Local Macro

Last week was an incredibly bad week for South Africa. As usual, the economic landscape was highlighted by Eskom, with the whole week being at stage 6 load shedding. These rotational power cuts have been a feature every day this year so far and there is no sign of either the intensity or frequency abating. This is an entirely unacceptable situation and it’s difficult to see how it ends.

The private sector has certainly made some important inroads into new electricity generation in the country but it is not, as yet, sufficiently advanced to make a meaningful difference to the overall energy requirements of the country. Some of the elements in the latest budget may help in this regard, notably the ability for corporates to claim back 125% of their expenditure on renewable energy for tax purposes. Individuals, too, get a tax break for installing roof-mounted solar arrays. It might be small but it’s a move in the right direction. The minister of finance also announced a debt relief package of R254 billion for Eskom.

Andre de Ruyter, Eskom CEO since 2019, gave an explosive interview on eNCA last week. De Ruyter leaves immediately following an explosive interview on eNCA last week in which he suggested that high-ranking members of the ANC were involved in Eskom-related corruption. That degree of frankness was never going to be tolerated and he was asked to leave his position immediately, instead of waiting to serve his notice period until end-March. He has been replaced as acting CEO by Calib Cassim former CFO at Eskom.

South Africa finally fell foul of the Financial Action Task Force (FATF) last week and was grey-listed by FATF. FATF is a global anti-money-laundering organisation and it had given SA plenty of notice that it intended grey-listing the country. To achieve global implementation of the FATF Recommendations, the FATF relies on a strong global network of FATF-Style Regional Bodies (FSRBs), in addition to its own 39 members. The nine FSRBs have an essential role in promoting the effective implementation of the FATF Recommendations by their membership and in providing expertise and input in FATF policy-making. Over 200 jurisdictions around the world have committed to the FATF Recommendations through the global network of FSRBs and FATF memberships. Since 2007 the ICRG has reviewed 125 countries and publicly identified (i.e. "listed") 98 countries. Of these 98, 72 have since made the necessary reforms to address their AML/CFT weaknesses and have been removed from the process.

The earliest date on which SA can hope to be removed from FATF’s grey list is January 2025. Between now and then, it will become tougher for South African corporates and individuals to invest offshore, as the level of scrutiny from prospective participants will be increased significantly.

Global Macro

US and EU inflation is proving to be stickier at elevated levels than anticipated by the market, even as recently as a few weeks ago. As a result, the USD is remaining stronger and puts pressure on EM currencies, such as the ZAR.

After years of wrangling with the EU over the unique position of Northern Ireland in a post-Brexit situation, it appears that the UK has managed to extract a deal.

In Ukraine, Russian forces appear to be gradually encircling the city of Bakhmut in the east of the country, in a grinding campaign that has cost many lives on both sides. There have been vague suggestions from China that it might supply Russia with arms and ammunition to help its campaign in Ukraine. Not surprisingly, America has criticized this potential move.

Featured Stock – City Lodge

After experiencing the double whammy of strict lockdown regulations as well as the highly dilutionary effects of a massive rights issue in 2020, City Lodge Hotel Group (CLHG) returned to profitability with the release of its interim results by the end of December 2022. It also paid a small dividend of 5c per share, which had not been widely expected by the market. Ordinarily, this would have been the cause of some celebration among battered shareholders but the reverse happened; on the day of the trading update, a few days before the actual results release, the share price dropped by around 10%. The reason for this weakness may lie in CLHG’s shareholder structure, where a lot of unsophisticated punters sell on any perceived strength in the price and thus drag it down. These “stale bulls” may take some time to shake out.

Average occupancy levels increased to 57% compared with 30% at the same point a year ago, while Average Room Rate (ARR) was 10% higher than a year ago. However, it was only 1% higher than in 2019. This highlights how difficult it has been to extract room rate increases during the past three years. Having said that, the calendar year-to-date ARR is 8% higher than the previous year.

For the six months to the end of December, CLHG earnings 17c in HEPS and paid out 5c in dividends. That HEPS figure included R27 million in business interruption insurance. Stripping that out leaves a figure closer to 14c/share. For the full year, HEPS is likely to be at least twice the earnings figure of H1, so somewhere between 28c and 34c HEPS seems reasonable. At the current share price of 447c, the prospective PE is therefore 14.4x.

The net replacement asset value per share, based on the insured value of the hotels, is 1060c.

City Lodge Historical Share Price Chart

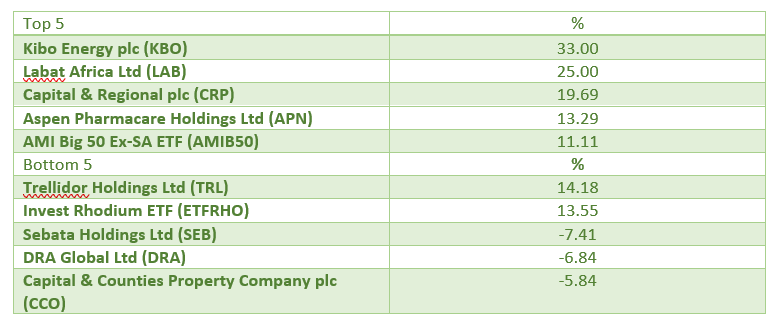

JSE Top and Bottom 5 (1 March 2023)

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

Learn and earn more today.

Visit our Education Centre