You can also download a PDF version of this report HERE

Contents

-

Q4 Recap and Overview of Key Drivers for Q1 ..................................By Fawad Razaqzada

-

Q1 FX & Gold Outlook ........................................................................By Victor Golovtchenko

-

Q1 Crude Outlook: Risks Skewed to Downside .................................By Fawad Razaqzada

-

Q1 Global Stock Market Outlook ........................................................By Kearabilwe Nonyana

-

Q1 Crypto Outlook ..............................................................................By Carl Capolingua

1. Q4 Recap and Overview of Key Drivers for Q1

By Fawad Razaqzada

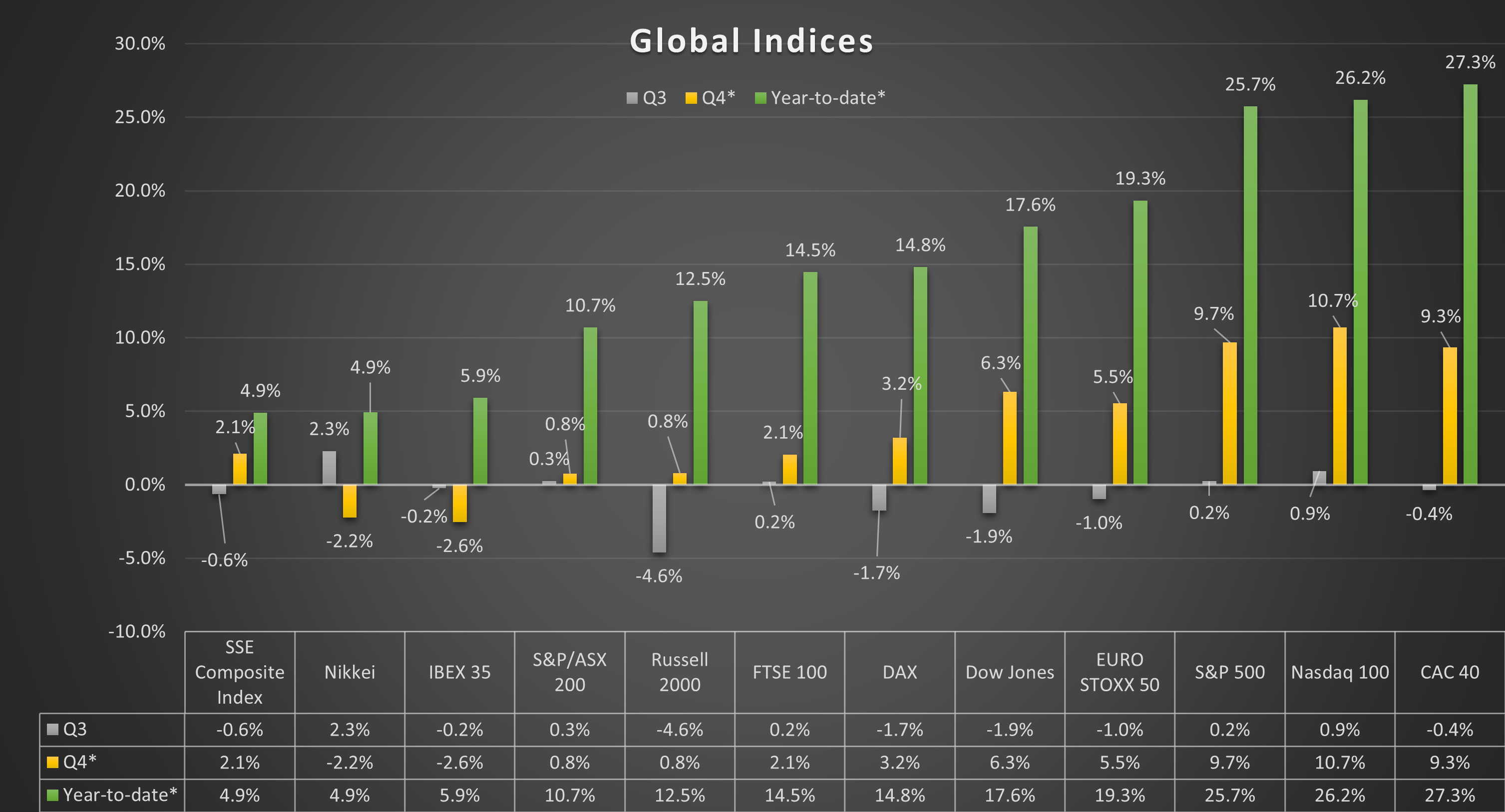

The global stock markets traded mixed in Q4 2021, with the major indices in US and Europe managing to claw back some of their losses suffered in the third quarter. The fourth quarter itself was quite volatile. October was generally a positive month, while November and start of December saw investors abandon risk as concerns over the economic impact of omicron variant of Covid, surging inflationary pressures and monetary tightening from major central banks all weighed on sentiment. But as we went to press in the final week of the month before Christmas, the markets managed to claw back their losses suffered earlier in the month. Investors were relieved by scientific evidence that although more infectious, there were not as many severe illnesses caused by Omicron as the Delta variant. This left the major indices on track to end the year with solid gains:

