After Wall Street stocks recorded their best quarter since 1998, European markets and US index futures started Q3 with a whimper as profit-taking hit indices in this first half of the day, despite the publication of largely better-than-expected Eurozone data.

Investors are looking forward to publication of key data from the US for short-term direction, as the focus shifts to the world’s largest economy in a shortened-trading week with the Independence Day holiday on Friday. The ADP report was published a few moments ago, showing a 2.37 million increase in private sector nonfarm payrolls compared with 2.9 million expected. Although this is clearly good news, it remains to be seen whether there will be a corresponding increase of this scale in the official nonfarm payrolls report, due out on Thursday, as the ADP is not always a reliable indicator for NFP. Ahead of the NFP, the ISM manufacturing PMI will be published later this afternoon at 15:00 BST, along with Construction Spending, followed by Crude Oil Inventories at 15:30 and FOMC Meeting Minutes at 19:00.

Investor head into an uncertain Q3

Going into the third quarter, the markets face more uncertainty. There is the potential for a new wave of coronavirus to emerge, even though the first wave is far from over given the situations in the US and Latin America. Stock investors will find out exactly how the lockdown hit company profits, with the second quarter reporting season soon to kick off. Then there is the ongoing trade friction between the US and China to deal with, not to mention other geopolitical risks. Meanwhile, the impact of vast stimulus programmes announced by governments and central banks during the height of the pandemic will diminish.

So, given all these risks, I think is unlikely we will see another impressive quarter for equities, even as easing of lockdown measure should boost economic recovery.

The only caveat I can think of is if the economic recovery accelerates sharply, which is not impossible given the huge stimulus programmes. In fact, incoming data since the peak of the pandemic suggests the economic recovery is happening at a faster pace than expected. We have seen, for example, record jumps in US employment and retail sales already. But the key question is whether there will be follow-through in the improvement of incoming data over the next few months, as those jumps were from historically low bases.

Eurozone data improves further

The publication of better-than-expected Eurozone data this morning suggests the single currency bloc is starting to shake off the Covid-19 slowdown, with German numbers looking quite decent.

Although the German unemployment rate hit a five-year high of 6.2% as unemployment rose for the third straight month, the 69,000 increase in job losses were well below 120,000 expected and May’s 238,000 print.

Earlier in the day, a big jump in retail sales provided more evidence of improving conditions at the Eurozone’s largest economy as German shoppers went on a post-lockdown spending splurge in May, driving sales up by a record 13.9% from the previous month. This was much better than 3.5% expected and more than made up for the 6.5% drop in April.

The downturn in Eurozone’s factories also eased sharply in June, according to the purchasing managers’ indices. Spanish manufacturing PMI improved sharply to 49.0 from 38.3, beating expectations of 45.2. Eurozone, German and French PMIs were unexpectedly revised higher to 47.4, 45.2 and 52.3, respectively.

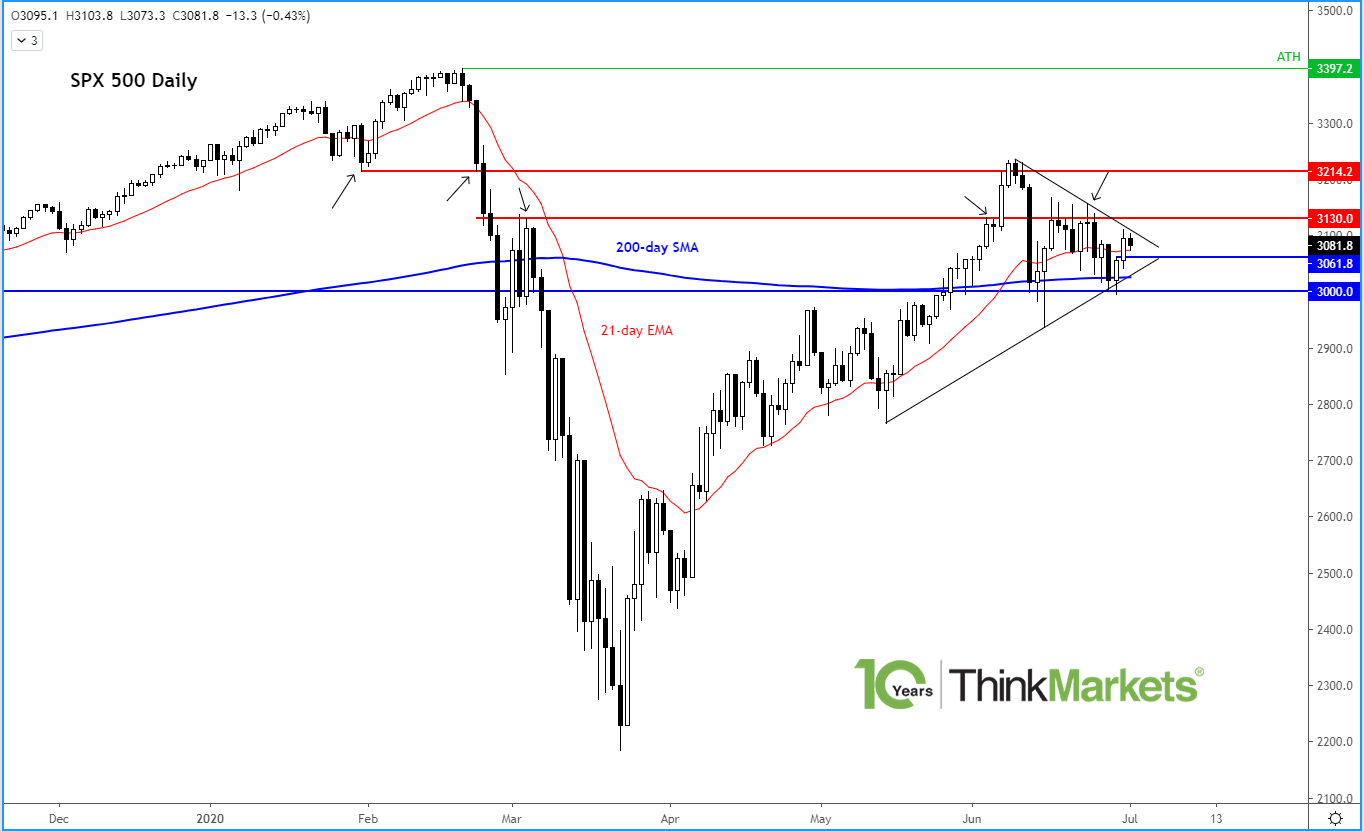

S&P 500 breakout or breakdown imminent

Despite today’s weakness, the S&P 500 remains in a consolidation zone as per the chart, so it could still continue pushing higher:

Source: TradingView and ThinkMarkets

What I am wating for now is a clean break above the bearish trend line or below the bullish trend of the consolidation pattern. While it is contained in this zone, I don’t have too strong a view on the direction given the above fundamental considerations.