Global Macro

It has been a terribly busy couple of weeks in the global macro environment. Geopolitical tensions in far east Asia reached a boiling point last week as US House Speaker Nancy Pelosi visited Taiwan in defiance of requests by the Chinese Communist Party not to do so. Grain shipments from Ukraine’s Black Sea ports resumed in earnest, while the utilization of sophisticated American weaponry appears to have levelled the balance of the war in Ukraine’s favour for the first time in the six-month conflict. In the UK, the Bank of England raised the prime lending rate by 50 basis points last week to 1.75%, the largest rate increase in 27 years and warned of a lengthy recession looming next year. Liz Truss and Rishi Sunak, the two contenders for the leadership of the Conservative Party and the role of the UK Prime Minister continued slugging it out at the hustings as the 160 000 members of the Conservative Party get ready to indicate their preference by postal voting. In the televised debates so far, Rishi Sunak has appeared to be the clear winner, however, the Conservative-leaning Daily Express poll the day after the most recent debate revealed that Truss was the winner. The final result will be known by September 5. And while the developed world is getting used to higher interest rates, spare a thought for the developing world, especially developing Asia, where the need to increase interest rates is playing havoc with their exchange rates.

Nancy Pelosi is undoubtedly a woman of high moral integrity. Her anti-Chinese Communist Party credentials go back to at least 1991, when she made a very vocal protest at the crushing of dissent in Tiananmen Square in Beijing two years earlier. And in this latest episode, one can understand her reasoning for wanting to visit the breakaway island state, even though President Joe Biden had expressed his disapproval of such a trip. But the political and diplomatic stakes could not be higher right now. Russia is involved in a hugely illegal invasion of sovereign Ukraine and China is tacitly supporting this invasion. The Americans are supplying arms to Ukraine, which may, at last, be turning the tide in Ukraine’s favour. The last thing America needs right now is for China to resurrect a possible excuse for invading Taiwan.

In reality, of course, the Chinese wouldn’t dare risk invading Taiwan, for two reasons. Firstly, the Russia/Ukraine war, which was meant to be a template for a possible Chinese invasion of Taiwan, has gone hopelessly wrong for Russia. Instead of overrunning Ukraine in a matter of days and installing a puppet government in Kyiv as was originally planned, Russia has now got bogged down in a war that is sapping it of vital energy and resources. And Ukraine is a relatively flat country right next door to Russia which has only been preparing for war since 2014. Taiwan, conversely, is an island bristling with defensive structures and has been preparing for war with China for the best part of 70 years. An air and sea invasion would come at a great cost to China in terms of troops and hardware.

But secondly and more importantly, the west has exhibited a degree of coherence with respect to implementing sanctions that Vladimir Putin must have thought was impossible at the start of hostilities. China must realise now that if it were to invade Taiwan, it could reasonably expect to be sanctioned at least as hard as Russia.

There is one big difference, however. While Russia is more than self-sufficient in both food and energy and can therefore tough out sanctions for a long time, China is reliant on 80% of its oil from imports, which can easily be blockaded by cutting off two choke points in the Straits of Hormuz in the middle east and in the Malacca Strait that connects the Indian and Pacific oceans. China also imports around 80% of its food and so its food security would be at great risk if blockades were enacted against it.

So, unless and until China has managed to overcome its dependence on easily-blockaded sea routes for imports and exports, it will be vulnerable to retaliatory western and other sanctions. For this reason, China has been very busy gaining favour with its Belt & Road Initiative (BRI), which is effectively re-creating the old Silk Route between the west and China overland.

In Ukraine, the effective utilization of the American HIMARS multiple rocket launcher systems has resulted in a noticeable levelling up in the war in that country. The Ukrainians have managed to destroy a significant number of Russian ammunition depots in various parts of the country, and this has largely halted any Russian advances. Moreover, Ukrainian forces appear to be mounting a counter-offensive to recapture the city of Kherson in the south of the country.

What began as being a seemingly easy “limited special operation” for Russia has turned into a grinding nightmare for Vladimir Putin, the Russian leader. Putin badly miscalculated on so many fronts. He wasn’t counting on a long-drawn-out conflict where the largely conscripted Russian army would become disillusioned, nor did he quite grasp that the chains of command were top-heavy, with too many majors, colonels and generals and not enough sergeant-majors. Logistically, the Russian invasion has gone wrong almost from day one and any success the Russians have enjoyed has been almost entirely due to incessant artillery bombardment.

