This special report has been written by our in-house analysts, providing a preview for the upcoming quarter.

1. Overview: Key drivers

By Fawad Razaqzada

In Q2, the major US indices hit repeated new all-time highs along with the German DAX and Australian S&P/ASX, while the other mainland European indices climbed to multi-year highs. But the UK’s FTSE and Japan’s Nikkei, as well as the Chinese markets, were more subdued. In FX, the dollar found support in June as the US Federal Reserve turned a little hawkish after it provided hints that tapering QE could be on the cards in the not-too-distant future and after the FOMC projected 2 rates hikes in 2023. This hurt the likes of the EUR/USD and gold, with the latter giving up most of its quarterly gains. Iron ore, crude oil and natural gas bucked the trend as they kept rising amid a tightening market, while other commodity prices, which had also ballooned earlier, deflated as China threatened crackdowns on speculators and released strategic stockpiles. Cryptocurrencies surged initially then went into a bit of turmoil before bouncing back to end the quarter on a slightly positive note in what otherwise would be considered a bearish quarter. Will there be another turn in the tide in the markets as we start Q3?

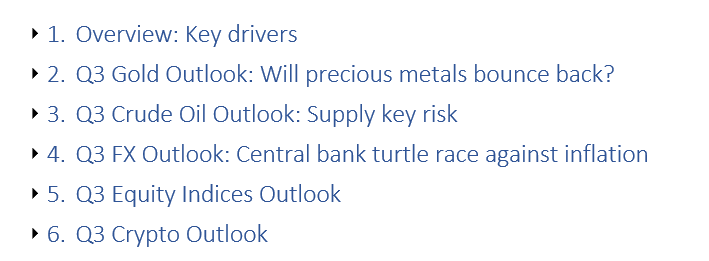

As we begin the third quarter, the attention was once again on lifting of lockdown measures around the world vs. growth of new variants of Covid-19, especially the most infectious, delta. Overall, sentiment towards risk was still very positive as the S&P 500 hit repeated new all-time highs to end Q2. Investors hoped that the acceleration of Covid vaccinations around the world would keep the virus at bay and allow the global economy to grow strongly. One side effect of stronger growth could be high levels of inflation. Price pressures have been building for months. Most economists were expecting inflation to rise further in Q3 with central banks also acknowledging that risk and thus preparing the markets accordingly. But the market seemed convinced that inflation would not accelerate to uncomfortably high levels, for otherwise yields would have already moved sharply higher and stocks lower. Central banks have repeatedly pointed to higher price levels as a result of supply chain disruptions and other temporary factors.

Only time will tell whether the rise in inflation would turn out to be transitory or permanent. One reason why inflation may well come back down is the fact many commodity prices (excluding energy) fell back towards the back end of the second quarter, although this does not necessarily mean they won’t rise again. So, in terms of how risk assets will behave, a lot will depend on the path inflation will take in Q3, as central banks have become data-dependent.

If inflation does not accelerate as sharply in Q3 as some fear, this will allow the likes of the Fed, ECB and BoE to keep their respective policies extra-ordinary loose for months to come. As a result, global equity markets may remain supported on expectations that central banks would keep driving yield-seekers away from bonds and into racier stocks. There will likely be spill over into other markets, including gold and silver, as well as cryptos and other non-interest or low-yielding assets.

