria. Germany reported its highest number of cases in about 6 weeks and worryingly the R has remained above 1.0 for a sixth consecutive day. Mexico, which is set to become the nation with the third-highest number of Covid-19 deaths, reported another 5,752 cases. And China is seeing local infections, with Xinjiang region being the hotspot currently.

- It is also reasonable to expect that the selling has been exacerbated by some investors reducing their risk exposure in what is one of the busiest days of the reporting season, with the big American tech giants Apple, Amazon, Facebook and Google set to report their earnings after the close tonight and following a batch of mixed-bag earnings in Europe:

- Echoing the poor performance in the second quarter, some of Europe’s biggest manufacturers such as Airbus and Safran reported plunging sales as the pandemic hurt activity at factories quite severely. German carmaker Volkswagen saw its shares tumble after unveiling a first-half operating loss and slashed its dividend, while French carmaker Renault also fell sharply as it posted a record loss in the first half of the year. Banks fell with Lloyds slumping 8% in London to the bottom of the FTSE after reporting a larger than expected H1 loss of £602 million. Spain's BBVA saw its shares drop as second-quarter net profit almost halved. Banks have struggled because of low and falling base interest rates, their main source of profit.

- However, not all companies reported bad results. London-listed BAE Systems bucked the trend and it was the top riser in another otherwise bearish day for the FTSE. Royal Dutch Shell trading operations saved them from one of the worst quarters ever for the oil and gas industry. Shell’s adjusted net income was down 82% from the second quarter a year earlier but this was still better than a loss expected by analysts. Like Shell, Total SE posting better results due to its trading gains which offset a slump in oil prices.

- Given the deteriorating virus situation, it is no surprise that Jay Powell yesterday called the economic downturn the most severe “in our lifetime,” as the Fed Chair promised to do everything the central bank can do to drive boost the recovery.

With monetary policy set to remain extremely loose, this should help to keep some stock market bulls happy, especially as scientists get closer to producing effective vaccines and other treatments for coronavirus. But a sell-off like today was almost inevitable given the sharp gains over the previous week amid a deteriorating macro picture. However, if the upcoming earnings results and more importantly earnings guidance disappoint from the big tech companies tonight then we may see a more pronounced sell-off.

Source: TradingView.com and ThinkMarkets

Back