It is rare for a central bank meeting to be such a foregone conclusion, but so it has been for many central bank meetings lately. Pretty much wherever you are in the world right now, Inflation is too high, and central banks primary monetary policy lever to fight inflation is hiking up interest rates.

On Wednesday, the bankers which make up the US Federal Open Markets Committee (FOMC) will meet to decide upon what economists expect will be another 0.25% increase to the Federal Reserve's (the "Fed's") key benchmark cash rate. It will be the eleventh increase since March 2021 bringing the total interest rate hikes over this time to 5.25%, and the official cash rate range to 5.25%-5.50%.

Click on image to enlarge

Click on image to enlarge

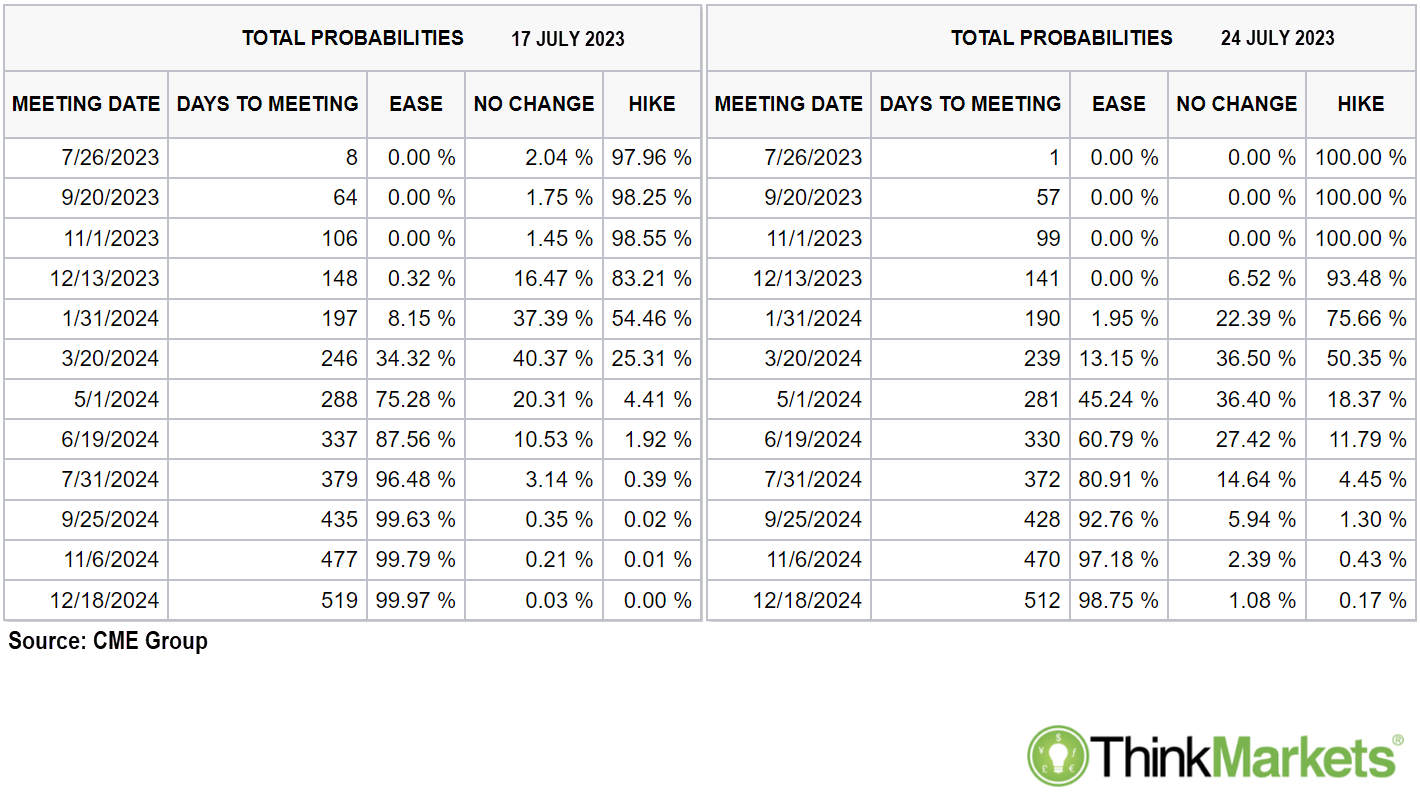

The table above shows market pricing reflects rare combination of probabilities for this and the next two meetings: 100% chance of a hike times three meetings. I cannot think of a time where the market was so certain about anything! Note however, these numbers don't necessarily imply we have three more interest rate hikes to go, rather that the probability is very high we will see at least one more hike at any of these meetings.