2. Q3 Gold Outlook: Will precious metals bounce back?

By Fawad Razaqzada

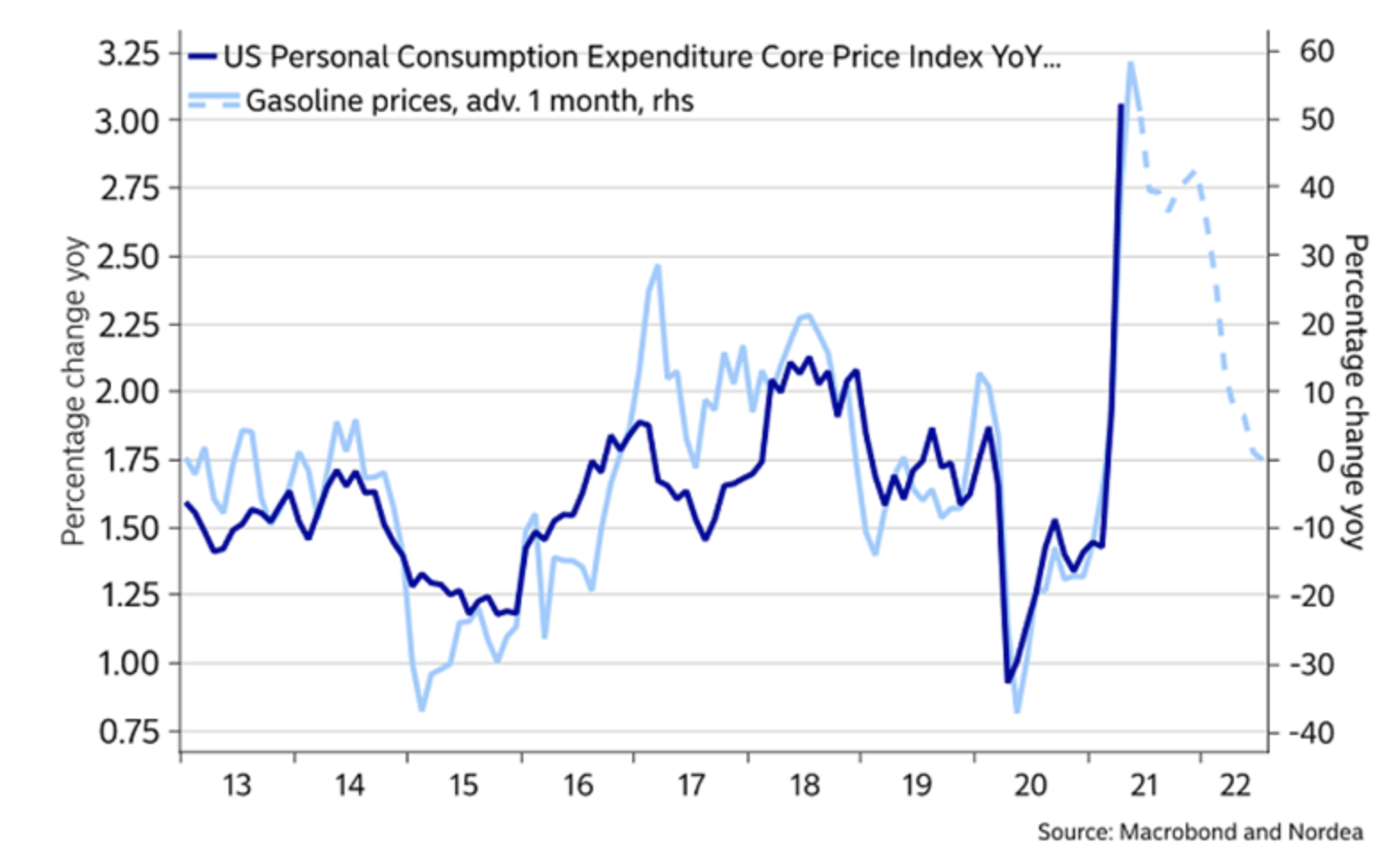

The drop in gold prices in June was attributed to talks about tapering QE having unofficially started at the Federal Reserve. However, this should have been expected by the market even before the Fed’s June meeting. After all, data had been improving for several months and inflation had already shot higher. Another reason why I am still keen on precious metals is this: gold was on the rise before the pandemic, when central bank policy was nowhere near this loose. The metal had hit a high of $1703 in early 2020, before initially selling off and then rebounding sharply with every other risk asset as central banks and governments unleashed record stimulus measures. Now back at around $1760-80 (when this report was written), gold was only $80 more expensive than just before lockdowns started. Is it not reasonable to expect that with vast stimulus measures still in place that gold should be much higher? Of course, you could argue that gold has already gone considerably higher before topping out last August as yields bounced back, so it has done what it should have. Still, the fact that all other major assets classes are holding onto much of their stimulus-driven gains, gold looks massively undervalued in that regard. Gold bulls would also point to seasonality factors, with the yellow precious metal historically doing well during the third quarter.

Gold seasonality favours bulls in Q3:

Source: EquityClock.com

The key risk to my bullish view on gold is if yields were to rise sharply as a result of the major central banks tapering QE sooner and more profoundly than expected. This is unlikely in my opinion.

3. Q3 Crude Oil Outlook: Supply key risk

By Fawad Razaqzada

Crude oil rose further in Q2. The historical turnaround from negative prices last year continued as the market tightened considerably. In the first half, prices have risen about 50%. Will prices rise further in the new quarter or are we finally going to see some consolidation or a pullback? In Q3, the key risk facing oil investors is from the supply side, rather than demand as the latter is likely to be strong.

Oil consumption should improve with major economies having re-opened and with the holiday season upon us, we should see increased air and ground travel. The only caveat is if new, more infectious, variants of Covid-19 emerge, causing renewed lockdowns.

But as prices rise, so will the pressure on the OPEC and its allies to hike output in order to avoid creating unwanted inflation and chocking economic growth. The OPEC+ was scheduled to meet on July 1 to discuss boosting supplies. The coalition was considering whether to continue reviving crude supplies gradually, as favoured by Saudi Arabia, or more vigorously as per Russia’s request. The supply hikes, if there are any, would likely be for August or September. But with no Iranian nuclear deal in sight, and in light of the rising delta variant of Covid (which has raised the risk for weaker demand), this may well discourage the OPEC+ to increase supplies more than expected.

In any case, the pressure will grow on the OPEC+ to hike output later on in the summer, if oil prices do not ease back. If the OPEC decides to ease output steadily as they have been in recent months, then, all else being equal, oil prices may remain supported near their recent highs amid expectations of a tight market. But if the OPEC+ decides to restore production more aggressively, then that could catch the market off guard, leading to a drop in oil prices.

