- Will inflation concerns replace growth optimism?

- Big Wall Street banks set to report Q1 earnings

- US inflation data tops busier economic calendar

- Coinbase IPO

After what has been a low key and holiday-shortened week for the markets, things should pick up in the weeks ahead. As well as a busier economic calendar, US corporate reporting season will kick into a higher gear with the release of big bank earnings. We may well see some volatility after the S&P 500 hit repeated new all-time highs on falling volumes. The key question going into the earnings season is this: Will company CEOs mirror investors’ optimism on economic outlook, or will they provide more subdued forecasts? And what about the US dollar? After ending the first quarter on the front-foot, the start of Q2 has seen the dollar weaken against most major currencies. The underlying bullish trend could resume for the buck, especially against currencies where the central bank is comparatively more dovish than the Federal Reserve, or regions where the vaccinations have been slower than in the US.

Until now, investors have been quite happy to be buying any dips in equity markets amid growth optimism and despite rising inflationary pressures and valuation concerns. Covid vaccinations continue at a very good pace in the US and UK, while the eurozone is lagging behind but some reports suggest authorities there are going to ramp up their efforts - which is why the euro has shot up this week.

Taper talks could resurface

One source of concern that has not materialised yet but may come back to haunt investors in the near future is the potential for inflation to overshoot as a stimulus-fuelled economy recovers from the pandemic. So far, investors seem to think that the Fed will see through any short-term price pressures as there is plenty of spare capacity left in the economy. After all, stronger economic growth should boost earnings and revenues of US companies. So, “why sell?” is what some investors would be thinking.

At some point, sky-high valuations will come back to the forefront, especially when the Fed plans to slowly withdraw stimulus. This could happen for example if inflation turns out to be longer lasting rather than a temporary shock. But policy makers at the Fed don’t think that is going to the case any time soon. They have suggested there are no imminent changes to be expected in monetary policy, according to the FOMC’s last meeting minutes. They think it will likely be "some time" until substantial further progress is made towards the maximum-employment and price-stability goals.

Inflation data eyed

This means that for now, the stimulus programme of buying assets worth $120 billion per month will continue. However, with the March employment report surprising to the upside, combined with signs of rising inflationary pressures, and not to mention the faster pace of vaccinations and fiscal support, the Fed may want to ease off the gas sooner than expected as the economy potentially heats up faster. They wouldn’t want to overcook inflation and then apply the brakes harshly. So, watch out for a change of tone from Jay Powell and co. in the coming weeks, especially if we now start to see an acceleration in inflation data. Tuesday’s release of CPI is thus going to be important for the dollar and the markets in general, as too will the speeches scheduled from various FOMC members (see below).

So, I reckon that volatility will spike sooner or later as growth optimism is replaced by inflationary concerns and taper tantrums. All it takes is a few people to start selling to get the ball rolling. With all the above macro concerns and talks about corporate tax hikes to pay for the cost of stimulus, things could unravel on Wall Street soon. Keep a close eye on the major indices -- and indeed individual names with the reporting season officially underway now.

Key economic data and company earnings highlights

Big Wall Street banks are set to report earnings next week, with JPMorgan, Wells Fargo and Goldman Sachs all due on Wednesday. On a macro level, Tuesday’s inflation data from the US is undoubtedly going to be important as it could impact bond yields, the dollar and obviously gold. Oh, and there is going to be an IPO as the largest US cryptocurrency exchange, Coinbase, goes public.

Tuesday

- Chinese trade figures

- UK GDP, construction output and industrial production

- German ZEW survey

- US CPI

- FOMC Member Daly speech

Wednesday

- RBNZ rate decision

- Eurozone industrial production

- Fedspeak: Chair Powell and FOMC members Williams and Clarida

- Earnings: JPMorgan, Goldman Sachs, Wells Fargo

- Coinbase IPO

Thursday

- Aussie employment report

- US retail sales, unemployment claims, industrial production and a few other second tier data

- Earnings: Bank of America, Citigroup and PepsiCo

Friday

- Chinese GDP, industrial production and retail sales,

- US building permits, housing starts, and UoM Inflation Expectations and Consumer Sentiment

- Earnings: Morgan Stanley, Bank of New York Mellon Corp and Honeywell International

Coinbase IPO

The largest US cryptocurrency exchange is set to go public on

Wednesday 14th April. Its shares will be listed on the Nasdaq Exchange and the company will trade under COIN stock ticker. The price range is still unknown. The company is planning a direct listing of its stock, meaning there won’t be a middleman (usually an investment bank such as Goldman Sachs) involved. In effect, the direct listing means the current stakeholders will be able to sell their shares to new investors.

