Local Macro

When South Africans awoke in the new year of 2023, it became painfully obvious that very little was going to change on the economic front. While a recession has been narrowly averted, the extent of any positive economic growth this year and next will be nothing to get excited about. And the dreary, dismal outlook for Eskom is likely to deteriorate even further this year if that’s possible.

The Council for Scientific and Industrial Research (CSIR), a government think-tank, believes that another decade of rotational power cuts (load-

shedding in Eskom-speak) is a possible scenario for South Africa. This depressing possibility was articulated in a recent interview by senior CSIR energy researcher Monique Le Roux in an interview with a local TV channel.

According to Le Roux, the problem relates to the incapacity of the electrical grid system to bring renewable energy from the areas in which it is generated to the areas in which it is needed. So for example, most of the solar energy in SA is generated in the sparsely-populated northern Cape and wind energy tends to come mainly from the western and eastern Capes, where there is not too much demand either.

An additional problem with solar is that demand is at its greatest at precisely the time of day when solar plants are at their weakest generation point ie early morning and early evening.

Le Roux reckons it will take ten years to upgrade Eskom’s grid to be able to handle new renewable capacity, during which time, load-shedding will persist.

Outgoing Eskom CEO Andre de Ruyter was poisoned with cyanide in his coffee late last month. De Ruyter still has three months to go before he steps down at the end of March and as yet there is no indication as to who his successor will be. Anyone taking on the role will be taking on a poisoned chalice (pun intended) as it appears that the utility is fully in the grip of criminal syndicates and it is effectively in a state of siege.

Whoever assumes the role of the new CEO will have the unenviable task of cleaning up the utility and attempting to rid it of the criminal elements that are currently suffocating it operationally.

The National Energy Regulator of SA (NERSA) granted Eskom an 18.65% tariff increase for 2023/24, which although much lower than the 32% requested by Eskom, will still be a serious inflationary element for all South African consumers to bear. Worryingly from an immediate power cut perspective, NERSA declined Eskom’s request for a further R16.9 billion for diesel to power its open cycle gas turbines (OCGTs). This means that Eskom will effectively be applying two stages higher than it otherwise would if it had unfettered access to as much diesel as it needed.

While NERSA is, understandably, attempting to play the role of an external disciplinarian with Eskom in the matter of diesel budgets, it may have lost sight of the bigger picture ie the opportunity cost to the economy of not having enough power. It’s a difficult balance to get right.

It appears as though control of Eskom will pass from Pravin Gordhan’s State-Owned Enterprises department to Gwede Mantashe’s Department of Mineral Resources & Energy (DMRE). While cynics may regard this as being no more than re-arranging the deckchairs on the Titanic, there can be little doubt that such a move opens the door for Manatashe to get his own way, especially when it comes to the vexed question of using Turkish power ships and making greater use of coal-fired plants. Only time will tell.

At the next SARB/MPC meeting on January 26, it is now widely anticipated that SARB governor Lesetja Kganyago will announce a softening of rate hikes from the tough 75 basis points of recent meetings to something closer to 50 basis points or even 25 basis points. Much depends on the perceived trajectory of US Fed Funds rates and currently it looks as though rate hikes in America are about to peak.

Locally, inflation continues its gradual downward trend, printing at 7.2% in December from 7.4% in November and a recent high of 7.8% in July. But it is still well outside the MPC’s target of 3% to 6%. Nevertheless, the trend remains encouraging.

NAAMSA domestic vehicle sales rose by 13.9% in 2022 compared with 2021. Passenger vehicles rose by 19.3%, due mainly to rental fleets re-stocking post-Covid to accommodate the return of international visitors.