Meanwhile, despite the surging prices and unlike the previous boom cycles, US shale producers have not responded by raising their output yet. This is, in part, because investors have demanded better financial returns rather than production of more crude volume, as well as the fact that the focus has shifted to the production of more renewable energy than relying on fossil. By June, shale output remained about 15% below the January 2020 peak of 9.18 million barrels per day (mbpd). But production levels are likely to rise more robustly later in the year, which may help put a ceiling on crude prices.

4. Q3 FX Outlook: Central bank turtle race against inflation

By Victor Golovtchenko

Central bank response to rising inflation numbers across the globe will be key to the upcoming currency market moves, and no doubt for other markets too.

We have come full circle in the inflation/deflation cycle, and the coming weeks are going to be crucial for the currency markets. There is no country in the world that hasn’t felt the effects of rising prices and the time for reaction from monetary policymakers is nigh. Among the major central banks, the U.S. Federal Reserve and Bank of Canada appear to be the first ones to acknowledge the problem openly, albeit for now Chairman Jerome Powell and his Canadian counterpart Tiff Macklem remain cautious in their approach.

While the

Bank of Canada was the first to highlight high inflation numbers and began the process of reducing its weekly asset purchases, the Board of Governors retained its policy at the June meeting after a CAD$1 billion reduction in bond buying in April. The Canadian dollar has been among the strongest currencies across the G7 over recent weeks, and for the time being, the BOC is only being followed by some rhetoric from the Fed at its June meeting.

Following on the hawkish rhetoric from the

U.S. Federal Reserve, the US dollar regained some ground across the board, closing the second quarter only 150 pips lower against the EUR, after rallying almost 350 pips during the month of June. The strong closing of the quarter signals continued strength for the USD from a technical perspective, while the fundamentals remain strong as other central banks such as the European Central Bank, the Bank of England, and the Bank of Japan continue to remain pat and even dovish (as recently signalled by the President of the ECB, Christine Lagarde).

As a result, I expect the US dollar rally to continue at least throughout the summer months as the market digests the news that the Fed is going to start tapering its asset purchases. Once the pace of asset purchase reduction is unveiled (we expect that to happen at the Fed’s September meeting), USD bulls are likely to pause and reassess their positions depending on the Fed’s pace of asset purchase reduction.

While some other central banks might consider tapering, we don’t expect them to be as forthcoming as the Fed throughout the summer months – especially the

European Central Bank.

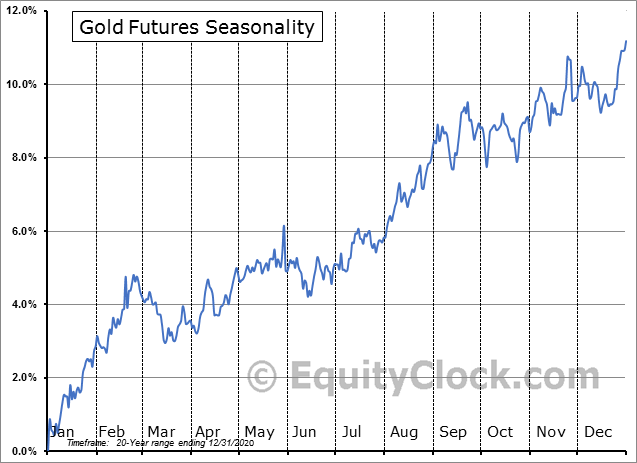

Potential risks to this outlook stem mainly from the spread of the Delta coronavirus variant across North America. While case numbers are rising for the time being, the death toll is much more contained, presumably due to the relatively well executed vaccination campaign. Europe continues to be on track with vaccinations, however the pace of the economic recovery is much slower. Should the recovery pace in Europe increase, the EUR could see a boost, reflecting a change in sentiment.

Another risk for the single European currency stems from a reshuffle in the inflation targeting methodology of the ECB. The Fed has shifted to flexible inflation targeting late last year, signalling that it will tolerate higher inflation rates and an average path for inflation around 2%. If the ECB also diverges from its target of “close to 2, but less than 2%,” to something more flexible, like a symmetrical band on both sides of the 2% figure, the EUR could suffer given weaker price pressures in the Eurozone:

The Bank of Japan

The Bank of Japan remains committed to keep rates lower for longer, especially considering the relatively higher levels of public debt in Japan. A new cycle of weakness for the Japanese yen cannot be ruled out, with the main beneficiary being the US dollar, for the aforementioned reasons related to US monetary policy.

The Bank of England is relatively tame in signalling any prospective action on tapering asset purchases, and with the only board member who’s been voicing a hawkish tune, Chief Economist Andy Haldane, resigning in June, the UK central bank is likely to remain dovish over the summer. That said, should the recovery proceed at an accelerated pace, a change in tone could provide a temporary relief for GBP bulls, who have been firmly in control for the most of 2021.

