Local Macro

Locally, the SARB/MPC meeting resulted in a 75 basis point rise in the repo rate, taking it to 5.5% and prime lending rate to 9%. This is similar to where the repo rate was before the start of the coronavirus pandemic, although South Africa’s inflation rate now is significantly higher than it was two years ago, at 7.4% and thus it seems unlikely that this rate increase, as steep as it is, will be the last.

According to SARB governor Lesetja Kganyago, one of the most highly respected central bank governors in the world, three members of the MPC voted for a 75 basis point rise, one member voted for a 100 basis point rise and one member voted for a 50 basis point rise. Considering that South Africa’s inflation is mainly caused by imported factors such as fuel and food price -and not excessive demand, it is difficult to see the rationale for believing that raising interest rates will have the desired effect of containing inflation.

It is much more likely to depress what little growth is left in the SA economy to negligible levels. It will almost certainly suppress retail sales growth, which in turn will have an almost immediate negative knock-on effect on GDP growth. However, it should also help to slow down the depreciation of the rand, which in turn should help to contain inflation.

While the rest of the world is in a tightening interest rate cycle, there is little if any prospect of SA’s interest rates doing anything else but rising.

Global Macro

The global macro scene remains clouded in uncertainty, as the war in Ukraine drags on with no end in sight, inflation and interest rates keep rising around the world and in China, a regional banking crisis threatens to become systemic if not handled properly.

According to the World Bank, the war in Ukraine could soon deliver a tragic blow to many of the world’s poorest countries: many of the countries at greatest risk of a debt crisis are now grappling with the threat of a food crisis as well.

In its blog dated 18 July 2022, the World Bank says that food-import bills are surging fastest for poor countries that are already in debt distress or at high risk of it. Over the next year, the tab for imports of wheat, rice, and maize in these countries is expected to rise by the equivalent of more than 1 percent of GDP. That is more than twice the size of the 2021-2022 increase—and, given the relatively small size of these economies, it’s also twice as large as the expected increase for middle-income economies.

The danger of an overlapping food and debt crisis is greatest for seven countries in particular—those at high risk of debt distress or already in it: Afghanistan, Eritrea, Mauritania, Somalia, Sudan, Tajikistan, and Yemen. But several middle-income countries are at risk as well—including some that are already in the midst of a simultaneous debt and food crisis.

The poorest economies—particularly in Africa—happen to be exceptionally dependent on food imports from Russia and Ukraine. As many as 25 African economies, including several of the poorest, import at least one-third of their wheat from those two countries; for 15 of them the proportion is greater than 50 percent. The near-term scope for finding alternative sources within Africa is scant: the regional supply is relatively small—and transport infrastructure and storage capacity is limited in any case.

Debt, moreover, has been a rising problem for these economies—since well before the COVID-19 pandemic. By the end of 2020, the public and publicly guaranteed debt owed by these economies to foreign creditors stood at a record $123.8 billion, an increase of nearly 75 percent from 2010. The debt-service payments of these economies now constitute nearly 10 percent of their export earnings, up from less than 4 percent a decade ago.

In late July, a deal was brokered between Ukraine and Russia that would allow Ukrainian grain shipments to start being shipped from three Ukrainian ports, including Odesa on the southern Black Sea coast. No sooner had the ink dried on the deal than a Russian cruise missile struck a grain building in Odesa, so the outlook for a meaningful resolution of this deal is remote. For it to succeed, it would require Nato protection in the Black Sea and beyond, over and above the extensive de-mining of the area outside Odesa. In the meantime, poor people in Africa and elsewhere are going hungry.

As widely anticipated, the US Federal Reserve (The Fed) increased the Federal Funds rate by 75 basis points on July 27, the second such movement in as many months. Fed chair Jerome Powell is trying to keep a balance between avoiding recession while attempting to contain inflation via increasing interest rates. The next meeting of the Federal Open Market Committee is in September and Powell is keeping the door open to possibly raising rates by a further 75 basis points at that meeting.

Powell is of the opinion that inflation is already declining in the US as oil prices decline. This is probably a dangerous assumption, as oil and gas prices have been directly affected by the war in Ukraine and Vladimir Putin can confound markets pretty much at will. It is virtually impossible to second-guess Putin’s next move and anything is possible.