Global Macro

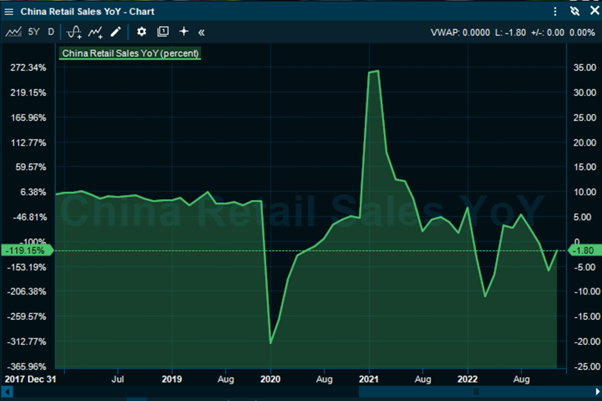

Chinese Q4 GDP figures surprised to the upside when released earlier this week. Against a consensus of a 1% contraction in Q4, the Chinese economy grew by 2.9%. This compares with 3.9% in Q3 and for calendar 2022, GDP growth in total was 3%. The big swing factor in this release was Chinese consumer spending, which bounced back strongly with the eventual abandonment of the Zero-Covid policy that had been in place previously. Retail sales growth, while still slightly negative, was a lot better than forecast.

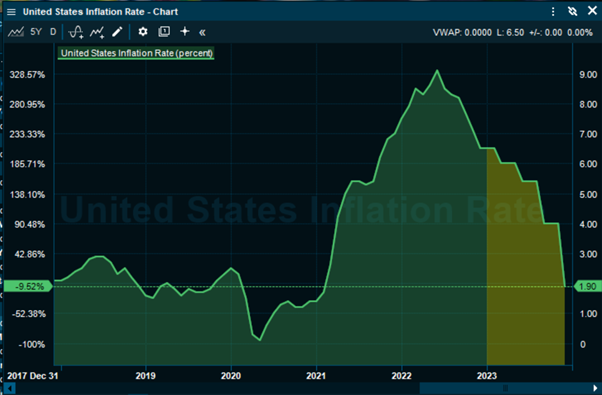

In the US, inflation as measured by the year-on-year change in CPI keeps falling. In December, inflation fell to 6.5% from November’s 7.1%. And although the jobs market remains strong and the US consumer keeps on spending, inflation appears to be coming under control. A mild recession, beginning in March this year, seems to be widely anticipated by economists. If inflation remains stable throughout 2023, interest rate cuts may begin before year-end.

Featured Stock

Featured Stock

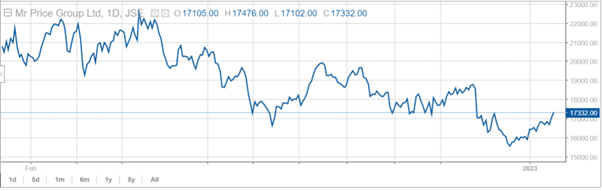

Mr Price recently released its interim results to 1 October 2022. Weaker than expected due mainly to a one-off blip associated with the implementation of ERP, a software programme, they were still reasonably good results, especially considering that this is a highly discretionary category of consumer spending. This result was also cycling a high base of comparison in the previous year, which made it difficult to maintain earnings, never mind increasing them slightly. And as was the case with rival TFG, rotational power cuts from Eskom took their toll, especially during the month of September.

Revenue rose by 6.5% to R13.3 billion, while the operating profit margin rose by 80 basis points to 14.7%. Diluted headline earnings per share rose by 10.8% to 486.1c and an interim dividend of 312.5c per share was declared, an increase of 10.6%

It was notable that Mr Price’s credit sales grew at the expense of cash sales (11.5% vs 5.2% for cash), suggesting that Mr Price's management as well as Mr Price's customers are becoming happier about using credit again. Having said that, there is no suggestion that Mr Price is about to become in any way reckless with its credit-granting procedures.

The next couple of years are going to remain tough for discretionary consumer retailers. But Mr Price and TFG, with their aggressive through-the-cycle acquisition programmes, appear better positioned than most to capitalise on what spending power is available in the SA economy.

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.