The Reserve Bank of Australia and New Zealand have been voiceful in signalling their intentions to move on with tapering asset purchases and even signalling higher rates next year, however a pause in rising commodity prices could impact those intentions. Both of these currencies have staged impressive rallies as the pace of price increases of commodities went on for over a year, and a continuation of this trend is likely to keep them supported. That said, with multi-year highs in commodity prices already being printed and China signalling that it intends to take steps to limit input price pressures, commodity currencies could face some headwinds during the summer months.

Overall, the expected theme for Q3 is for the US dollar to retain a bid and continue to crawl higher. As usual, however, the many variables that affect the currency markets can shift quickly and any forecast should be looked upon as a mere possibility, and not a certainty.

5. Q3 Equity Indices Outlook

By Kearabilwe Nonyana

Global stocks ended the second quarter sitting at or near all-time highs. The economic outlook brightened considerably as the vaccination rollouts gathered pace in developed economies, while at the same time central banks refused to give their money printers a rest as QE ran at full throttle.

Interest rate risk environment

Post the global financial crisis, central banks around the world have found themselves in a quagmire having to use unorthodox methods to support the financial economy. Quantitative easing coupled with a low inflationary environment have caused central banks to keep rates low and conduct open market operations to buy government debt at record levels. This has brought down the cost of capital. I foresee the low cost of capital environment carrying on in Q3, even though at the last Federal Reserve policy meeting we saw more hawks rear their heads. Inflation will likely run hot due, in part, to the fiscal support that President Joe Biden has announced for the economy in an infrastructure deal. But it is clear that the composition of the FOMC has more doves than hawks, with policymakers repeatedly suggesting inflation is going to be temporary.

United States

There has been a tug of war on the US indices. Growth stocks, which are majority in the technology sector, have yielded around 12.7% in the previous quarter whilst the DJIA, containing mostly value stocks, is only up about 3.3% for the quarter. The attractive valuations in the value stocks will probably be the next spot that the financial market participants may look at in the coming quarters as the global recovery takes hold and central bank policy remains loose. Upcoming Q2 corporate results will provide us with big clues on the next move for the tech sector.

European Markets

A considerable number of positive factors are impacting European stocks and indices. But towards the end of Q2, a growing list of countries started to impose restriction on travel as the delta variant of Covid spiked. This caused the EU indices and the FTSE to pull back from its highs as industrial and consumer discretionary stocks, which need an open economy to thrive, struggled. I believe these stocks might struggle in the early parts of Q3 if renewed covid restrictions are imposed.

Emerging Markets

Global commodity demand, driven mainly by China, has propelled stock markets in some emerging markets. Chinese tech companies in the next quarter have some of the most value in the growth sector globally and Chinese financials. In Africa, there has been a sizable sector rotation from cyclical miners who benefit from the higher commodity and FX prices to stocks which show value in the battered financial and industrial sectors in the economy.

