The economic calendar is going to play second fiddle to the events that have weighed on investor sentiment. On Friday, after a relative period of calm, stocks resumed sliding and the dollar pushed higher, most notably against commodity dollars and emerging market currencies. Chief among investor concerns are: (1) Omicron variant of Covid, and (2) the potential speeding up of bond tapering by Federal Reserve.

Crude oil on slippery slopes

Although crude oil bounced back off its multi-month lows that were hit in the immediate aftermath of the OPEC+ decision on Thursday, prices remain vulnerable and on Friday, they revered along with stocks and other risk assets. In early parts of the week ahead, don’t be surprised to see further weakness. Contrary to some expectations for only a moderate hike or no hike at all for January, the OPEC+ said it will raise output by another 400K barrels per day in January, adding more oil to the global supply and thus completely removing the threat of supply shortages at a time when demand is expected to fall. Still, the OPEC+ has now stated that it may adjust future production plans if the market changes. So, I suppose it all now depends on Covid and lockdowns. If the situation deteriorates then the OPEC+ will stop further production hikes, possibly as early as their next meet on January 4th. Otherwise, the current policy may rollover as planned. Expect to see moderate further weakness in oil prices.

Stocks face greater uncertainty as we approach year-end

Europe has been struggling after the recent upsurge in virus cases, causing German consumer confidence to drop sharply in November. The fourth wave of Covid, has added to worries about surging inflation – not just in Europe, but US too. The potential for more lockdown measures means the outlook for the festive season is going to be a bit murky. This may discourage investors to take on too much risk, potentially meaning equities might struggle for direction, or worse fall further.

Friday’s nonfarm payrolls report showed US jobs growth slowed in November, although investors have other worries. Fed Chairman Jerome Powell has already set out the near term path of monetary policy at his testimony this week. Powell admitted the central bank’s “transitory” view of inflation was wrong and that they could wrap up bond purchases in the next few months, despite the threat of Omicron variant. The market seems to have not liked this, selling off as we closed the week.

In the week ahead, Omicron developments should continue to move the markets. I reckon the risks are skewed to the downside in the short term outlook, but until the impact of the new variant of the virus becomes clearer, don’t expect a more significant drop. In any case, a repeat of the 2020-style drop looks very unlikely. After all, the world is in a much better place to deal and live with the new variant of Covid. What’s more, it could be that this new variant may not be as dangerous as some people fear.

Europe likely to outperform US in slightly longer-term outlook

Looking further out, it is possible that the European markets may outperform Wall Street. US investors have been spooked by the potential for a faster end to the Fed’s bond-buying programme, which could open the door to earlier interest rate hikes. Unlike the past, it looks as though concerns over economic growth stemming from the renewed upsurge in Covid cases and new variant have been replaced by surging inflation. The Fed wants to tackle inflation now before it gets too overcooked. In contrast, the European Central Bank is likely to maintain its bond buying programme in some form even after PEPP ends, likely in March. Here, growth concerns remain significantly higher than in the US, with the likes of Spain struggling to recover from the pandemic. Though inflation has sky-rocketed in recent months, we have seen energy prices come down sharply while other factors such as supply bottlenecks are likely to fade further in the months ahead. Hopefully inflation will ease back, allowing the ECB to keep the printer going ‘brrrr’. The euro should weaken as result, boosting European exports – all else being equal.

Pounded

It is worth keeping a close eye on the pound, too, given that the Bank of England’s Michael Saunders, a hawk, seems to have had a change in heart. Saunders said he sees advantages in waiting for more data on the omicron variant, before potentially hiking rates. Investors sold the pound as the probability for a rate hike this month was slashed.

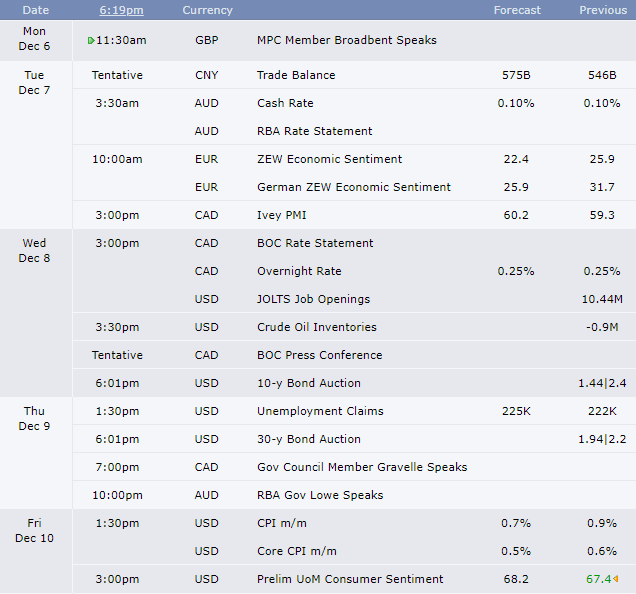

Macro highlights

Source: ForexFactory

Source: ForexFactory

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

Learn and earn more today.

Visit our Education Centre