Markets assume a 0.25% hike on Wednesday is a given. If this occurs, we will likely see a moderation in the hike probabilities for the September and November meetings. Most economists believe we may see one rate hike at either of those meetings, or no hike at all. We will have to wait for the press conference to be hosted by Chairman Jerome Powell after the Committee meeting.

It is expected he will shift his rhetoric from the "

Multiple rate hikes to come" tone, which was prevalent after the FOMC's June pause, to either a "

One more", or potentially even a "

We can now afford to wait and see what impact previous rate hikes have on prices and the economy" tone.

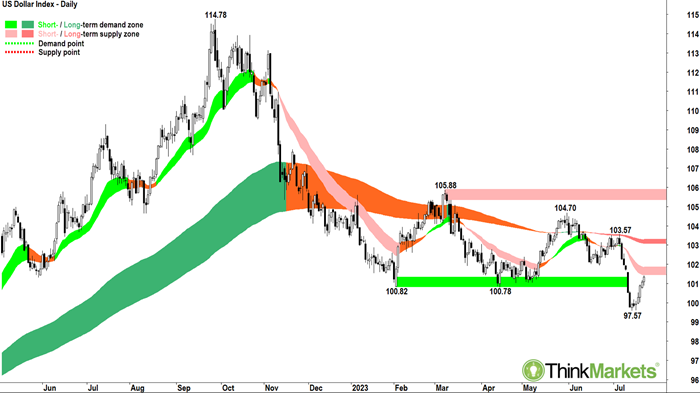

Either outcome will likely have a substantial impact on stock, bond, and forex markets. A "

One more" tone is likely largely factored in, but it should still see at least some improvement in stocks and bonds as US market yields grind lower. In this scenario, the US dollar would likely weaken modestly against the other majors.

Click on image to enlarge

Click on image to enlarge

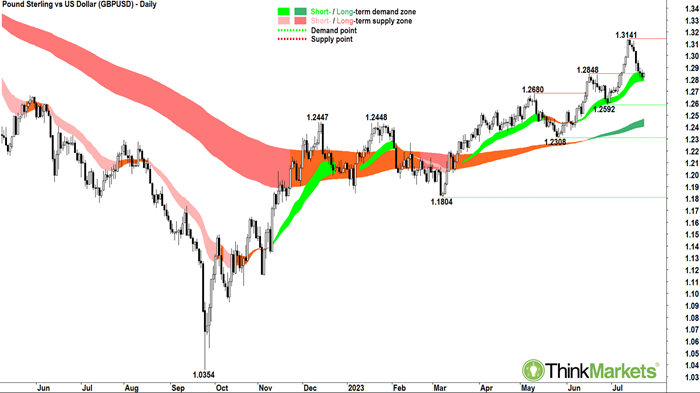

If we instead get a "

We can afford to wait and see" tone, this is the best-case scenario for stocks and bonds, and the worst-case scenario for the US dollar. Risk markets would love nothing more than an on-hold Fed. In this scenario, forex traders should look for long term downtrends in the US dollar against the Euro and the Sterling to reestablish after recent short-term pullbacks.

Click on image to enlarge

Click on image to enlarge

Click on image to enlarge

Click on image to enlarge

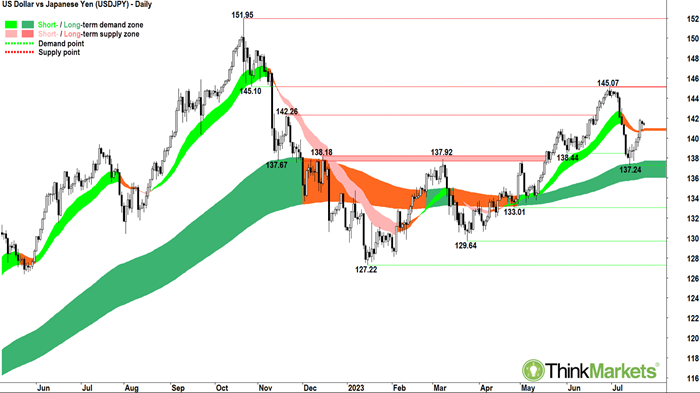

Finally, if we get a "

Potentially still multiple hikes to go" tone, this is the worst case scenario for stocks and bonds and the best case scenario for the US dollar. US market yields would likely spike, sending stocks and bonds sharply lower, and the US dollar sharply higher. This is the least likely of the three scenarios, but one which traders should be prepared for. If it does turn out to be the case, I would be looking for US dollar longs against the weakest of the majors, the Japanese Yen.

Click on image to enlarge

Click on image to enlarge

My bet is we see either a "

One more" or a "

We can afford to wait and see" message from Chairman Powell. Either way, he is going to continue to talk tough on inflation whilst acknowledging the disinflationary process is well under way. He may even begin to talk up the chances of a soft landing in the US economy and this will likely also bolster confidence among investors (i.e., leading to a positive stocks and bonds versus negative US dollar posture in markets).