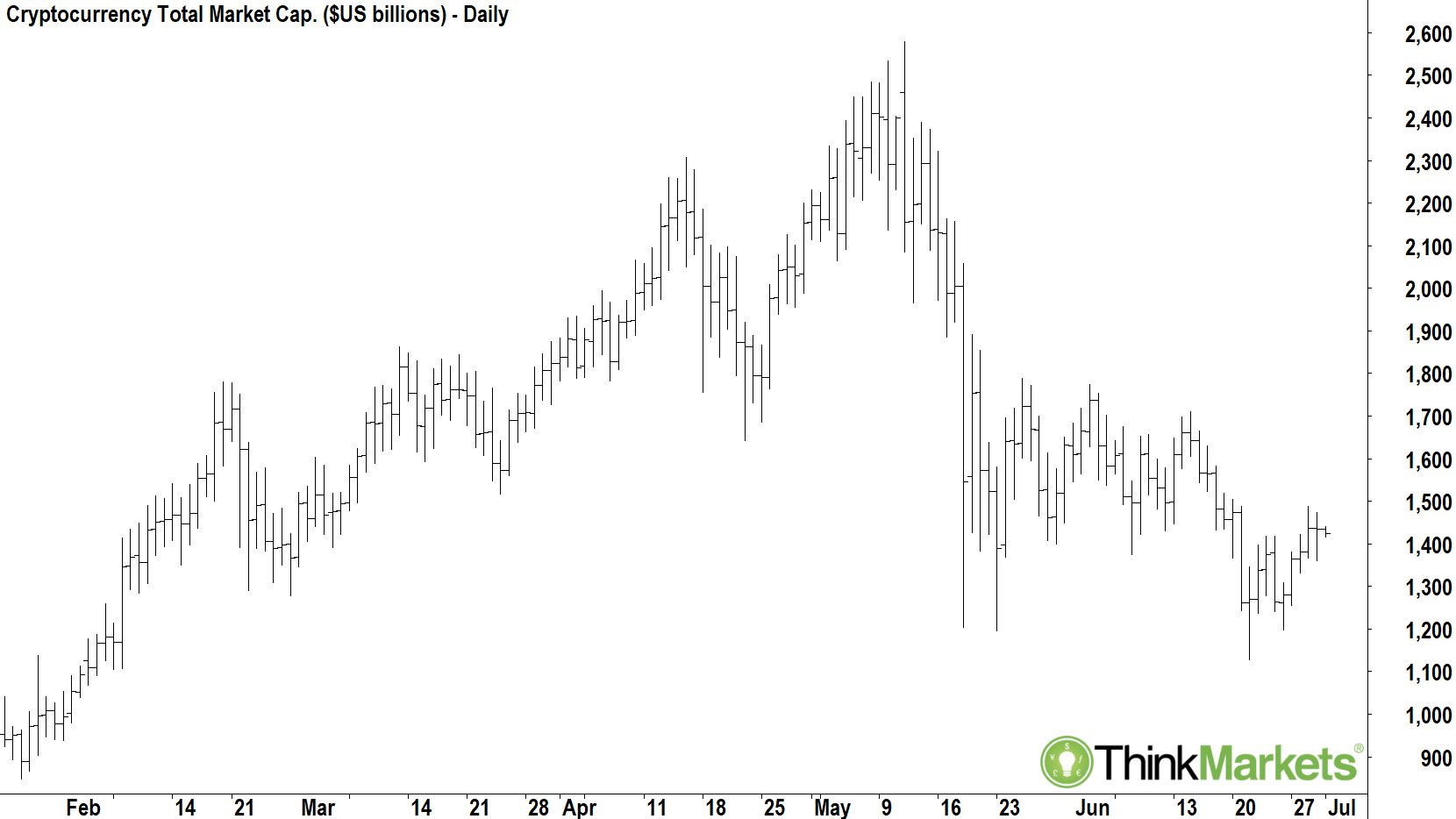

6. Q3 Crypto Outlook

By Carl Capolingua

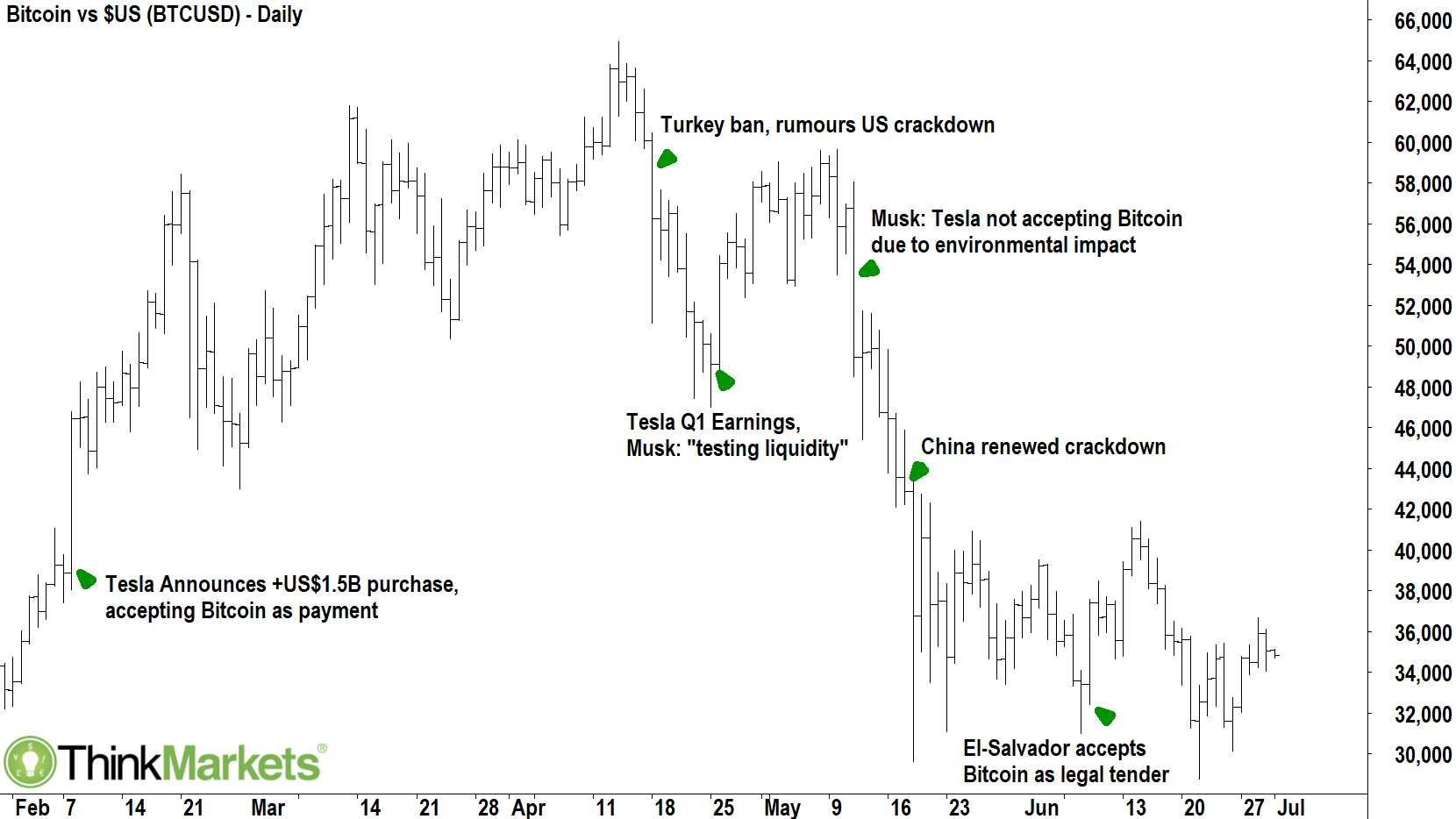

The second quarter was a wild one for cryptocurrencies, but to be fair, the words 'volatility' and 'cryptocurrency' are regularly used in the same sentence! Once again, headlines were dominated by charismatic billionaires, in particular Tesla founder and CEO, Elon Musk. Musk's is perhaps the most influential person with respect to an entire asset class in the history of finance. Certainly, he caused a surge in the prices of Bitcoin and other cryptocurrencies (known as 'altcoins') in February following the announcement that Tesla had amassed a US$1.5billion holding in Bitcoin and the company would also accept it as payment for Tesla vehicles. But, in late April, Tesla's first quarter earnings report made public that the company had sold US$272 million worth of its Bitcoin holdings, reaping a tidy profit on the sale. Shortly before this announcement, Bitcoin prices had plunged from record highs around US$65,000 to just under US$50,000 after Turkey banned all payments in cryptocurrencies, and rumours swirled that the US was on the verge of doing the same. The selloff abated somewhat after Musk justified the Tesla sale by tweeting, "Tesla sold 10% of its holdings essentially to prove liquidity of Bitcoin as an alternative to holding cash on balance sheet".

It has been an eventful second quarter for Bitcoin and for cryptocurrencies in general…

