Download Carl's Bear Market Survival Guide e-Book:

https://www.thinkmarkets.com/au/lp/2023-bear-market-survival-guide-ebook/

This is possibly one of the most "forgone conclusion" FOMC meetings we've had since the Fed starting increasing interest rates in March last year.

Download Carl's Bear Market Survival Guide e-Book:

https://www.thinkmarkets.com/au/lp/2023-bear-market-survival-guide-ebook/

This is possibly one of the most "forgone conclusion" FOMC meetings we've had since the Fed starting increasing interest rates in March last year.

Why? Firstly, we've had a clear and consistent message from several Fed speakers over the last couple of weeks, each singing from the same hymn book. "Skip, not a pause" is the jargon they've used to give the market enough

carrot rates are going to be on hold at the June meeting today, but to also retain enough

stick to imply the Fed isn't necessarily done hiking rates just yet.

Skip, pause, jump, hop, stumble, flop. Whatever you call it, the market is pretty certain there isn't going to be another increase in the Fed's official cash rate at this June meeting. July? Well, that's another matter completely!

Secondly, the data generally shows a slowing in the US economy (albeit not necessarily in the labour market yet), and Tuesday's benign CPI print indicates the process of disinflation is well and truly underway. There's a very good chance the Fed simply wants to take a breath to observe its handy work – if only until their next meeting in a month's time.

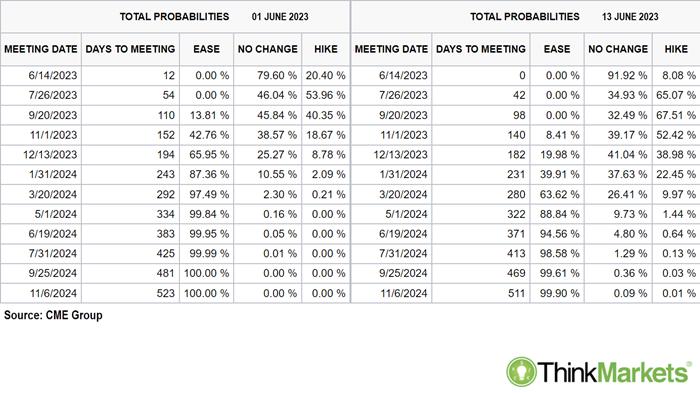

On this point, since the "skip, not pause" rhetoric emerged, the market has been pricing in an increased probability of a rate hike in July or August. We can see from the CME Group Fed Meeting Probabilities (based upon the Fed funds rate futures curve), the probability of a hike in July has increased from 54% at the start of this month, to 65% on 13 June. Respectively, the probability of an August hike has moved from 40% to 67%.

click to enlarge image

click to enlarge image

The other key takeaway from futures pricing is how dramatically the market has heeded the Fed's messaging they won't be cutting rates in 2023. Note how the probability of an "Ease" in September has narrowed from 14% at the start of the month to a flat-out 0% on 13 June. Similarly, an ease in either November or December has been all but ruled out (compared to relative certainty just a couple of weeks ago!).

It's the latter market shift (i.e., the factoring out of rate cuts this year) which has had a greater impact on US bond yields than the former (i.e., what's happening with potential hikes in the very short-term). The US 2-Year T-Note yield, which is a benchmark proxy for short-term interest rates in the US, has risen steadily over the past month. The gap between it and the official Fed funds rate has narrowed from as much as 128 basis points on 4 May, to 41 basis points currently. What you're seeing there is 2023 rate cuts evaporating into thin air…

Note, yields in many other countries have also risen over the same period, but for different reasons. Generally, it's stubbornly high inflation (e.g., the UK), or strong hawkish signaling from a central bank (e.g., Australia's RBA pausing/skipping in April and then delivering 2 further rate increases in May and June).

