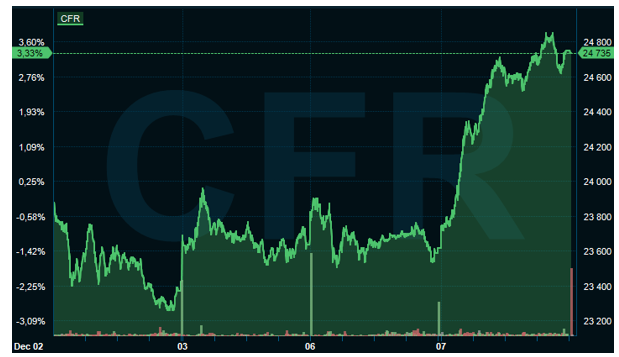

In Tuesday’s trading session in the local markets, the Top 40 closed the day up by 2.96%. The Resources 10 sector went up by 4%, the Financial 15 went up by 0.74%, the Industrial 25 went up by 2.8% and lastly the South African Listed Property index up by 1.14%. The rand traded at R15.87 against the United States Dollar, R21.00 against the Great British pound, and R17.84 against the Euro. On the macro front, South Africa's GDP slumped by 1.5% in the third quarter, eroding some of the economic gains the country has made since the severe impact of COVID-19 in the second quarter of 2020 and a major setback to the recovery from last year’s 6.4% contraction. Richemont had a great day in the market and managed to reach 12-month highs in the trading session.

Figure 1:CFR weekly chart

On the commodities front, the Brent Crude oil is trading at $74.90 a barrel and WTI Crude oil is traded at $71.39 a barrel. Gold Spot price is currently trading at $1790.20; Platinum Spot is now trading at $965.50 and lastly, Palladium Spot price is at $1873.50. The oil prices remain stable after rebounding from the overreaction around the new variant. Omicron has led to some restrictions on air travel, and researchers in South Africa said the strain’s ability to evade vaccine and infection-induced immunity is “robust but not complete.” On inventory news, stocks of crude in the US fell by 3,089 million barrels. Meantime, tensions between Moscow and Kyiv grew, with US President Joe Biden warning Russian President Vladimir Putin that he could face tough economic sanctions from the West if Russia invades Ukraine.

Across the globe, the S&P 500 closed the day up 2.13%, Dow Jones closed up 1.46% and the Nasdaq had a 3.15% climb. The FTSE 100 closed up by 1.49% and the DAX was up 2.82% and CAC40 was up 2.91%. In the Asian markets, the Nikkei 225 is up 1.42% and the Hang Seng is currently down 0.02%. Meanwhile, investors are also weighing the likelihood that the Federal Reserve would accelerate its stimulus tapering and hike rates sooner than expected, with markets focusing on the inflation data due later this week which could become the catalyst for the Fed to deliver faster tightening of its policies.

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

Tags:

Daily BriefingFundamental Analysis

Learn and earn more today.

Visit our Education Centre