Last week was action-packed, presenting numerous trading opportunities. This recap will cover the significant events of last week, the key data points to watch this week, and a review of the financial charts.

Geopolitical tensions in the Middle East caused massive price swings in the global markets, including cryptocurrencies, forex, stock indices and commodities. However, the markets stabilised soon after as it was clear that there would be no immediate retaliation efforts from Iran.

In the US, economic data suggests a delay in the anticipated Federal Reserve rate cuts. March's retail sales rose by 0.7% month-over-month, surpassing the expected 0.4%. The Empire and Philly Fed Manufacturing Indexes reached new highs, with the former hitting its highest level in nearly a year and the latter indicating elevated inflation levels.

Federal Reserve Chair Powell emphasised that restrictive policies need more time to take effect, suggesting that rate cuts may not occur soon, despite recent data hinting at a robust US economy. The first rate is likely not to happen until November or December according to the Fed Funds futures markets.

In contrast, European Central Bank (ECB) members have indicated potential rate cuts as early as June, independent of the Fed's actions. This has already impacted the EUR/USD pair, which is trading lower. In the UK, a higher-than-expected unemployment rate has pushed the British Pound to a new low for 2024, a trend that might persist in Europe and the UK.

Looking ahead to next week (London hours, BST):

Monday: ECB President Lagarde Speaks 16:30

Tuesday: EU Flash Manufacturing PMI 09:00, UK Flash Manufacturing PMI 09:30, US Flash, Manufacturing PMI 14:45, and Tesla (TSLA) AMC.

Wednesday: AU CPI 02:30, US Durable Goods Orders 13:30, and Meta Platforms (META).

Thursday: US GDP 13:30, US Unemployment Claims 13:30, Microsoft Corp (MSFT), and Snap Inc A (SNAP).

Friday: BOJ Policy Rate, SNB Chairman Jordan Speaks 09:00, US Core PCE Price Index 13:30.

EUR/USD

The EUR/USD has remained relatively stable compared to last week, though it did experience a bounce that presented short-selling opportunities. The price is still below the crucial level of 1.0732, which continues to define the bearish trend for the coming week.

GBP/USD

The GBP/USD has trended lower as anticipated, and the new trend-defining level has been adjusted from 1.2563 to 1.2514. Last week, the UK's central bank head noted a satisfactory decline in inflation, aligning with their targets, even as the UK unemployment rate worsened more than expected.