It has been an eventful second quarter for Bitcoin and for cryptocurrencies in general…

From the extraordinary to the ridiculous: Thank you Elon!

If the above sounds extraordinary, then things went from extraordinary to ridiculous just a couple of weeks later on 12 May. This is when Musk announced in another tweet that Tesla would no longer be accepting Bitcoin as a means for transactions as he was "concerned about rapidly increasing use of fossil fuels for Bitcoin mining and transactions, especially coal, which has the worst emissions of all." The backflip caught the market by surprise, and Bitcoin prices tumbled from around US$58,000 to as low as $29,641 over the course of the next week. There was good reason for the market to be surprised, disappointed, and probably even a little baffled by Musk's change of heart. At the time of his backflip, Musk was certainly no 'Newb' to Bitcoin or its protocol which uses a 'proof of work' consensus mechanism to add new blocks of transactions to the Bitcoin blockchain. Proof of work is long well known to be an extremely energy intensive process, and Bitcoin 'mining', which is the term associated with the proof of work process, uses a similar amount of electrical power to Argentina or the Netherlands. Various think-tanks estimate that approximately 60-70% of Bitcoin mining done is using non-renewable sources of energy, mainly coal. Musk noted that he would only reconsider Bitcoin, or other cryptocurrency alternatives for that matter, if they "use <1% of Bitcoin's energy/transaction."

