Here is our week ahead preview for the week commencing 13 July 2020.

This week has been quite choppy for the major indices, good for bonds, bad for yields and the dollar, and therefore great for base and precious metals, with gold topping $1800 for the first time since 2012 and silver climbing to $19. Meanwhile the major stock indices – ignoring the mighty Nasdaq, which again hit repeated new all-time highs – rallied sharply at the start of the week, tracking the big gains seen in China, before drifting lower in mid-week, and then rebounding again on Friday as risk sentiment remained overall positive heading towards the weekend, and ahead of a big week for earnings and economic data. Investors again ignored the spikes in Covid-19 cases in many US states and local shutdowns in other parts of the world after the re-emergence of the virus. Instead, they welcomed falling death rates and the relaxation of lockdown restrictions for example in the UK and other European countries.

Week Ahead

The economic calendar for the week ahead is filled with top-tier macro data and central bank meetings, which should make it a busy week for FX traders. Stock investors will also be busy as the US earnings season kicks into a higher gear, with large banks and some tech names set to report their results.

Key data and earning releases to watch:

Tuesday:

- Chinese trade figures

- UK monthly GDP as well as construction output and industrial production

- Eurozone industrial production and ZEW surveys

- US CPI

- Key earnings: JP Morgan, Wells Fargo and Citi

Wednesday:

- BOJ and BOC policy decisions

- UK CPI

- US industrial production and crude oil inventories

- Key earnings: eBay and Goldman Sachs

Thursday:

- New Zealand CPI (quarterly)

- Australian employment data

- Chinese GDP, IP and retail sales

- UK earnings and claimant count

- ECB

- US retail sales and unemployment claims

- Key earnings: Netflix, Johnson and Johnson, Bank of America and Morgan Stanley

Friday: UoM Consumer Sentiment

So, after a quiet Monday, investors will be bombarded with data and company results in the week ahead. It is impossible to predict the impact of these macro and micro numbers on the markets, but what we want to see is the general trend of the data and earnings. If the economic data continue to point to a speedy recovery, then risk assets should be able to extend their gains. If the numbers are not so great, then we may see a reverse in the bullish trend. Individually, the data releases from each country will unlikely have too much impact as the focus will be on the trend of the data and on the “risk on, risk-off” trade.

Meanwhile upcoming bank earnings will highlight exactly how the lockdown and low interest rates have impacted lenders’ top and bottom lines. Recently, banks and other cyclical stocks have joined the rally on rising optimism over the recovery. However, if their earnings fail to match expectations and company CEOs provide bleak earnings forecasts, then reality might hit and their shares could fall sharply, dragging lower some of the major indices with them.