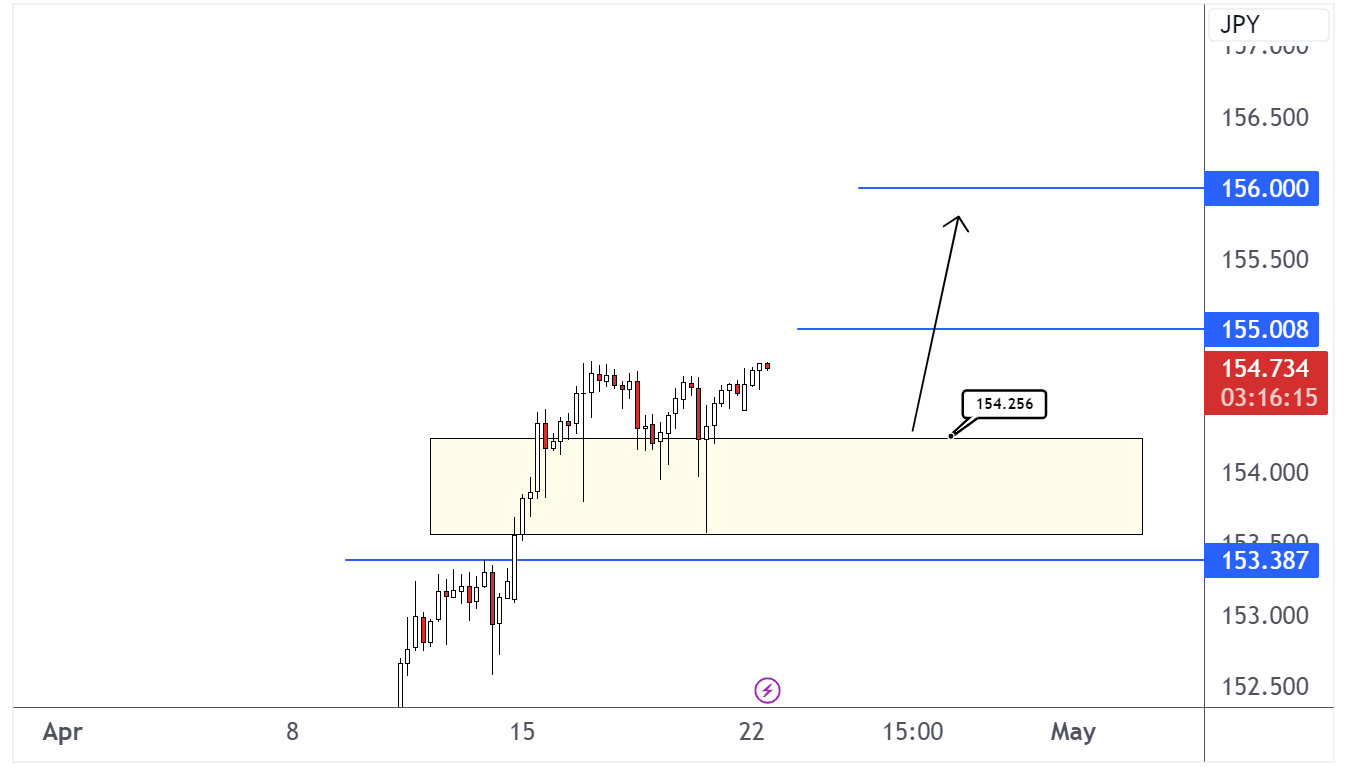

USD/JPY

The USD/JPY has risen, trading approximately 100 pips higher than the update provided last week. The trend-defining level has been raised from 152.56 to 153.38, indicating potential for further price increases if it remains above this new threshold.

Brent crude oil

Brent crude oil (BRENT) prices have fallen amidst market turmoil, yet the overarching bullish trend remains intact. The risk-reward ratio favours the upside in the $85.69 and $83.45 interval.

XAU/USD

Gold prices moved higher as expected last week, but as the new week begins, they are reverting to the same level seen early last week, maintaining a short-term bullish trend above $2317.

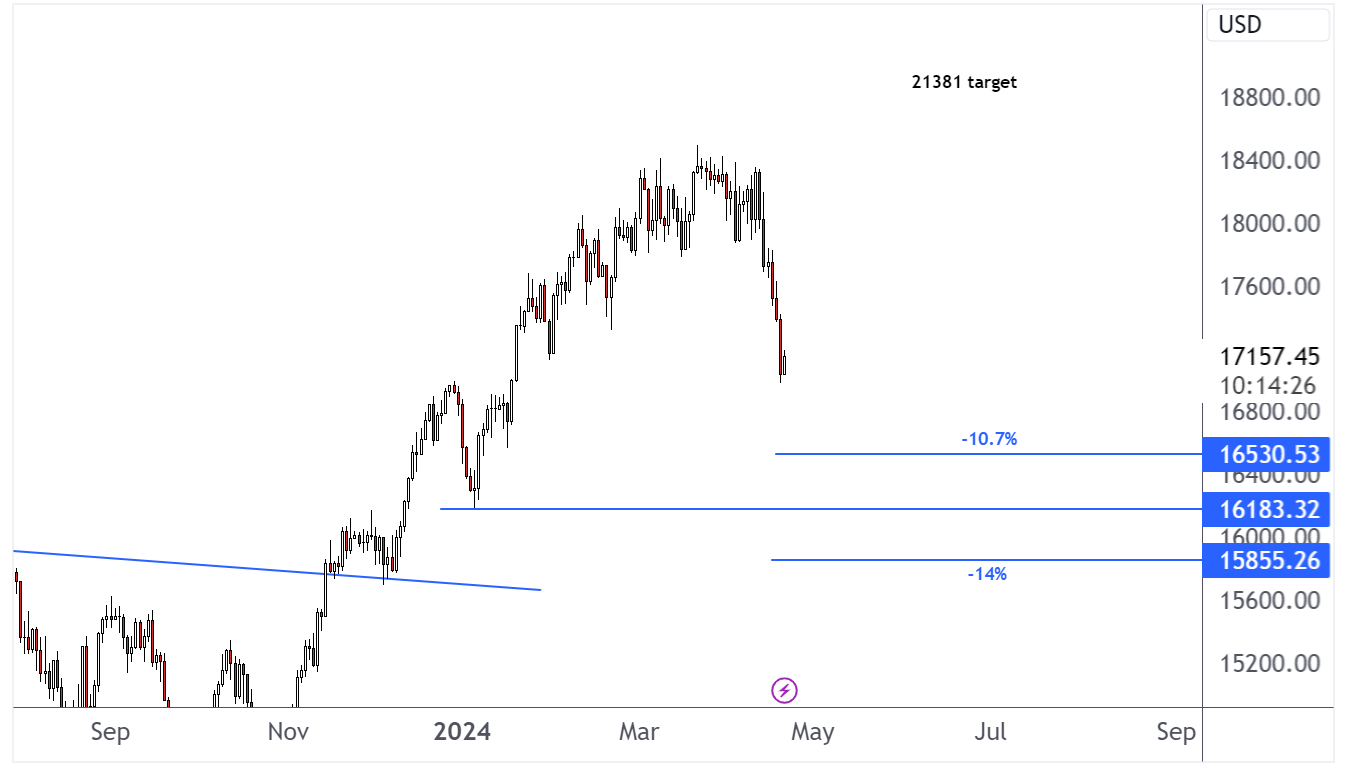

Nasdaq 100

The Nasdaq 100 (NAS100) has veered off its bullish course, experiencing notable declines. The index has found some support, yet typical corrections in a bull market suggest a further drop could occur. A standard 10.7% decline from its peak would position the index at approximately $16,530, while a more severe 14% fall would bring it down to around $15,855. These levels mark potential turning points for a rebound.

What is your take on the markets? Trade your view on ThinkTrader and access an extensive suite of technical analysis tools now!

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.