EU

EU

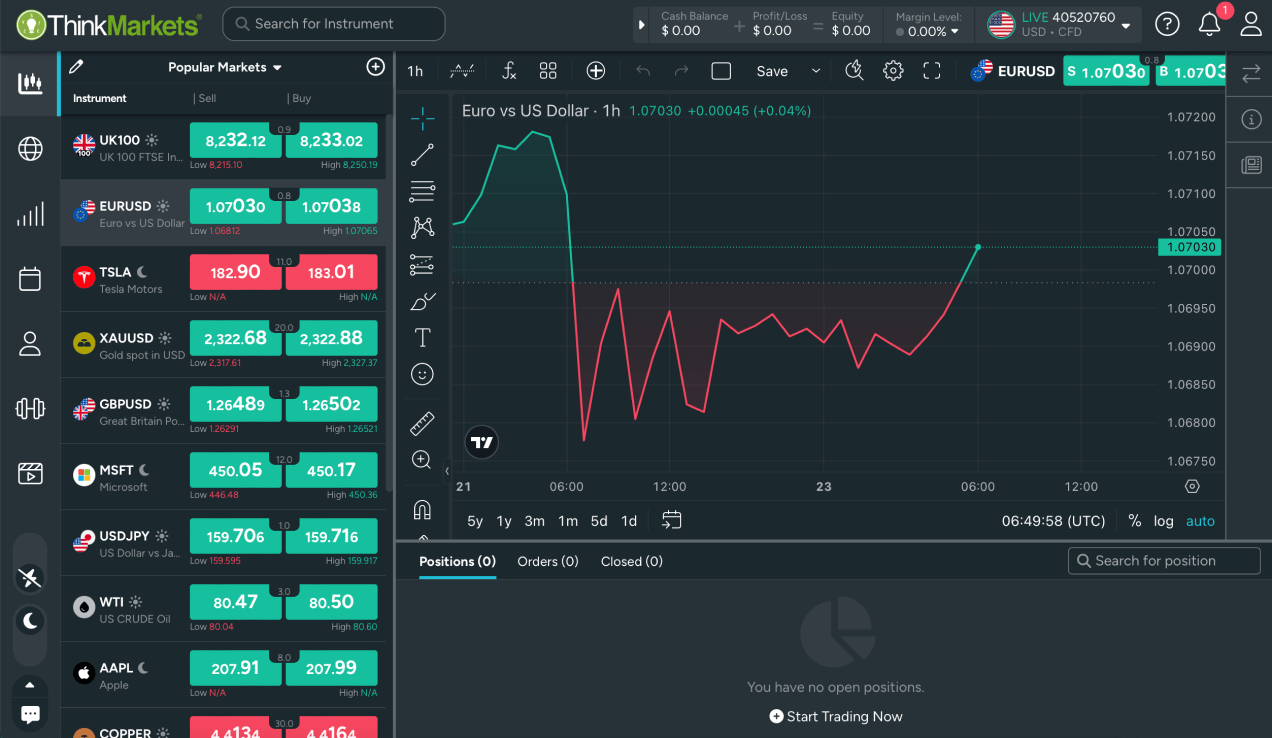

ThinkTrader

Where innovation meets efficiency

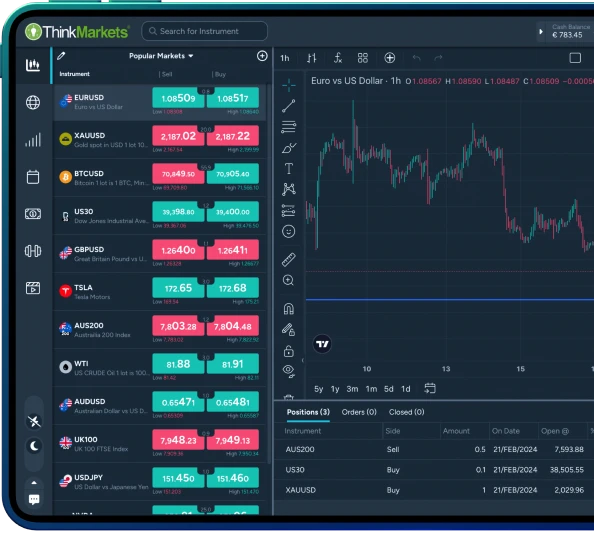

Trading View charting

120+ indicators and 19 chart types

120+ indicators and 19 chart types

Innovative tools

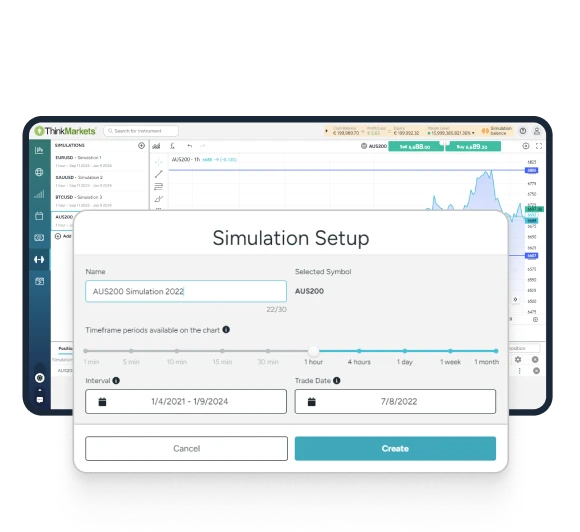