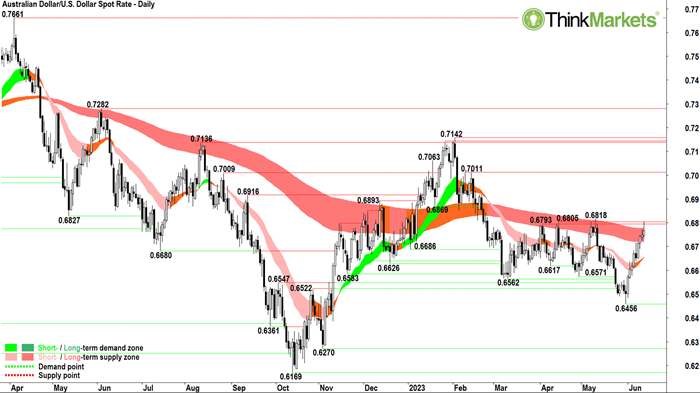

This means the rise in US yields has been largely matched by increases in the yields of other major currencies. In particular, the yield on the Australian 2-Year Government Bond has risen over 100 basis points since 4 May, relatively more its US counterpart's 87 basis point increase. This turnaround has triggered a major rally in the AUDUSD.

click to enlarge image

click to enlarge image

One country's 2-Year Government Bond yield has been notably absent from the recent gains – Japan. The yield on the Japanese 2-Year Government Bond (JGB) has been largely flat over the last month. Forex moves on relative yields, and more importantly, on changes in relative yields. It follows, we've seen general yen weakness against the other majors, particularly the AUDJPY.

click to enlarge image

click to enlarge image

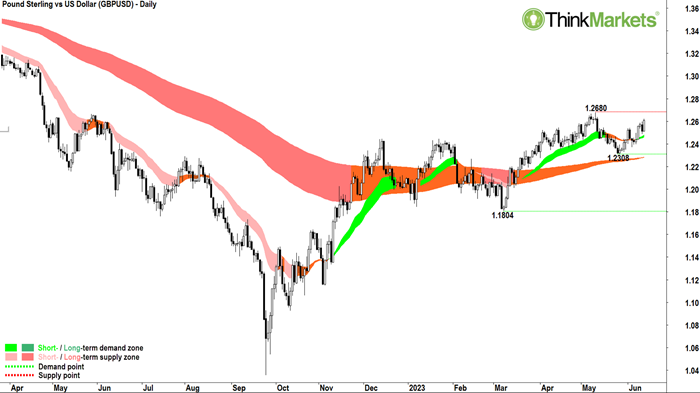

Another major yield winner of late has been the Pound Sterling. The yield on the UK 2-Year Government Bond has surged a whopping 120 basis points since 4 May, further widening the yield advantage of the Pound over the Yen (the 2-Year JGB has a

negative yield of -0.07%!). It is no surprise then the exchange rate with the best appreciation among the majors against the Yen since May is the GBPJPY.

click to enlarge image

click to enlarge image

Back to the US dollar and back to the Fed. If markets continue to firm up the case for another hike in July or August, and/or continue to push out the first potential rate cut well into 2024, expect US yields to remain strong, and therefore the US dollar to remain relatively buoyant against its crosses. If this thesis changes, perhaps because Fed messaging tilts towards a "pause-pause", not a "skip-pause", then we could see the US dollar weaken significantly against currency jurisdictions where the hiking cycle is still well underway (e.g., AUD, EUR, and GBP).

click to enlarge image

click to enlarge image

The Pound Sterling is once again probably the best bet against the US dollar. It's showing the best short-term uptrend against the Greenback compared to any of the other majors, and the long-term trend appears to also be turning higher. I'd be happy to add some long-side risk exposure here and some more on a close above the intermediate point of supply at 1.2680. There's really not a great deal of resistance on the chart until the October 2021 low of 1.3161. Stops could sensibly be set below the 1.2308 swing low.

Want your portfolio questions answered? Register for next week's Live Market Analysis sessions and attend live! You can ask me about any stock, index, commodity, forex pair, or cryptocurrency you're interested in.