Market Sentiment

Global stock markets produced their best first-quarter performance in five years in Q1 2024. For markets that were already stretched in terms of valuation, this is quite a performance. In ZAR terms, the standout feature in March was gold, which returned +6.7% and was the best-performing traditional asset class.

India, China and Middle Eastern central banks are all buying gold in an attempt to diversify away from US dollar assets. However, that demand is capricious and could evaporate at any time. Thus, it’s important to realise that the gold price may not be a one-way bet forever and speculators should not get too attached to the yellow metal. If and when central banks begin dumping gold, the price will likely drop quickly.

FAANG stocks fell by 0.4% in March. Tech stocks, notably particularly Apple (AAPL), had a bad March, with iPhone sales being down in China and the company being targeted for antitrust behaviour by the US Justice Department.

Global bonds and South African bonds were both down in ZAR terms for the month of March.

Tesla (TSLA)’s share price has more than halved in the past two years and there are no signs of that trend reversing any time soon. Indeed, the share has fallen by more than 33% since the beginning of the year and it is the worst-performing stock in the Nasdaq 100 (NAS100) so far this year. It is also the second-worst performing stock on the S&P 500 (SPX500) this quarter. The reasons for the most recent share price decline appear to be both industry-related and Tesla-specific.

Electric vehicle (EV) sales growth in the US slowed to only 2.7% in Q1 2024, compared to 47% growth for the full year 2023. This has resulted in a drop in EV market share from 7.6% at end 2023 to 7.1% in Q1 2024. Major specialist EV makers Tesla and Rivian missed production estimates due to slowing EV demand. Tesla's sales fell 20.2% quarter-over-quarter and 8.5% year-over-year.

Several US automakers such as GM, Ford, and Mercedes USA have attenuated previously announced EV goals due to slowing demand and higher costs. Concerns about EV range limitations and lack of robust US charging infrastructure are also making consumers apprehensive about adopting EVs.

So, for example, GM reported approximately a 20.5% drop in EV sales for Q1 2024 in the US, selling only 16 425 vehicles. EVs contributed only 2.8% to GM's total US vehicle sales of 594,233 units in Q1 2024.

In comparison, Tesla reported an 8.5% year-over-year decline in global deliveries for Q1 2024, delivering 386 810 vehicles compared with an anticipated figure of 457 000. However, Tesla sold 17 027 units of its higher-end Model S, Model X, and Cybertruck vehicles, a 59.2% increase from Q1 2023. Tesla's lower-priced Model 3 and Model Y sales dropped 10.3% year-over-year, dragging down overall deliveries.

Tesla-specific problems included Houthi militia attacks on ships in the Red Sea disrupting Tesla’s component supply and temporarily suspended production at its German factory outside Berlin in January 2024.

Local Macro

According to Reuters, South African Reserve Bank (SARB) governor, Lesetja Kganyago, says he would prefer to establish a lower inflation target range than the current 3-6% before 2025. The current inflation target was introduced in 2000 and most economists at the time believed this was not an especially onerous target for the SARB to achieve. In fact, there were plans to lower this target range, firstly to 3-5% and then to 2-4%.

Governor Kganyago reckons it was a missed opportunity that the target was never lowered. The SARB currently has an objective of 4.5% (the midpoint of the 3-6% target) but expressed the view that it would prefer to see inflation at 3%. Inflation was 5.6% y-o-y in February, and the SARB forecasts it to slow to 4.5% only in 2025Q4.

If such a policy of lowering the target inflation band is instituted, the likely effect is that interest rates will take even longer to come down than would otherwise have been the case.