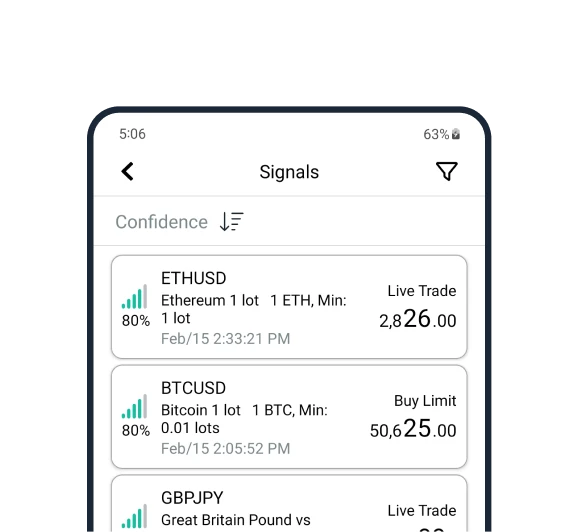

Signal Centre and Traders’ Gym

Signal Centre and Traders’ Gym

Valuable insights

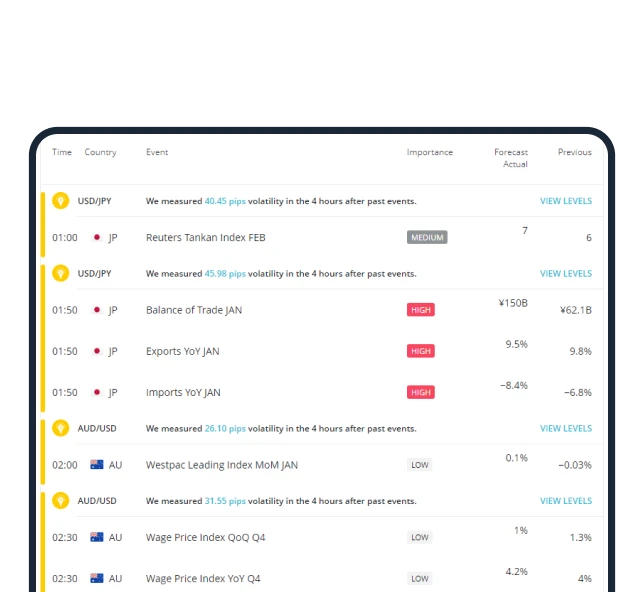

Real-time data and updates

Real-time data and updates

User-focused experience

Intuitive UI and streamlined trading

Intuitive UI and streamlined trading