Every Doge will have its dayor monthbu t maybe not a whole year

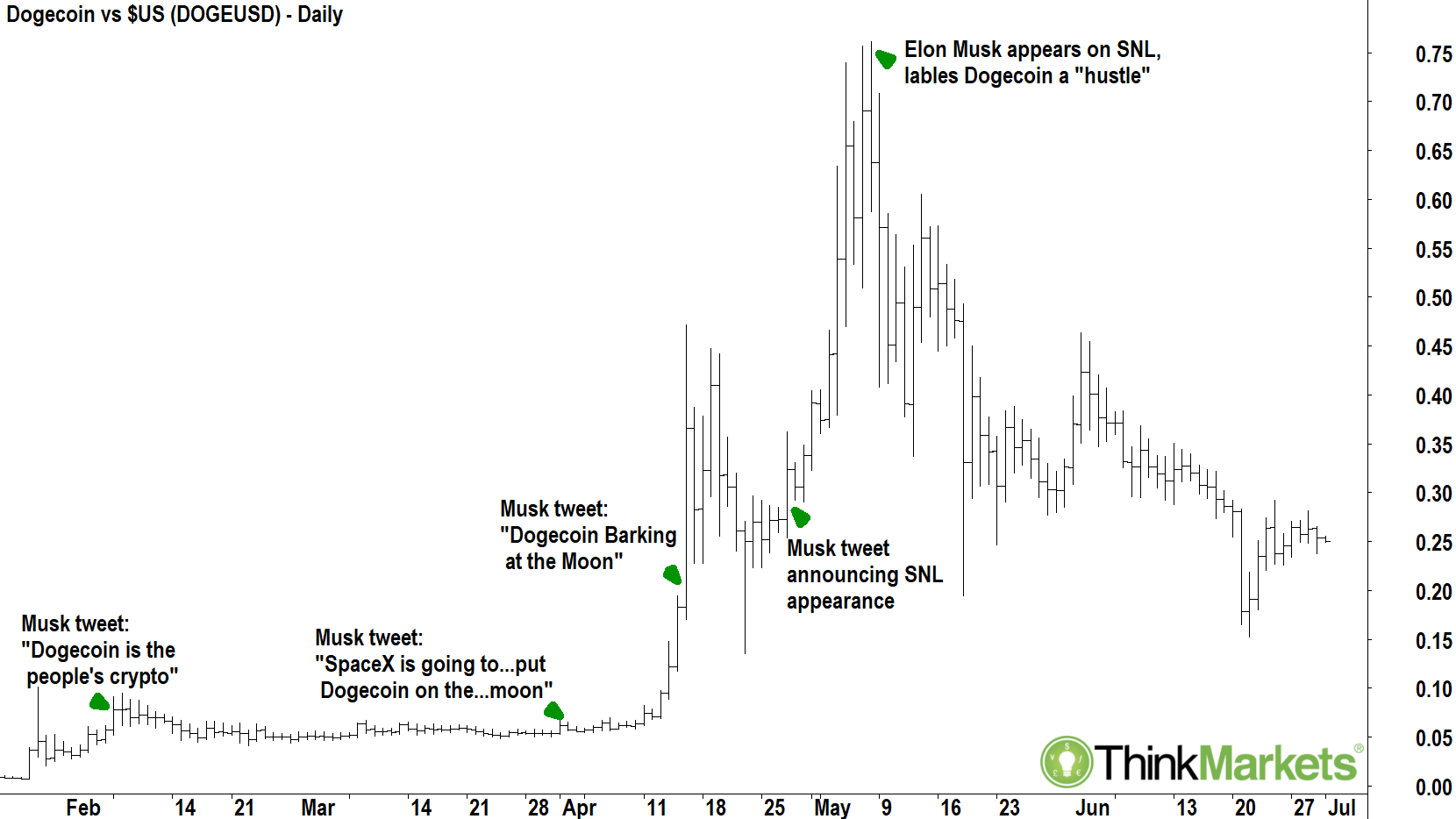

Many cryptocurrency commentators speculated that Musk's backflip on bitcoin had much to do with his support for popular memecoin Dogecoin. A 'memecoin' is a cryptocurrency that was created as a joke and typically does not have any real-world usage case. Dogecoin, or 'Doge', is arguably the original memecoin, and on 4 February it spiked over 60% as Musk tweeted "Dogecoin is the people's crypto". Musk's involvement in Doge steadily increased from there as he went on to declare himself the 'Dogefather'. This spurred an explosion of the 'Doge Army' (i.e., Doge supporters) who pumped themselves into a buying frenzy via social media pushing the price of Doge higher again. As the price exploded, both social and regular media abounded with reports of overnight Doge millionaires. This fed the frenzy even more until prices eventually spiked into Musk's appearance on comedy television show

Saturday Night Live (SNL) on 8 May

. By that point, the Dogecoin had worked its way into fourth place in terms of market capitalisation on the cryptocurrency leader board. At just under $US100 billion market capitalisation, this self-proclaimed joke was worth more than the market capitalisations of major US companies Twitter and Kimberly-Clark

combined. During one of the skits in his episode of

SNL, Musk appeared as a professor attempting to explain Dogecoin to a reporter. After failing to do so, the reporter asks Musk's character, "So it’s a hustle?" to which Musk responds: "Yeah, it’s a hustle". This admission did not bode well for the Doge Army, and perhaps ironically, Musk's

SNL appearance also coincided with the exact high for Doge prices at around US76 cents. In a classic 'buy the rumour, sell the fact' debacle, Doge prices subsequently crashed in the following few trading sessions to just under US20 cents. Still, that's not bad considering that one Dogecoin cost just half a US cent at the start of the year!

Elon Musk has inspired a new generation of crypto hopefuls, turning some of them in to overnight millionaires…

Elon Musk has inspired a new generation of crypto hopefuls, turning some of them in to overnight millionaires…

Green altcoins succumb to one-two crypto punch

Back to Musk's

Bitcoin shenanigans! They certainly confused cryptocurrency investors, and they also had a significant negative impact on the broader cryptocurrency universe as other proof of work-reliant blockchains were caught in the selloff. However, for a short period, blockchains reliant on other consensus mechanisms such as Cardano (ADA) and Polka Dot's (DOT) 'Proof of Stake', and Solana's 'Tower Consensus', actually benefited from Musk's so-called Bitcoin greening crusade. Each of these other consensus mechanisms use just a tiny fraction of proof of work's energy footprint as neither requires computers supporting the network to solve complex cryptographical puzzles in order to win the race to add the next block of transactions to the blockchain, thus winning any associated transaction fees and cryptocurrency rewards. The surge in non-proof of work cryptocurrencies was short lived however, as a couple of developments on opposite sides of the Pacific rocked the cryptocurrency market to its core, and further exacerbated the new downtrend in prices sparked by Bitcoin's environmental impact debate.