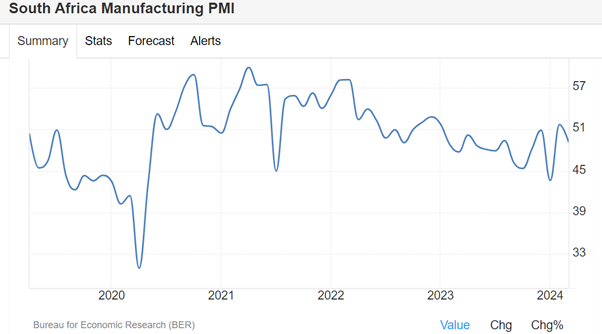

The Absa PMI-a gauge of factory activity-slipped back to below 50 points in March 2024. The headline index declined from 51.7 in February to 49.2 in March. Following robust improvements in February, both the business activity and new sales orders index declined – although the indices remained above recent lows seen in January.

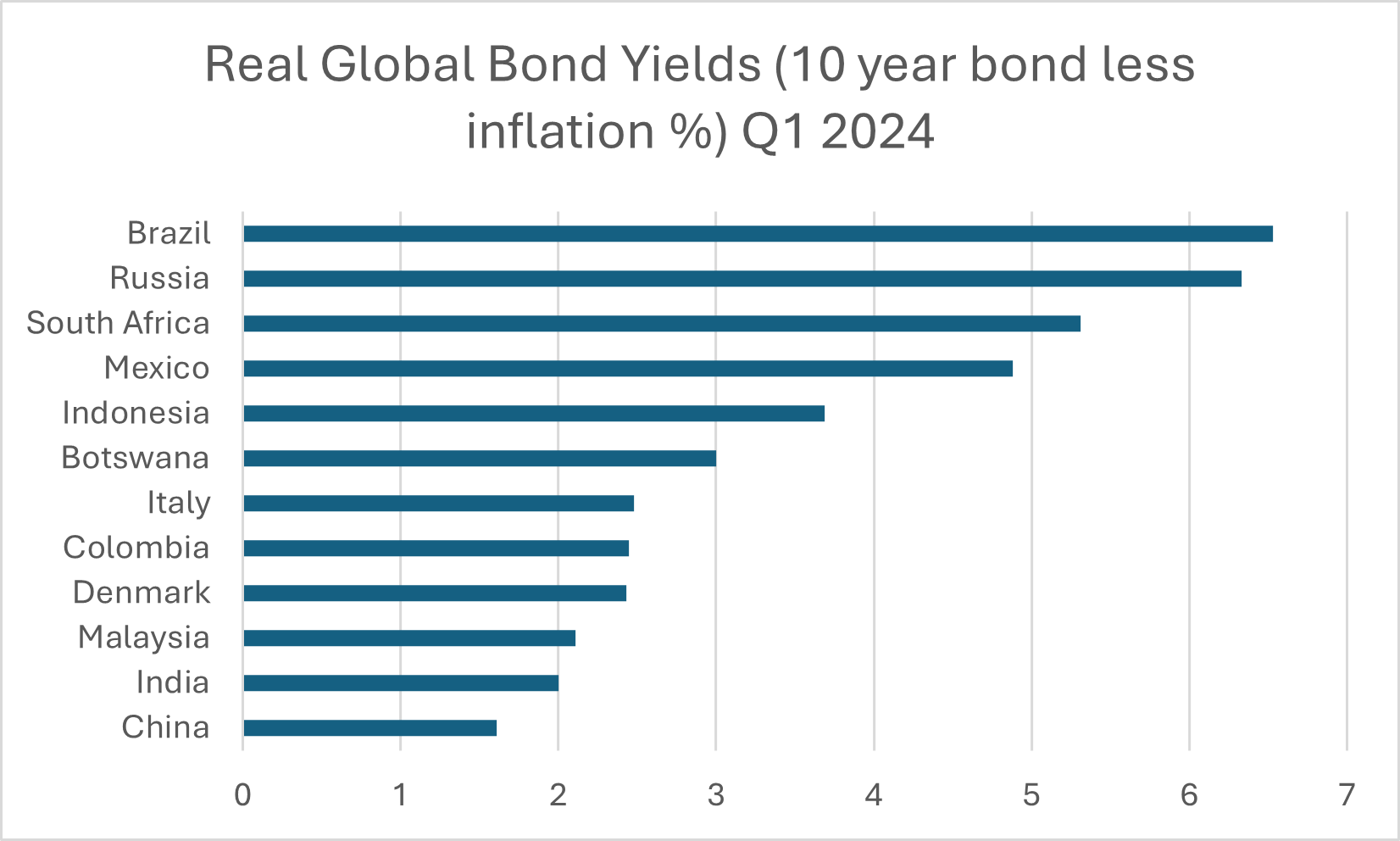

The real bond yield in SA is high but is it high enough to keep attracting foreign money? Only time will tell and the outcome of the election on 29 May will be critical not only in determining whether capital flows remain intact, but also the direction of the rand (ZAR).