Putin also didn’t reckon on the west entering recession quite as quickly as it has. Although the US has still to have its technical recession verified by the National Bureau of Economic Research (NBER), most economists agree that the US has definitely entered a slowdown. This is reflected in reduced demand for oil and Brent crude is currently back at similar levels to where it was at the beginning of the war.

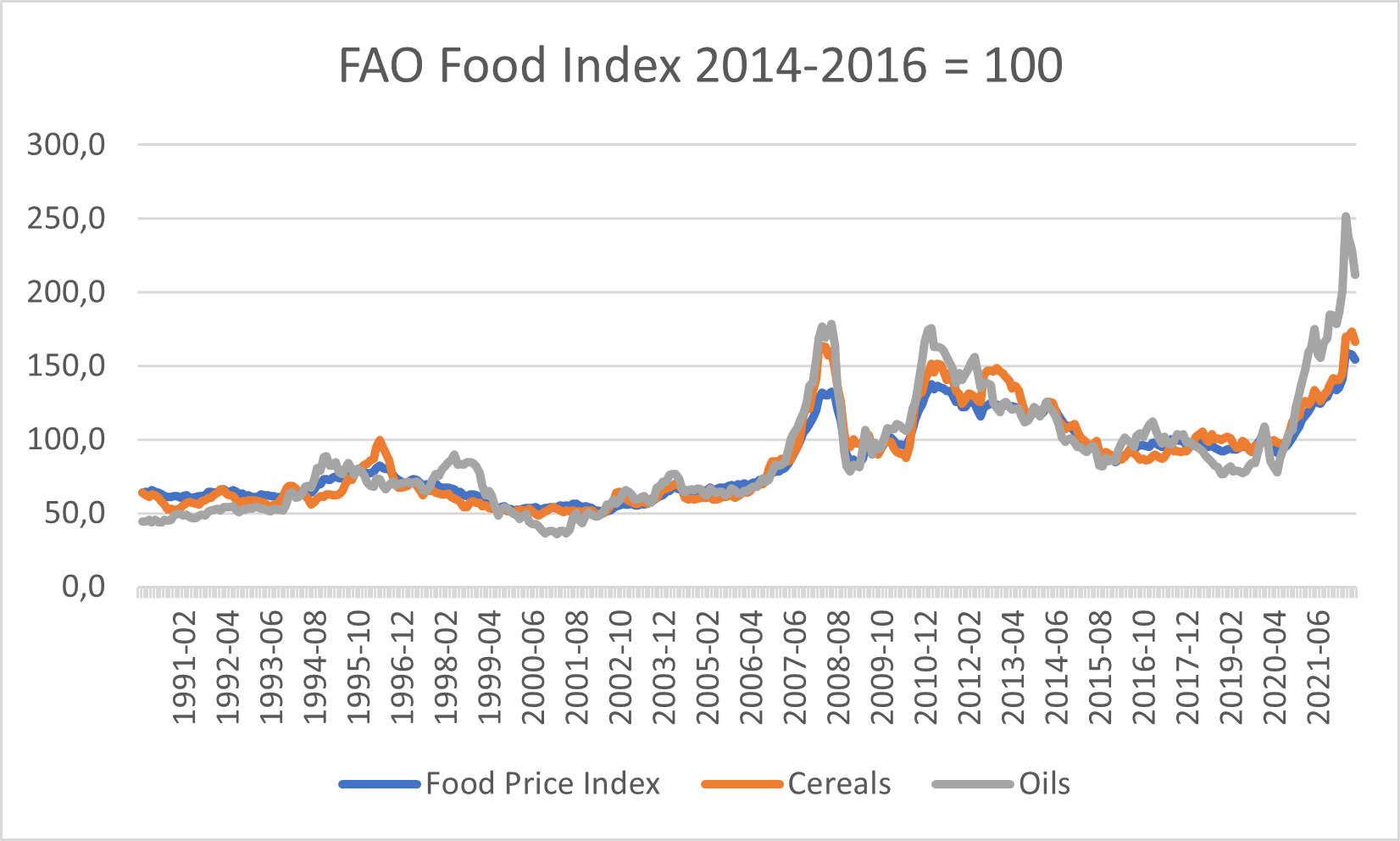

One of the few bright spots has been the noticeable reduction in the UN FAO Food Price Index, as shown in the accompanying graph.