Firstly, on 7 June, US law enforcement agencies announced they had recovered the majority of the US$4.4 million ransom paid to the perpetrators of the ransomware attack on the Colonial Pipeline in May. They did not disclose how they had effectively 'hacked the hackers' by successfully identifying what most in the cryptocurrency world thought were anonymous and untraceable transactions. One of the major drawcards of cryptocurrencies for both proponents and hackers alike, is the anonymity of users, and the ability to transfer wealth instantaneously without the assistance of traditional financial institutions. But, the success of US law enforcement in recovering the Colonial ransom significantly undermined this theory, and also demonstrated that Bitcoin's transactions, whilst anonymous, are still very traceable.

The 'two' of the 'one-two post-Musk punch' was China's renewed crackdown on cryptocurrency use and on cryptocurrency mining operations within Mainland China. Prior to this crackdown, approximately two-thirds of global mining activity for Bitcoin occurred on the Mainland. Roughly just over half of this mining used non-renewable sources of energy, mainly coal. The impact of the crackdown was two-fold, firstly it resulted in an almost-overnight exodus of Chinese cryptocurrency exchanges to other jurisdictions, and correspondingly, those exchanges ceasing services to Mainland Chinese customers. Secondly, miners were also forced to relocate, with most estimates now believing that as much as 90% of mining operations within China's borders have ceased.

Q2 was certainly eventful for cryptocurrencies, but are we facing another boom and bust cycle like we saw in 2017?

Q2 was certainly eventful for cryptocurrencies, but are we facing another boom and bust cycle like we saw in 2017?

These developments no doubt triggered a degree of selling from Chinese retail holders of cryptocurrencies, but likely also from the substantial holdings of Chinese miners as well. The costs of relocating their operations to other jurisdictions varies from 'comparatively small' for miners who moved to neighbouring countries such as Kazakhstan, to 'comparatively large' for miners moving to Western countries with stronger rule of law and larger renewable energy reserves such as Canada and the USA. Many miners were forced to sell down their Bitcoin holdings in order to fund their relocation costs, and this most likely put further pressure on Bitcoin and altcoin prices. In the period from the Turkey ban, to then end of the second quarter, the value of all cryptocurrencies has fallen by a staggering US$1.1 trillion, or roughly 44%.

Technical analysis vs the Volcano

So we enter the third quarter of 2021 at somewhat of a cross-roads for cryptocurrency in general. There remain a number of high profile proponents of the space such as Microstrategy CEO Michael Saylor, Twitter founder Jack Dorsey, and hedge fund investor Cathy Wood, but just as many detractors including legendary stock investors Warren Buffet and Charlie Munger among others. The price of Bitcoin seems to reflect this, having found a base around the US$30,000 mark it has struggled to decisively break back into the $40,000's. Both the long term and short term trends appear to have turned lower (pink and orange zones), and appear to be impeding movement to the upside. The fact that no less than five probes of the US$30,000 support level have so far held is encouraging, and it speaks to the faith that the Bitcoin true-believers have in setting this point as a concrete long term low. Interestingly, perhaps the biggest of these rallies occurred when El-Salvador announced that it would be accepting bitcoin as legal tender alongside US dollars. Also, that it would look to become a hub of Bitcoin mining using geothermal power from its volcanos, thus assisting in the greening of the beleaguered crypto. Certainly, adoptions such as these are helpful in convincing the mainstream that Bitcoin has a long term future as a store of value and a unit of exchange.

US$30,000 is the key support point for Bitcoin, but can it continue hold?

US$30,000 is the key support point for Bitcoin, but can it continue hold?

The question however, is if there will be enough good news flow of this type to more than balance out the short-to-medium term overhang in supply from Chinese miners and from hedge funds following the new downtrend. As continued selling pressure is applied, one expects that the longer we go without a US$40,000 handle, eventually support is going to crumble and give way to a sharp move towards US$20,000. I would expect that this level would also be a significant support point, as it coincided with the 2017 high, and the most recent move's major breakout. But, only time will tell.

If you thought Q2 was a doozy…

The proponents of cryptocurrencies beat their drum saying that recent weakness in prices is only temporary as the Chinese crackdown plays out, and that it represents a major buying opportunity. Further, they believe that we are only at the beginning of a revolution in how we think about money, and that cryptocurrencies are going to change forever how we pay each other, how we do business, and how we interact with the financial system. Better still, anyone, anywhere can participate on a fair and level playing field free from central bank meddling. Certainly, there are a number of exciting projects in the space such as Ethereum 2.0, Cardano, and many others, which seek to transform cryptocurrencies from simply a store of value or unit of exchange, into a complete decentralised financial ecosystem. And then there will always be the Doge's of the cryptocurrency world, which are there simply for 'fun'! One thing is for sure, we'll no doubt have plenty to talk about in our Q3 update!

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.