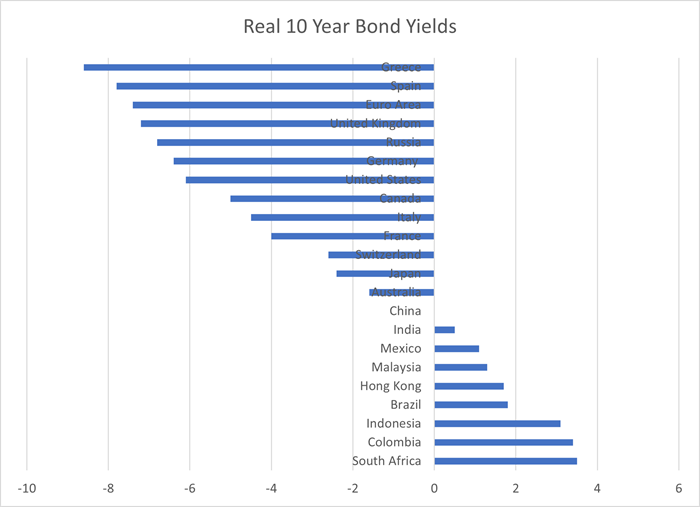

Globally, ten-year bond yields in most countries are now highly negative, as depicted in the graph below. Only a handful of countries, including South Africa, have managed to maintain positive real ten-year bond yields. As inflation remains elevated, interest rates will inevitably rise in an attempt to contain inflation and the current debate revolves around to what level interest rates will need to rise in order for this to happen. More and more people are coming round to the view that interest rates and going to have to rise significantly higher than current levels if they are going to have a meaningful impact on curbing inflation. But if that happens, the risk of recession looms ever larger. Some observers, such as former US treasury secretary Larry Summers, believe that a recession is the only way to deal conclusively with inflation. Only time will tell.

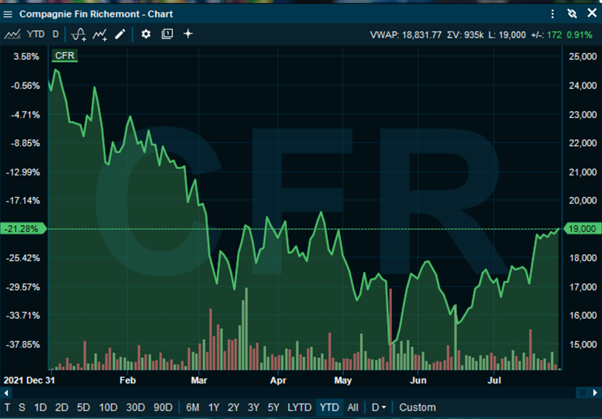

Featured Stock-Compagnie Financiere Richemont (CFR)

Featured Stock-Compagnie Financiere Richemont (CFR)

According to Reuters, activist fund manager Bluebell Capital Partners wants to change the composition of the Richemont board. Swiss-domiciled luxury goods group Richemont is controlled by the South African Rupert Family, notably Johann Rupert the chairman, via an intricate, though some would say archaic mechanism of B shares, whereby the Ruperts control Richemont by only holding 9.1% of the issued equity. These B shares carry 50% of the voting rights of the company. Bluebell is seeking to have both the A and B shares represented by the same number of board members, effectively conferring the same voting rights to A & B shares.

While Bluebell has had a degree of success in changing management at a number of European companies recently, including multinational food company Danone and French-headquartered multinational construction firm St Gobain, Richemont is an altogether different kettle of fish. Rupert and his father before him, Anton, were past masters at preserving control at what is now called Remgro but what used to be known as Rembrandt Group in the 1950s, 60s, 70s, 80s and 90s. Richemont was created in 1988 to house all of Rembrandt’s non-South African interests, hence it only has a depositary receipt structure for South African shareholders.

Richemont has said it will comment on the proposals, which will be submitted at the AGM on September 7 in Geneva. Even in the unlikely event that Bluebell is successful in its application, it is by no means certain that this will have a positive impact on the share price.

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.