Source: ThinkMarkets; *prices and index levels correct as of 23 December 2021

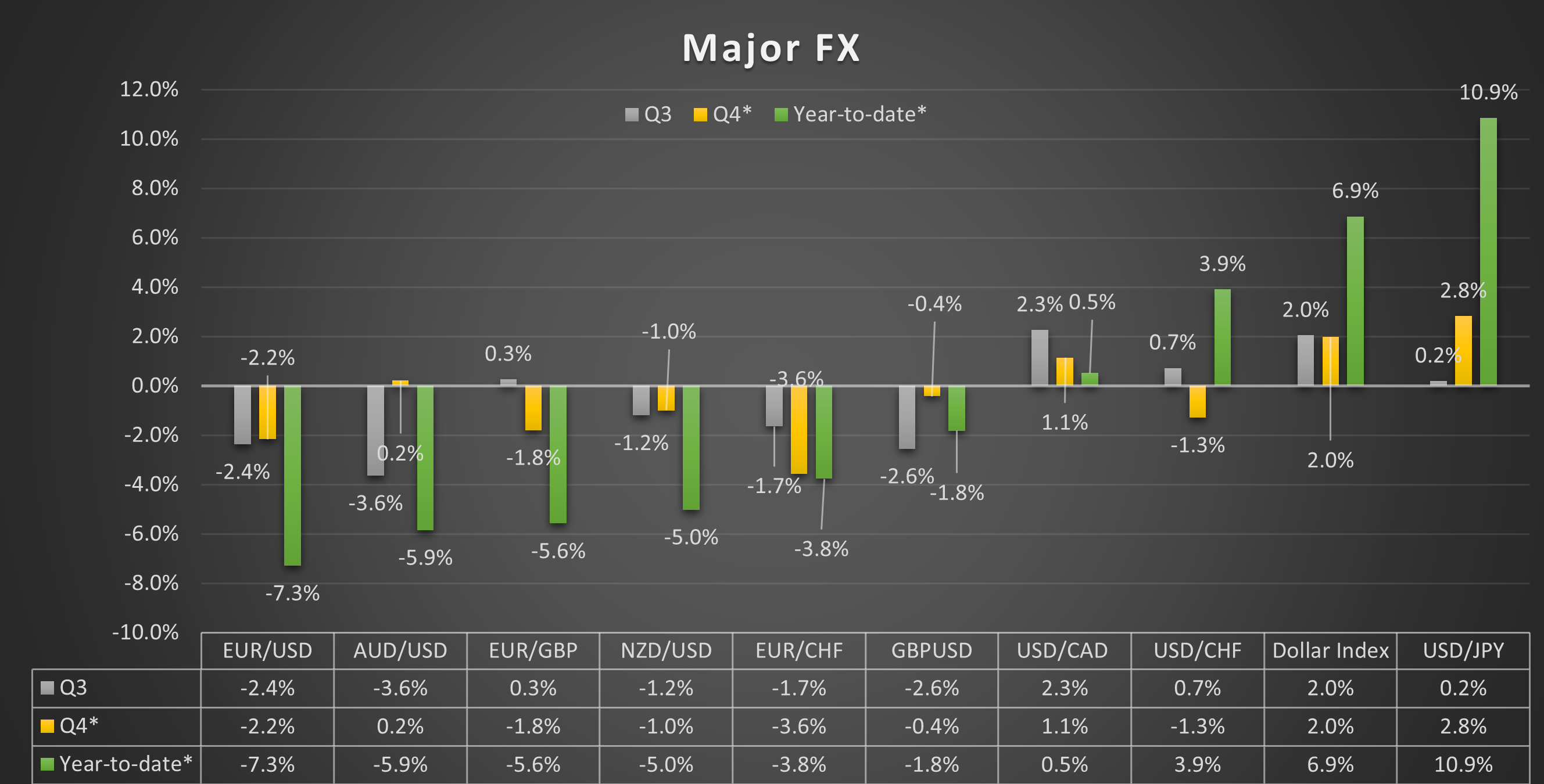

The FX markets were fairly contained in Q4, with the US dollar remaining bid against all the major currencies owing to a more hawkish central bank. The Fed announced in December that – because of NOT transitory inflation – it was speeding up tapering of its QE purchases and end the programme by March 2022, while the median FOMC projections pointed to three rate increases in the year ahead. This was in sharp contrast to the European Central Bank and Bank of Japan’s monetary policy updates, keeping their respective currencies under pressure. The ECB did however turn a bit hawkish as inflation surged higher in Eurozone too, driven by an energy crunch. Rising prices of oil and gas weighed on currencies of oil consumer nations like Japan, while supporting producer nations’ currencies such as the Canadian dollar. The Bank of England finally raised interest rates by 25 basis points, providing only moderate support to the pound, with sterling being held back by concerns that the economy would weaken as Omicron variant triggered a fresh wave of restrictions in the country. At the time of writing, in the last week before Christmas, the dollar remained head and shoulders above the rest:

Source: ThinkMarkets; *prices correct as of 23 December 2021

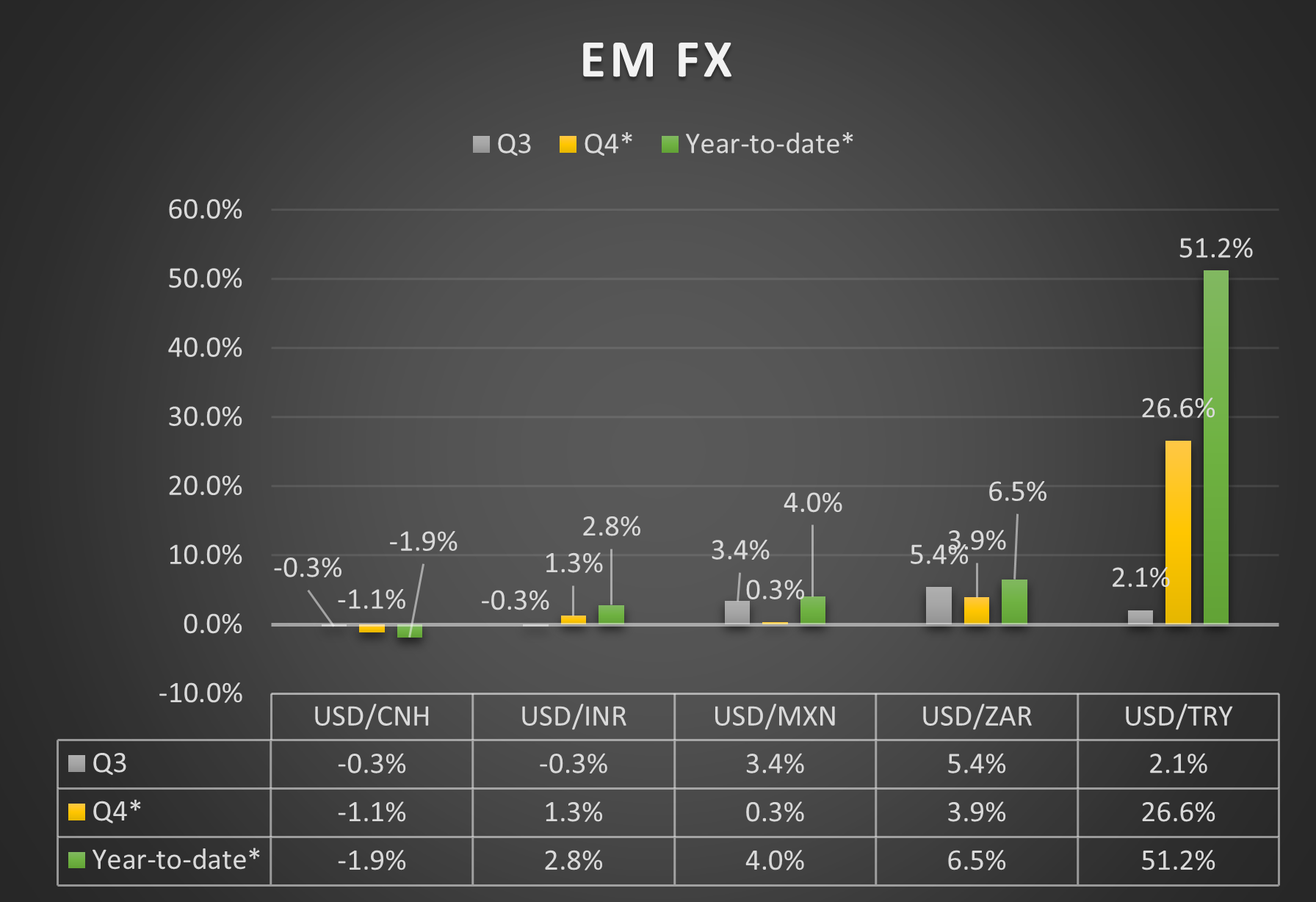

The greenback rose more profoundly against emerging market currencies, most notably the lira. The beleaguered Turkish currency slumped to repeated record lows, as despite high levels of inflation the country’s President Recep Tayyip Erdoğan ordered the CBRT to keep cutting interest rates. Some of the other EM currencies fared slightly better, with the Chinese yuan completely bucking the trend. Overall, though, it hasn’t been a good quarter or indeed a year for EM currencies as a whole:

Source: ThinkMarkets; *prices correct as of 23 December 2021

Source: ThinkMarkets; *prices correct as of 23 December 2021

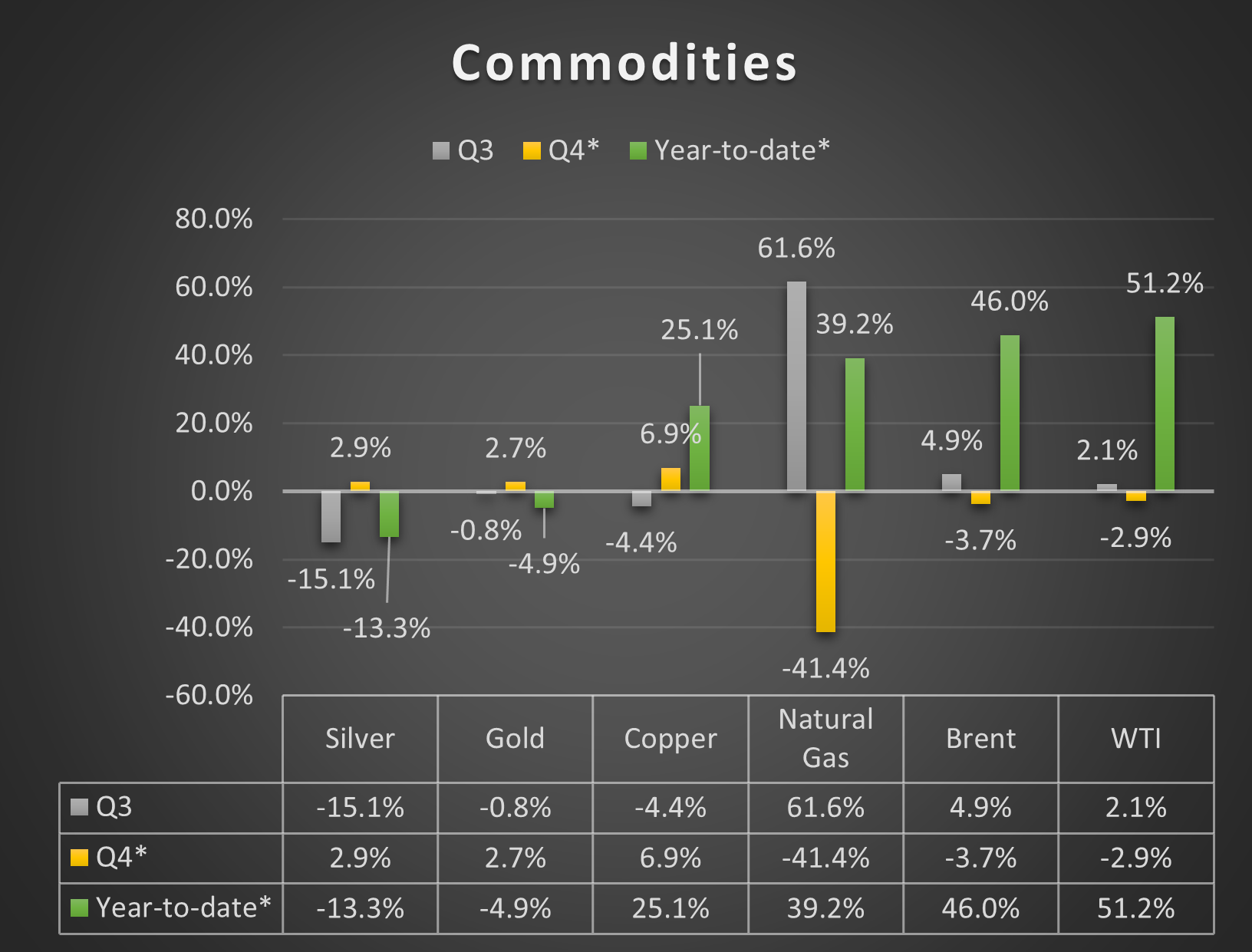

The key drivers behind the currency and equity markets have been inflation, due in part to surging commodity prices and supply chain issues. In the fourth quarter, however, energy prices came back down, and this helped to reduce the overall yearly gains. Precious metal prices have been under pressure all year long due to elevated bond yields and a stronger US dollar, with investors not too keen to buy gold as a hedge against soaring inflation.

Source: ThinkMarkets; *prices correct as of 23 December 2021

Source: ThinkMarkets; *prices correct as of 23 December 2021

Apart from the fact that both the US dollar and global bond yields both rose, the only other reason why gold was disliked was probably due to this:

Source: ThinkMarkets; *prices correct as of 23 December 2021

Source: ThinkMarkets; *prices correct as of 23 December 2021

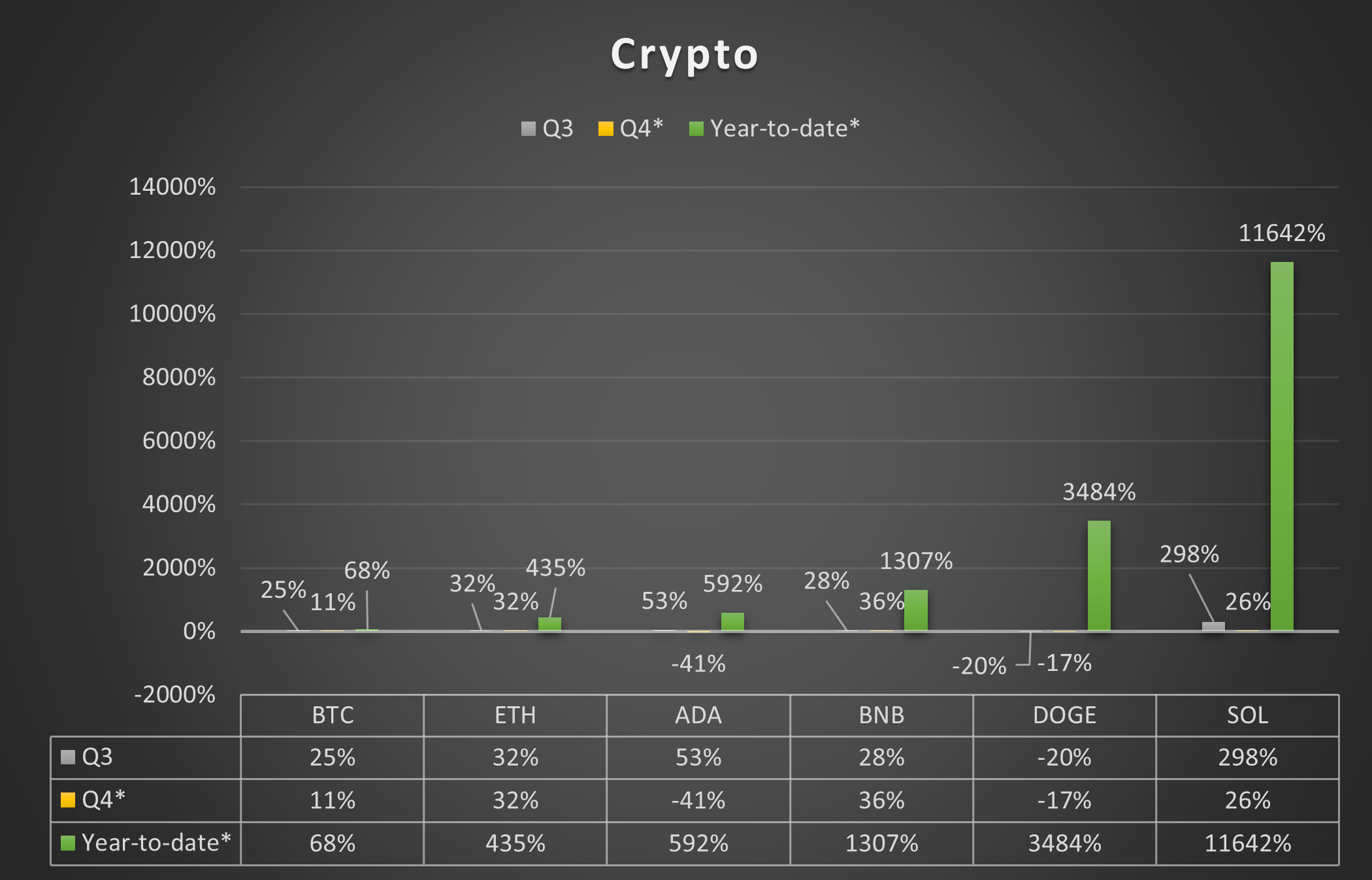

Bitcoin and Etheruem added more to their 2021 gains in Q4, while some cryptos consolidated their gains. Investor appetite remained insatiable for most of the year, although November and December weren’t great months for crypto as risk assets suffered across the board.

Q1 Outlook Overview: Key Drivers

Heading into the first quarter of 2022, concerns over the economic impact of the coronavirus and high levels of inflation will continue to dictate market and policy direction alike. Investors will want to know what steps governments and central banks might take to stem price pressures, and at the same time, keep their respective economies ticking over as the latest covid-linked restrictions weigh on activity. With governments around the world sharply increasing fiscal spending during the pandemic, introducing further stimulus measures without raising taxes will be politically very difficult. Likewise, central banks have pushed themselves into a corner. Surely, they will be less keen to ramp up bond purchases again, with inflation being so high. If anything, the Fed may not even wait until the middle of next year to raise interest rates and could also wrap up bond purchases sooner, if inflation heats up even more in the next couple of months. What the Fed decides will also have big ramifications for the dollar and commodities like gold and silver. Will gold finally respond to inflation, or will the dollar again prove too hot for the precious metal? Elsewhere in commodities, the OPEC+ has a tough decision to make. While oil prices have fallen back a tad, they still remain quite high. The group is set to boost its oil output by another 400K barrels per day in January, but the latest covid-linked travel restrictions could mean a pause in future output hikes. And what about crypto – more of the same or a year of consolidation?

2. Q1 FX & Gold Outlook

By Victor Golovtchenko

The outlook for the first quarter of 2022, is primarily contingent on the actions of the US Federal Reserve, as well as Covid.

How Far Can the Fed Tighten Before Breaking Something?

With the USD rally lasting through 2021, the positive news for the greenback appears to have reached a plateau, with more hawkish talk from Fed officials not translating into an even higher exchange rate. Our team considers the best days for the US currency during this cycle to be behind us, though assuming strong macroeconomic data in Q1, we might see another stab higher in the USD index, currently trading around 96.00. The level has proven to be crucial over the past 3 years, and the market is taking a breath of fresh air before attempting a more decisive move above (or below) this strong resistance area.

Dollar index daily chart:

Source: ThinkMarkets and TradingView.com

Source: ThinkMarkets and TradingView.com

BoE hikes and UK government provides more support

The first major central bank to hike rates was in fact the Bank of England and while it took a couple of days, the GBP rallied across the board, torpedoing the rest of the FX market into a defensive stance. The continuously evolving coronavirus is still the main concern for the UK economy, though fiscal measures targeting businesses affected most by the latest pandemic developments, were unveiled by Chancellor the Exchequer, Rishi Sunak, last week. The announcement coincided with the lows for the GBP, which gave back all of its rate hike-related gains in the two subsequent sessions.

ECB reluctantly turns slightly hawkish

The euro appears to be on the defensive against most major FX counterparts, and rangebound against the USD. ECB and BOJ policymakers have been reluctant to shift their tone to a more hawkish one, remaining the only major central banks to stay pat in the face continuously rising inflation pressures. Mrs Lagarde will have to continue walking a tight rope, as the health of the European banking system is much different when compared to across the Atlantic. Her dovish stance was recently reinforced, but the appointments of a new Head of the Bundesbank who’s expected to be quite hawkish, provided some temporary relief for the EUR bulls in recent sessions.

Commodity FX vulnerable

Commodity currencies appear to have bottomed out for now, as the market awaits more macroeconomic cues that could influence commodities markets. With almost all of the major central banks on their way to tighten monetary policy, a risk-off episode could still supply some upside for the USD, and pressure commodities and antipodean currencies (AUD, CAD, NZD). Stocks continue trading near all-time highs both in terms of nominal value, and valuations.

Gold outlook remains murky

Gold continues to trade in tight ranges, and in anticipating that the Fed will sooner or later “break” the liquidity pipeline, any selloffs are met with swift demand. While the majority of market players remain bullish on precious metals, a liquidity-driven selloff could also briefly impact this sector of the market. That said, gold bulls couldn’t have prayed for a better scenario for a multi-year bullish breakout, yet the current macro environment is still not yielding a decisive breakout above $2000. Ultimately it will all come down to monetary policy once again.

Damned if they do, damned if they don’t

The US Federal Reserve is in the unenviable position to choose between persistently high inflation numbers, and persistently overvalued financial markets that support the economy. The fiscal impulse appears to be waning and inflationary pressures in 2022 are unlikely to match the ones we’ve seen over the past two years. Even without monetary tightening, the fiscal side of policy is already enough to slow growth materially in the first half of the coming year. Chair Powell has been persistent in communicating to the market that policy is about to tighten, and some market players are forecasting the first hike as early as March.