Source: www.fao.org

Source: www.fao.org

The FAO Food Price Index averaged 140.9 points in July 2022, down 13.3 points (8.6%) from June, marking the fourth consecutive monthly decline. Nevertheless, it remained 16.4 points (13.1%) above its value in the corresponding month last year. The July decline was the steepest monthly fall in the value of the index since October 2008, led by significant drops in vegetable oil and cereal indices, while those of sugar, dairy and meat also fell but to a lesser extent.

As this newsletter went to print, the US CPI for July was released, which showed a welcome reduction in the rate of inflation compared to June. The Consumer Price Index for All Urban Consumers (CPI-U) was unchanged in July on a seasonally adjusted basis after rising 1.3 per cent in June, the U.S. Bureau of Labor Statistics reported. Over the last 12 months, the all items index increased 8.5 per cent before seasonal adjustment. That compares with a 9.1 per cent year-on-year increase in June.

The gasoline index fell 7.7 per cent in July and offset increases in the food and shelter indexes, resulting in the all items index being unchanged over the month. The energy index fell 4.6 per cent over the month as the indexes for gasoline and natural gas declined, but the index for electricity increased. The food index continued to rise, increasing 1.1 per cent over the month as the food at home index rose 1.3 per cent. This will take some pressure off the US Fed ahead of next month’s FOMC meeting, but inflation is still significantly higher than interest rates.

Local Macro

According to the Bureau of Economic Research (BER) in Stellenbosch, the seasonally adjusted Absa Purchasing Manager’s Index (PMI) plunged into negative territory in July as rotational power cuts and weak demand hurt output. This was the first reading below the 50-point neutral level since July 2021, when looting and unrest in KwaZulu/Natal and Gauteng beleaguered the sector. On an annual basis, official output data may look better compared to the weak July 2021 reading when output was distorted due to the looting and unrest, but the sharp decline in the business activity index argues against a strong quarter-on-quarter rebound following an expected decline in Q2.

In commodity markets, the 1-month forward Brent crude oil price declined by 13.7%. last week. Recession fears, notably in the US, where a technical recession is now evident, have weighed on the oil price since July. Brent averaged about $105/bbl in July, down from around $118/bbl in June, while the average during the first week of August was just $97/bbl. Although still early in the month, this could be good news for SA consumers who already saw a R1.32/litre decrease in the petrol price last week. The above also suggests that we may have seen the peak of the inflationary cycle for both fuel and food, at least for the time being.

Featured Stock

Massmart, US retailing giant Walmart’s 51%-owned South African subsidiary, released a trading update for the 6 months to end June 2022 recently. They were very poor and reflect not only a languid SA consumer economy but also Massmart’s attempts to turn this company around, which are not bearing fruit.

Total group sales were R41.3 billion, roughly the same as the comparable period in 2021. Stripping out Cambridge, Rhino and Massfresh, which were sold to Shoprite last year, leaves a figure for continuing sales of 38.1 billion, an increase over the comparable period in 2021 of 1.9%. Stripping out the impact of new store space, the sales growth number would have been 4.3%.

Liquor sales performed strongly from a low base of comparison in 2021, as no liquor restrictions relating to the coronavirus pandemic were experienced in the six months to June 2022. Liquor sales grew by 21.3%. Food sales rose by 6.4%. But general merchandise (GM), the second-most important category for Massmart, went backwards, with GM sales declining by 1.4%. GM has higher margins than food and associated categories, so there was a noticeable dampening effect on profitability. Additionally, the group experienced higher cost inflation than sales inflation, lower profit margins at Builders due to increased trade sales versus retail sales, increased finance costs and a once-off lease-exit settlement. The net result is an expected headline loss per share (HLPS) range of 409.1c to 425.7c from continuing operations for the six-month period. That compares with a HLPS of 166c for the comparable six months in 2021. The full results will be released on 29 August 2022.

This is a poor result, and the company has never managed to exhibit the kind of explosive growth that was expected from it in 2010, when Walmart took its majority stake. Instead, it has lurched from crisis to crisis and is currently undergoing another attempt at streamlining the business. But considering that the SA economy is about to experience an even tougher period as higher interest rates bite, Massmart’s prospects don’t look great.

Winners & Losers

Winners (%)

Winners & Losers

Winners (%)

SXM +25.24

HLM +11.54

FTA +11.46

BCF +11.23%

TMT +9.68

AME +9.38

SSK +9.33

SEB +8.70

MKR +7.87

SLG +7.69

BEL +6.96

Losers (%)

RNG -35.48

CND -28.57

VIS -25.0

KBO -20.0

MCZ -12.54

BRT -11.76

REB -10.19

CFRO -7.69

AVL -7.41

JSC -6.90

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.