In the weeks ahead, sentiment towards stocks will likely remain positive, especially in Europe. With a Brexit deal secured and COVID vaccines being rolled out (with relative success in the UK), investors are likely to look through the short-term economic risks arising from the current lockdowns. In fact, there was a bit of good news for a change as the number of people catching the virus fell in the UK, albeit from exceptionally high levels. The so-called R rate was estimated to be between 0.8 and 1 on Friday, meaning the outbreak is now shrinking if the official estimates are correct. But there is still a long way to go. Lockdowns are unlikely to end until deaths start falling and in any case until more people are vaccinated, especially in the high-risk category. This will probably keep the upside limited for risk assets.

3 factors to watch in the week ahead:

- Corporate earnings – especially from tech giants

- Macro data

- Bond yields

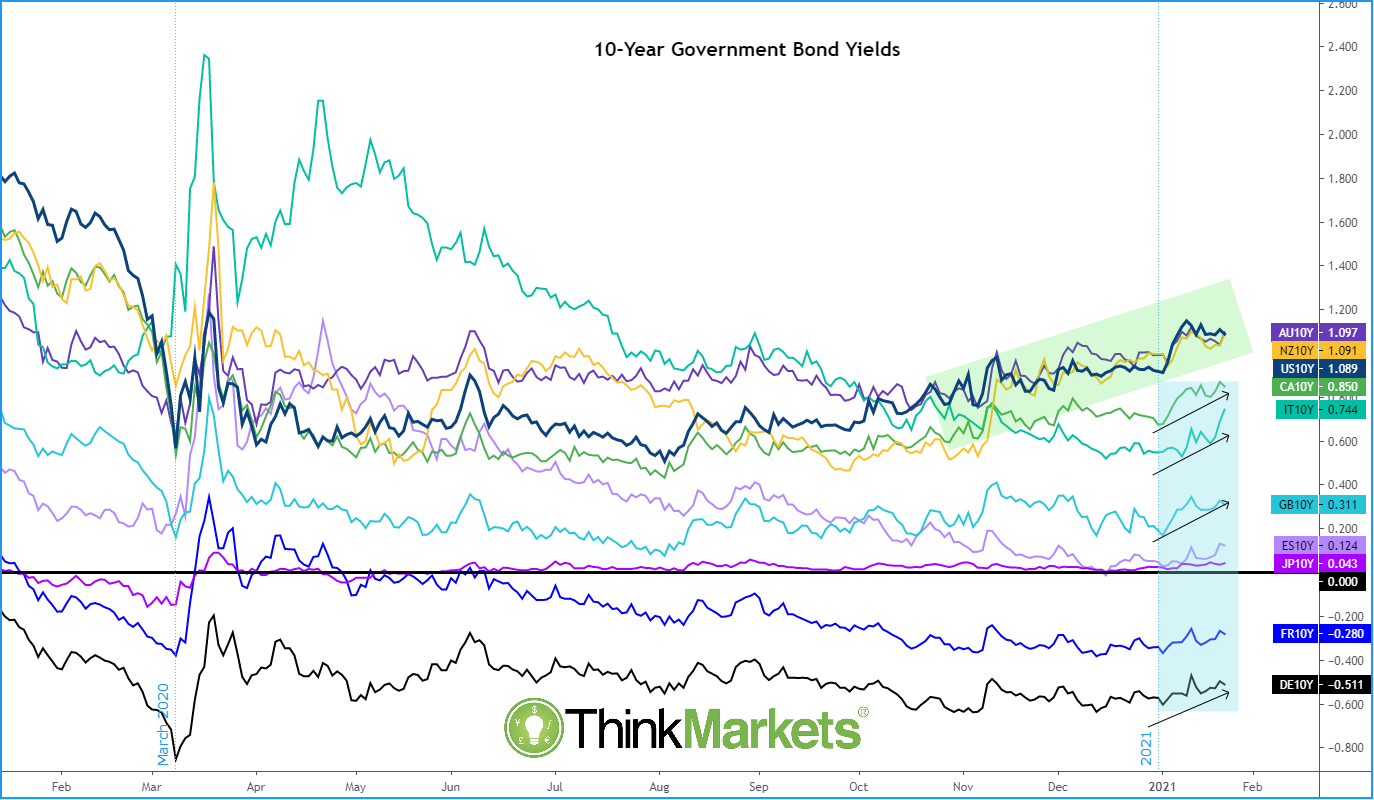

Keep an eye on bond yields

There has been a subtle upwards shift in benchmark 10-year government bond yields since the start of the year. Specifically, it has been the European yields starting to catch up after yields in US, Australia and New Zealand had all started to perk up from around November.

The rising yields in Europe suggest bond market investors are no longer expecting any further stimulus from the European Central Bank. This makes some sense as the ongoing vaccine rollout means the pandemic and lockdowns can, hopefully, be declared over at some point later this year. We have also secured a Brexit deal while a massive European Union fiscal package is forthcoming. The need for the ECB to continue offering as much support is thus diminishing. This should mean higher yields from here.

For investors, the key concern – for the lack of a better word – is that the ECB’s slower pace of purchases of government debt, potentially causing yields to rise further, may put upward pressure on the euro. This, in turn, could weigh on inflationary pressures and hurt Eurozone exports.

However, to suggest bond yields will stage a sharp rally – or bond prices will sell-off sharply – is very premature. While yields can stabilise further, it is worth remembering that they sit near historically low levels and central banks will be keen to keep them low for a long time to come.

In other words, conditions remain ripe for equities to continue outperforming, especially if the rollout of vaccines, or removal of the lockdowns, happen faster than expected. For FX investors, the positive signals from the equity market will likely keep haven currencies depressed, allowing the likes of the euro and pound to following the commodity dollars higher.

Corporate earnings galore

There will be plenty of fourth quarter corporate earnings results to keep stock market investors busy in the week ahead. Among others, we will hear from big tech giants Microsoft, Apple and Tesla, as well consumer stocks, providing us invaluable insights about the health of consumer and business spending.

Here are the earnings highlights for the week ahead:

- Tuesday: AMD, Microsoft, Starbucks, Johnson and Johnson and GE, among others

- Wednesday: Apple, Tesla, Facebook, Boeing and Sina Corp

- Thursday: Visa, Mastercard, McDonalds and American Airlines

- Friday: Chevron and Caterpillar

Economic data highlights

While the earnings calendar is quite busy, there is not a lot on the agenda for macro investors. Still, there are a handful of macro pointers to keep a close eye on. Here are the highlights:

- Monday: German ifo Business Climate

- Tuesday: UK Claimant Count Change and Average Earnings Index

- Wednesday: German GfK Consumer Climate and FOMC statement and press conference

- Thursday: US Advance GDP (first estimate), unemployment claims and New Home Sales

- Friday: Flash GDP estimates from France and Spain; German unemployment; US personal spending and income

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

Learn and earn more today.

Visit our Education Centre