Financial markets are currently pricing in three hikes for next year - March, June and Dec. A fourth hike in the beginning of 2023 is also on the cards. All of this while the midterm elections are incoming next year, and the democrats are likely to lose the House and get pressured hard in the Senate. Should this scenario unfold, the fiscal impulse until 2024 is unlikely to be positive for the stock market - yet another nail in the coffin of risk sentiment.

Keeping a close eye on the yield curve, and an inversion that usually signals that the Fed has indeed overtightened - usually just the time when the USD starts turning. To sum up - the key for the outlook for the USD during the first months of 2021 is how far can the Fed really tighten before breaking something. As the economic cycle turns, the last bouts of strength in the greenback will inevitably disappear and a new cycle of weakness could ensue.

3. Q1 Crude Outlook: Risks skewed to downside

By Fawad Razaqzada

In the fourth quarter, oil prices ended a run of six straight quarters of wins, although managed to rebound sharply in December as preliminary data showed that omicron is comparatively less dangerous than delta. Still, the very rapid spread of the new variant saw governments take measures to slow the spread. Many European countries banned travellers from the UK, while Chinese authorities locked down a city of 13 million people. There has been some resistance to more severe curbs in the US and Europe. Whether that resistance holds or folds, will depend on how the virus situation will evolve in the coming weeks.

Demand for oil has likely weakened somewhat already due to the travel restrictions, while supplies have continued to grow. This means that the pressure on oil prices are likely to ease back if the OPEC+ goes ahead with its planned output hike of 400K barrels per day of oil in January.

Beyond the immediate outlook, I cannot see how crude oil prices will rise significantly further. The OPEC+ remains committed to gradually release more oil to the market in 2022, for as long as the worst-case scenario from the pandemic does not play out.

Growth in demand could also slow because of (1) EM currency crisis in several oil-importing nations as USD extends its rally and (2) supply bottlenecks and the return of lockdowns could undermine the economic recovery in more developed economies, at a time when fiscal and monetary polices have already been – or nearly – exhausted. Meanwhile, US oil supply is on the rise again. The crude oil market is thus unlikely to remain tight, meaning prices could weaken somewhat.

From a technical point of view, the $70 support is going to be pivotal for Brent oil prices. However, Brent’s long-term bearish trend line has been reclaimed by the bears, which means short-term rallies could get sold into as you can see on this monthly chart:

Source: ThinkMarkets and TradingView.com

Source: ThinkMarkets and TradingView.com

4. Q 1 Global Stock Market Outlook

By Kearabilwe Nonyana

In the beginning of Q4, global markets were on a positive ground as US earnings for global tech companies were predicted to increase and show robust growth. What was revealed was even better, as US tech giants surprised with their third quarter results, spurring on US indices to hit fresh high and helped to keep sentiment supported for global markets. Apart from surging inflation, the other most common theme in the last quarter of 2021 was the market’s fascination with what the FOMC implied with its rhetoric on monetary policy and the path of future interest rates. The Fed has alluded that it will taper bond buying, although this does not necessarily mean the taps on bond buying will be shut completely. I expect high levels of liquidity to still impact the performance of the equity capital markets across the globe, as the search for inflation-beating returns are sought after by investors.

Looking ahead to Q1

Below, I have discussed some of the important themes which could impact the stock markets in Q1 2022, and potentially beyond.

Inflation outlook

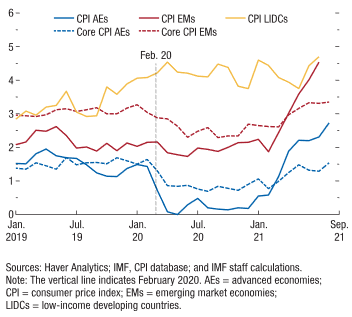

In recent months, inflation has increased sharply in advanced as well as emerging market economies. Price pressures have been driven largely by (1) strong demand as economies re-opened, (2) supply chain shortages and (3) rapidly rising commodity prices. Many market participants have been at loggerheads as to how to interpret the hotter-than-expected global inflation on monetary policy and in turn stock markets. There have been extensive debates as to the nature of the inflation – is it structural and long-term, or is it short-term and transitory? In my opinion, longer term inflation expectations are anchored and do not pose any threat to price stability. That said, the shorter-term movements of risk assets will be largely dependent on how changes in monetary and fiscal policies are communicated to the market. The problem which I have observed is that central banks and governments are finding it difficult to communicate effectively with the market as to how they are seeing inflation and how they will react.

CPI data for various country groups as given by the IMF:

Bond yield attractiveness

In the search for yield in the past 2 years, the equity market has had very little competition. Bond yields were at all-time lows as open market operation pushed them to near- or sub-zero; accommodative monetary policy led to different asset classes such as cryptos being the only competition for equities. With central bankers alluding to tightening monetary policy, this makes bonds attractive for yield-seekers. As yields rise, equities will become increasingly risky given their extremely high valuations. Some investors will start preferring the relative safety of bonds given that they are now providing an attractive alternative in terms of yields compared to, for example, the US technology sector. However, not all sectors will be negatively impacted by rising yields. Banks and financial stocks tend to do well when bond yields are on the rise.

Trend is your friend

Global equity markets are still in an upward trend even though many indices around the world have reached all-time highs. The threats to global supply chains still linger in the forefront to any positive gains in the first quarter and threats of the contagion effect of the spread of the Omicron variant. But looking at consensus forecasts of earnings being on the upside, the market will take favourably to corporates performing well and reward the ratings on the stocks that do well.