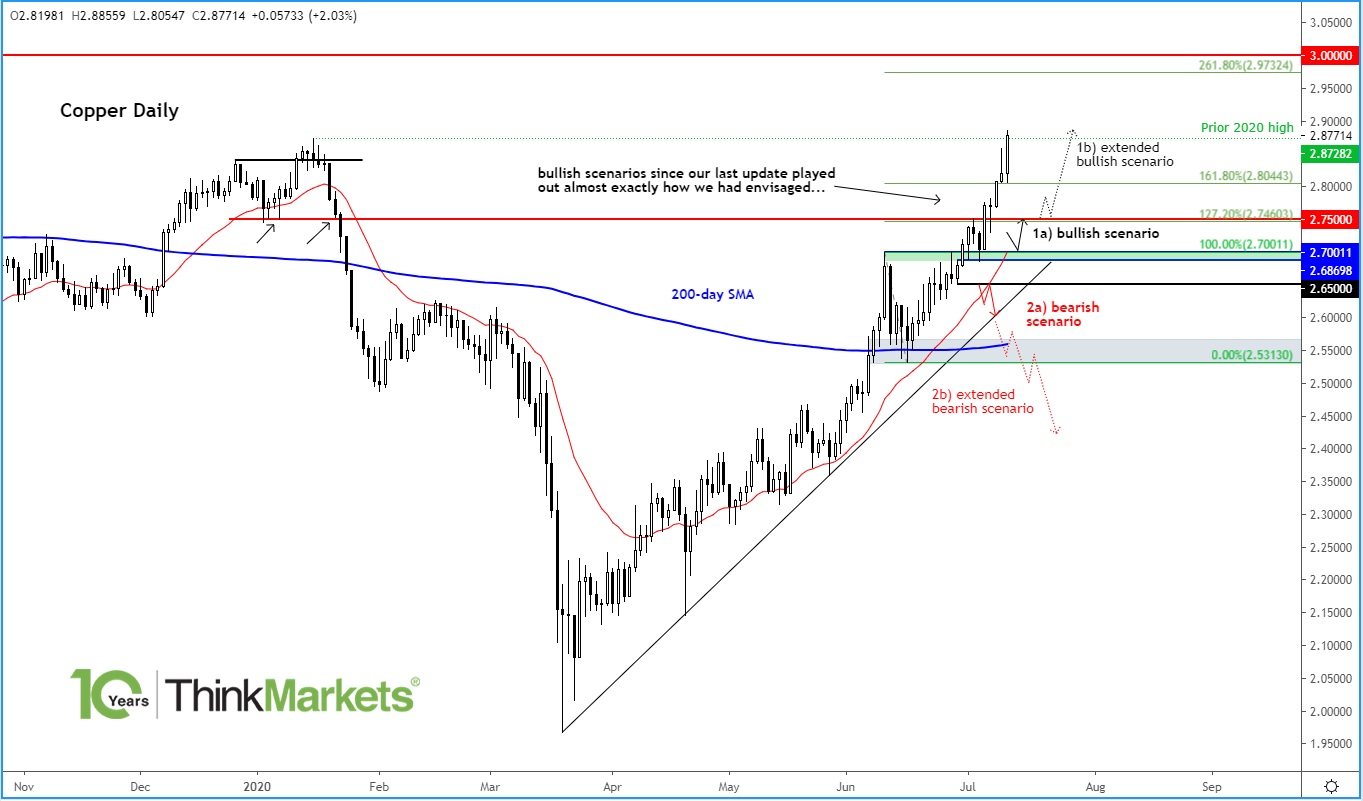

Chart to watch: Copper

With lots of Chinese and other macro numbers to digest next week, base metals and other assets sensitive to changing economic conditions will be in focus. This brings copper into greater focus. To say that copper’s rally has been impressive from the March lows is an understatement. There are two major reasons behind the sharp gains for the base metal, namely 1) optimism over a sharp economic recovery and 2) supply fears.

As mentioned, part of the reason behind the rally is a reflection of investors’ growing optimism over a sharp economic recovery, the same reason which partly explains why equities, especially in China and US, as well as crude oil have also been rising. These expectations are boosted by central bank stimulus and large government fiscal spending, the like of which many developed and some developing economies such as China have not seen for a very long time. Investors hope that the vast fiscal and monetary stimulus will spur growth as lockdown eases around the world, buoying copper demand.

In this regard, copper faces a key test in the coming week. The upcoming data release, especially those from China, need to be positive to support copper and other base metals’ prices further. In the slightly longer-term outlook, it will be interesting to see how copper will fare when supply fears ease. Output in Chile, for example, which is one of the largest copper producers, is under threat because of the pandemic. The country is currently in number 7 spot for Covid-19 infections.

From a technical point of view, Copper has played out the bullish scenario case almost exactly how we had envisaged in

THIS report a few weeks ago. On Friday it hit a new high for the year, thus ending all its Covid-related losses. Here is the updated chart:

Source: TradingView.com and ThinkMarkets

If it wasn’t for supply fears, the rally would have unambiguously pointed to economic expansion. But in this case it is difficult to say what exactly it indicates. Incoming data must remain positive as supply fears ease, otherwise there is a risk prices could collapse again. But for now, the path of least resistance is to the upside and the dips should be supported until something fundamentally changes.

Back