Now Coinbase generates its revenue, among other things, from charging fees when investors and speculators buy and sell Bitcoin and other cryptocurrencies. With demand for cryptos soaring, Coinbase revenues and profit could increase further in the future – especially during times of heightened volatility in the crypto space. The IPO will allow investors to gain indirect exposure to cryptos without actually owning any digital currencies and worrying about the day-to-day volatility of cryptos.

S&P 500 rally near exhaustion?

The S&P 500 is testing the upper resistance of the rising wedge pattern currently. Given the strong bullish momentum, a continuation higher cannot be ruled out. But what I am interested in seeing is whether the breakout will fail, and we go back below the trend line. If that happens, we could see a sharp drop to at least the support trend line of the wedge pattern in the days ahead. It is worth pointing out that Relative Strength Index (RSI) indicator is at overbought levels of around 70. Keep an eye on the S&P 500 as the earnings season kicks into a higher gear and as taper talks potentially come to the forefront in the weeks ahead.

Source: ThinkMarkets and TradingView.com

South African Markets in focus

By Kearabilwe Nonyana

After an incredible earnings seasons by South African corporates the stock market remains at highly elevated levels but still within acceptable valuations. I believe the buoyancy in the market is backed by global vaccination roll outs as well as record infrastructure spending in the US. The demand for industrial metals in the Asia pacific area and the US will bode well for our local miners in the coming quarter. The JSE benchmark Top 40 index has been trading sideways for the week awaiting a catalyst to give it momentum to anyone side. Watching the price action over the past week since the 1

st of April you have seen a particular interest in our dual listed counters.

The Week Ahead

In the light of increased commodity prices globally in industrial metals and precious metals it will be very important to look at Mining production numbers which will be issued on Tuesday the 13/04/2021. This will affect our mining stocks as good production numbers could see increase volumes and increased profits which will affect the price of Mining stocks operating in South Africa.

Retail sales numbers will be released on Thursday the 15/04/2021. It will be interesting to see the bounce back in retail sales. The 3.5% year on year fall in retail sales last month signified a 10

th straight month of decline. It will be important to see if there is any improvement in the number. Any positive print will lead to a reaction in the grocery and clothing retailers.

What has been at the forefront of market participants is when the first signs of inflation will show. On Tuesday, the 13/04/2021 the US CPI data will be out. I do not expect any surprises to the upside but trying to detect if there is any demand in the economy will be a litmus test on the reflation trade going into the 2nd quarter.

Stock Pick for the week

Naspers and Prosus

Since the announcement of the sale of 190million shares in Tencent Naspers and Prosus biggest holding. This has been seen as positive for the unlocking of value as NPN:SJ and PRX sit at a deep discount to the NAV. This will serve to close that gap and management have signified that some parts of the $16 billion cash, they have gotten on the sale of TenCent will be used to buy back shares.

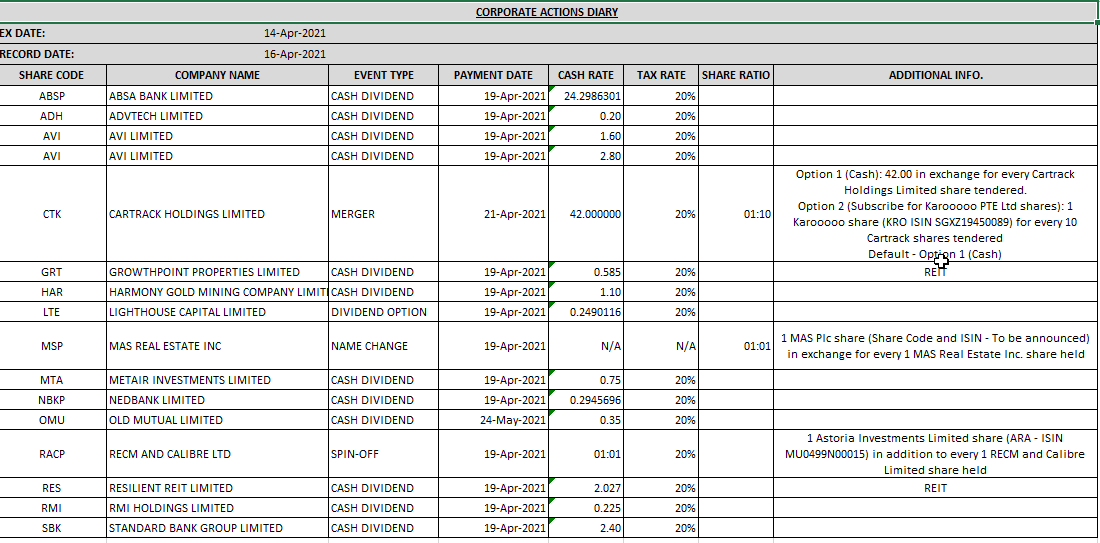

Corporate Actions Diary

Corporate Actions Diary

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

Learn and earn more today.

Visit our Education Centre