Volatility

The spread between the cash VIX and longest dated, most active, futures contract which is dated for end of February has shown a larger than expected divergence recently. This is usually an indicator of higher expected volatility or change in sentiment. The VIX is still very far off its highs at the beginning of the pandemic but is edging higher, so expect a spike in short term volatility in Q1. Even so, I still anticipate that global markets remain at elevated levels and positive returns on global stocks will be seen in 2022.

Overbought

From a technical point of view, all the major indices appear overbought on their longer-term chart. For example, take a look at the RSI on the monthly chart of US30, which it is reaching technically overbought territory of around 70:

Though it has had a correction in the past month as fears of the omicron variant threatened to slow down economic growth, it remains to be seen whether we will see some further short-term weakness. With that correction, the market already took some opportunity to come back and buy the dips.

5. Q1 Crypto Outlook

By Carl Capolingua

Quite a bit has happened since our last quarterly crypto update, but activity and volatility is what we have come to expect from this exciting asset class! Here are the key developments from the last three months, and then we'll conclude with a look ahead to the factors that may impact cryptocurrencies in the first quarter of 2022.

Finally, a Bitcoin ETF, but spot-based product is elusive

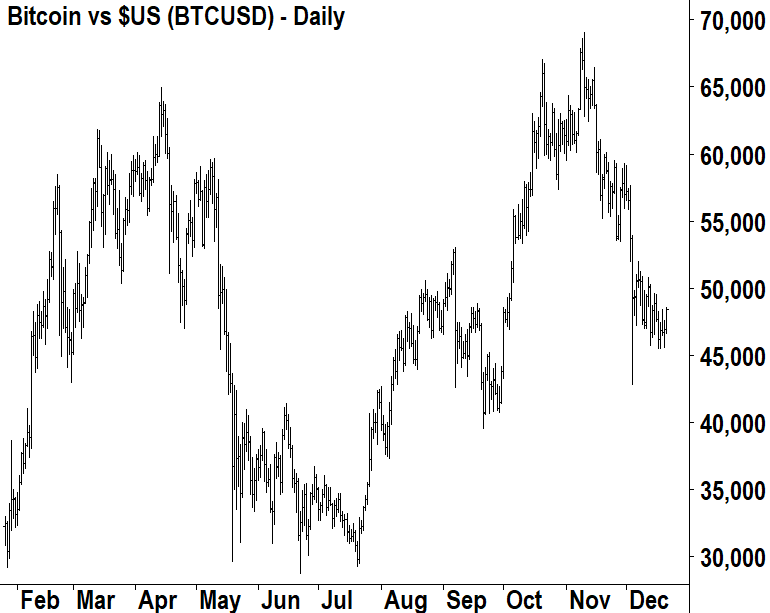

The first bitcoin-based ETF commenced trading on the New York Stock Exchange on October 18. The ProShares Bitcoin Strategy ETF tracks the movement of a number of Bitcoin futures contracts. Whilst Bitcoin prices saw a strong run-up in anticipation of the launch, the lack approval of a spot-based Bitcoin ETF was seen as a disappointment by many, and potentially acted as a catalyst for the subsequent correction in Bitcoin prices.

As of now, there are three bitcoin ETFs trading in the U.S. with at least two spot-based products under consideration by the SEC (they have rejected two spot bitcoin ETF proposals in recent weeks, one from Wisdom Tree, and one from Van Eck). The rejects will no doubt end up back on the SEC's desk before too long and will join other spot-based hopefuls Grayscale's Bitcoin Trust and Bitwise's Bitcoin ETP which have decisions pending in early February 2022.

Take me down to Bitcoin City…

After its official adoption of Bitcoin as legal tender in Q3, El-Salvador kept buying the dip trough Q4. President Nayib Bukele tweeted multiple times over the last couple of months that his country continued to build its Bitcoin reserves on price weakness. Interestingly, as the price of Bitcoin has settled firmly in the doldrums below the psychological US$50k mark, it appears the dip buying has stopped for now.

In other ES developments, Bukele proposed in late-November his country would build a new city dedicated to Bitcoin mining. The mining would be powered by volcanic energy as the city, dubbed "Bitcoin City", would sit at the base of one of El-Salvador's active volcanos. Citizens of Bitcoin City would be free of income, property, and capital gains taxes. El-Salvador intends to issue $US1billion of "volcano bonds" to pay for building the city, of which half would be directed to buying Bitcoin.

JP flips, crypto dips

Bitcoin started Q4 with a rocket underneath it as it as many investors began to assume US$100k by years' end. Typically, when the market gets that confident, a correction is generally in the cards, and this time was no exception. Whilst it did take out its April all-time-highs, Bitcoin faltered just under US$70k and has since steadily declined into the mid-US$40k's. Looking forward, investors can look elsewhere until Bitcoin breaks back above at least US$51k.

Working against Bitcoin and the broader cryptocurrency universe was a major hawkish tilt by US Federal Reserve Chairman Jerome Powell. The flip followed significantly worse than expected inflation data throughout the quarter, and perhaps not coincidentally, his reappointment as Fed chairman for another 4-year term. Bitcoin, and indeed cryptocurrency as an asset class, remains a confidence and liquidity game. As the Fed looks to remove liquidity from the financial system, this is expected to have a negative impact on the availability of hot money that has sought out these highly volatile assets throughout 2021.

Fed policy will no doubt be a major stumbling block for crypto in 2022, and crypto investors will have to be on their toes watching for signs liquidity is going to be removed from the system faster than originally expected. The next Federal Open Market Committee (FOMC) meeting, and therefore catalyst for further crypto volatility, is tentatively set for January 25-26 2022.

