Local Macro

Locally, the big event last week was the Medium Term Budget Policy Statement (MTBPS), delivered by finance minister Enoch Godongwana. Traditionally, the MTBPS has been a relatively lacklustre affair, with the real meat being delivered in the national budget in February each year. However, this year’s MTBPS contained lots to digest. The primary budget deficit has been trimmed back from 6% of GDP in February to 4.9% at the time of the MTBPS. This improvement would have been even better had National Treasury not been required to spend an additional R37 billion sorting out balance sheet weaknesses in non-Eskom state-owned enterprises. So for example, . SANRAL will receive R23.7bn for debt settlement while Transnet will get R5.8bn to repair April flood-related infrastructure damage.

Although widely reported in the media as heralding the final scrapping of so-called e-tolls in Gauteng, that scenario doesn’t appear to have quite reached fruition-yet. By helping to settle SANRAL’s debt, National treasury has gone a long way down the road to effectively scrapping the disliked e-tolls but it is not clear at this stage how the Gauteng administration will manage to pay for road infrastructure without some kind of additional “user-pay” system. The obvious answer would be to apply a levy as the OUTA organisation has been suggesting all along. This would be a simple solution that doesn’t involve electronic gantries on the highways and which is collected automatically in the fuel levy.

The other big announcement in the MTBPS was that national government will assume a sizeable chunk of Eskom’s total debt, now standing at a colossal R400 billion. The rationale for this is that it should allow the utility to worry less about funding and concentrate more on operational matters such as reducing rotational power cuts (loadshedding in Eskom-speak).

The local markets generally liked the MTBPS, with local bond yields going lower on improved sentiment. This also helped sentiment towards the banking sector stocks.

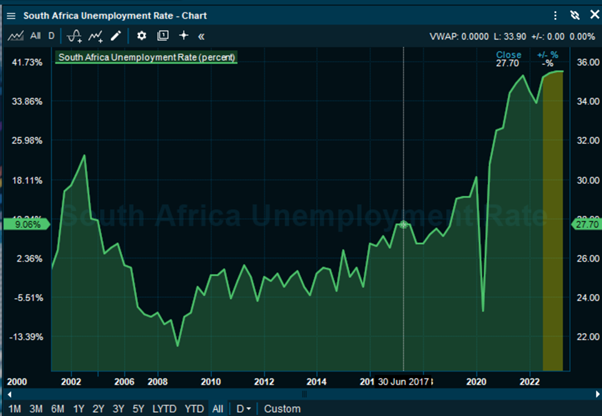

Delivering an address to the Wits School of Governance this week, SA Reserve Bank governor Lesetja Kganyago warned against pressuring the reserve bank into reducing interest rates inan attempt to revive the flagging SA economy. The governor made the point repeatedly that containing inflation is of paramount importance and if the SARB loses control, it will be extremely difficult in future to bring it down to acceptable levels. He also said that the country’s policy makers must find more practical solutions to reducing SA’s chronically high unemployment rate, the highest in the world.

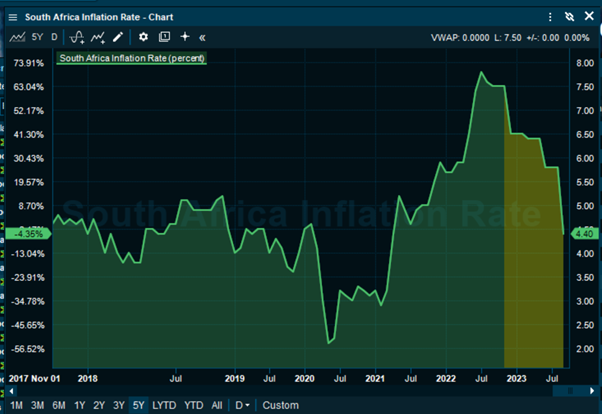

On a more positive note, he pointed out that inflation in the country may have peaked at 7.8% in July, since when it has fallen for two consecutive months.

Global Macro

Global Macro

In the UK, the long-running saga of revolving door prime ministers may have come to an end with the appointment of Rishi Sunak as leader of the Conservative Party and Britain’s prime minister, replacing Liz Truss, who was in office for less than 50 days. Sunak stands a better chance of succeeding in his new position than either Boris Johnson or Liz Truss but that doesn’t minimize the challenges associated with taking on this responsibility. UK inflation is high and rising, trade union unrest is as bad as it has been in a generation and mortgage and other interest rates are about to rise significantly. Add into the mix the likelihood of a five-quarter recession and the magnitude of the problems facing Sunak become much clearer.

The autumn statement (Britain’s version of SA’s MTBPS) has been delayed by two weeks and will be tabled by new chancellor Jeremy Hunt in mid-November. Meanwhile the Bank of England will likely hike interest rates by at least 75 basis points in early November.

In Brazil, Luiz Inacio Lula da Silva is president-elect of that country, following a very close election against incumbent Jair Bolsonaro. Lula, a left-wing politician and trade unionist, was president between 2003 and 2010

. He was jailed for allegedly being involved in money laundering, but after spending over a year in prison, the charges were eventually annulled and his political rights restored, allowing him to run for office again.

He was enormously popular in Brazil during his first presidency but he will need all of his vast experience and then some when he confronts the scale of the problems currently facing the Brazilian economy. And Bolsonaro and his supporters may not make life easy for Lula, with many large demonstrations occurring in the country.

Russia announced at the beginning of this week that it was backing out of the Turkey-brokered deal whereby Ukrainian grain would be allowed safe passage on ships from Black Sea ports. However, at least a couple of ships have set sail since the announcement with no apparent actions from the Russians. Later in the week, the Russians mounted a profound U-turn and agreed to honour the deal.

Chinese stocks ended lower on concerns that the new seven-man Chinese Communist Party politburo is packed with party loyalists rather than competent individuals. Tech stocks were especially hard hit.

Featured Stock

Clicks

Clicks, founded by the same person who founded Pick n Pay in the 1960s, Jack Goldin, turned in another predictably good set of results for the year to end August 2022. This is the most highly rated share in the retail sector of the JSE and investors are prepared to pay up for its resilience and predictable earnings and dividend growth. It rarely if ever shoots the lights out, it hardly has a a presence outside the borders of South Africa and yet this iconic retail pharmacy-oriented chain still manages to capture the hearts and minds of investors.

Group turnover rose by 6%, with retail turnover up 11.7% and 3.5% of that came from Covid-19 vaccinations. UPD, the pharmaceutical distribution side of the business, experienced a 2.6% drop in turnover from a high base in 2021. Operating margin rose from 8.2% to 8.4% and would have been higher had it not been for the impact of lower margin vaccinations.. Diluted headline earnings per share (HEPS) rose by 33.5% to 1 033c but if this is adjusted for the impact of the civil unrest in July 2021, this translates to 11.9%, which is still very respectable. The dividend was increased by 30% to 637 cents per share.

Market shares were gained in retail pharmacy, skincare, haircare, personal care and small electrical appliances, but slight market share was lost in the baby category. In the retail side, private label sales constituted 24.2% of total sales.

50% of the South African population is now within 5.3 kms or less of a Clicks pharmacy. Although at first glance this might suggest that Clicks is nearing saturation in the local market, the group still intends opening another 40 to 50 stores and pharmacies per year.

Gainers & Decliners

Gainers & Decliners

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.