ADA, DOT, LINK slip, AVAX, LUNA gain on DeFi

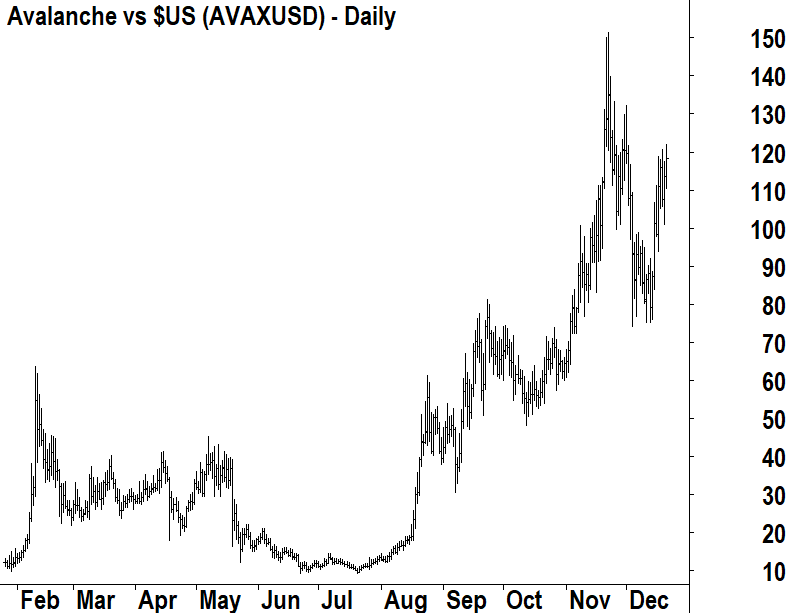

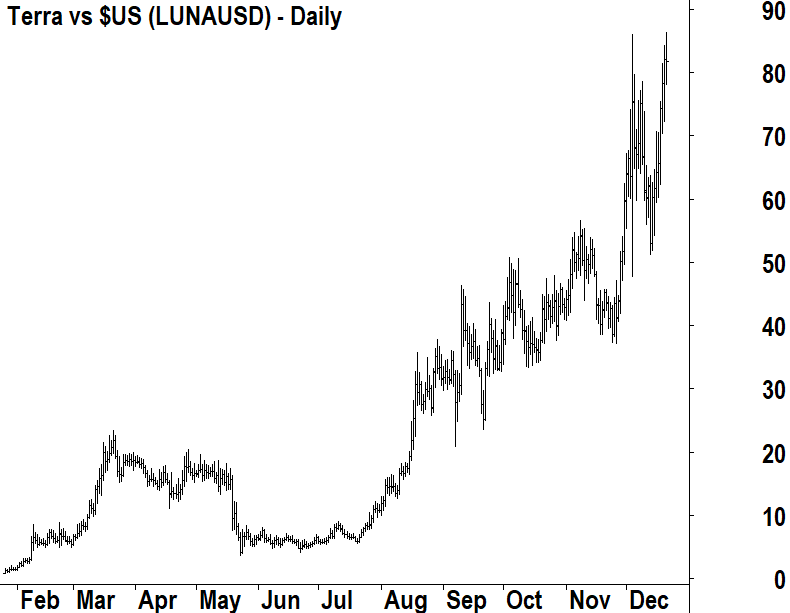

The vast majority of altcoins suffered fates far worse than Bitcoin approximate 30% fall during Q4. In the Top 20, Cardano's ADA (-44%), Polkadot's DOT (-60%), and Chainlink's LINK (-50%) were the worst performers. Two altcoins that prospered however, were Avalanche's AVAX (+77%) and Terra's LUNA (+113%). Each saw a steady increase in the amount of DeFi activity appearing on their blockchains.

One of the most commonly used metrics for measuring DeFi adoption on a particular blockchain is "Total Value Locked" or TVL. Avalanche's TVL rose from 2.1% at the end of Q3 to just over 5% at the time of writing, while Terra's TVL increased from 4.9% to 7.5%. Both blockchains took market share from DeFi juggernaut Ethereum, which saw its share of the TVL pie fall by around 4% over the quarter. Both the technicals, and the TVL trends for AVAX and LUNA remain strong, so crypto investors may wish to pay closer attention to them in Q1 2022.

2022 is going to be all about the 'R' word

It's perhaps inevitable (famous last words!) that we'll see a spot-based Bitcoin ETF in 2022, and all eyes will be on the SEC's decisions for Grayscale's and Bitwise's offerings on Feb 6 and Feb 1 respectively.

More broadly, the SEC has taken an increasingly tougher stance on cryptocurrencies and cryptocurrency businesses over the course of Q4. This is likely to continue into 2022 as Chair Gary Gensler has indicated that he wants extra layers of protection put in place for crypto investors. At the Yahoo.com All Markets Summit held in late October, he said: "Investors aren't protected the way they are [in the] the stock or bonds markets that we've overseen so long. Without that, I think it really is…a bit of the Wild West."

Elsewhere, Russia's stance towards its citizens holding crypto assets appears to be hardening with rumours the Central Bank of Russia is considering a total ban on the acquisition of crypto assets. But, in Australia, Federal Treasurer Josh Friedenberg a mooted a "comprehensive payments and crypto-asset reform plan" which could be finalised by the end of 2022.

Clearly the crypto market needs more regulation to protect investors and provide safeguards in the event of nefarious activity. It is an important step towards the widespread adoption of crypto as an asset class. We expect 2022 is going to be a defining year in crypto regulation as a number of governments move closer to backing up their rhetoric with legislation.

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.