As can be seen from the chart below, the South African 10-year real bond yield is not the highest among developing countries. Brazil and Russia both have higher real bond yields and Mexico’s 10-year real bond yield is not far behind South Africa’s. It is therefore vitally important that South African bonds remain attractive to foreigners especially.

Global Macro

The US is probably heading for a soft landing and Fed chair Jerome Powell is starting to make increasingly dovish noises about interest rate moves. However, there are some conflicting economic signals coming out of the US. For instance, the US consumer is running out of cash; the latest US retail sales were below consensus, money and credit growth are weak, delinquency rates for non-mortgage rates are rising and banks have tightened lending requirements. Non-mortgage debt payments have surged.

Total nonfarm payroll employment rose by 303 000 in March, and the unemployment rate changed little at 3.8 percent, the U.S. Bureau of Labor Statistics reported last week. Job gains occurred in health care, government, and construction. The number of long-term unemployed (those jobless for 27 weeks or more), at 1.2 million, was little changed in March. The long-term unemployed accounted for 19.5 percent of all unemployed people. The Employment Situation for April is scheduled to be released on Friday, May 3, 2024, at 8:30 a.m. (ET).

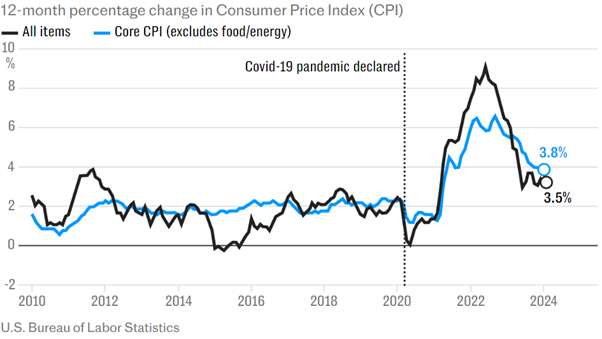

And US inflation in March surprised to the upside, coming in at 3.5% year on year compared with 3.2% in February. This has spooked US markets, which were anticipating 3.4%. A growing consensus is now emerging that sees only two interest rate cuts in America this year, with the first US interest rate only occurring in September.

In contrast to the US, UK inflation appears to be slowing. Inflation in shop prices in the UK has eased to the lowest level for more than two years after retailers cut prices on Easter presents, clothing and electrical goods amid a slowdown in spending by consumers in the cost-of-living crisis.

Industry figures show prices rose at an annual rate of 1.3% in March, down from a rate of 2.5% in February – the slowest pace since December 2021, according to the latest monitor from the British Retail Consortium (BRC) trade body and the market research firm NielsenIQ.

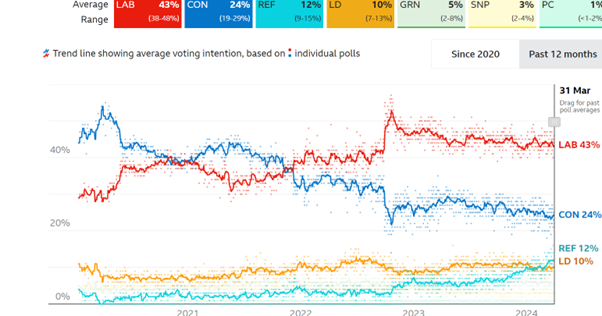

The UK general election will probably only be held in the autumn, but the BBC’s Poll of Polls is showing unequivocally that the governing Conservative Party is trailing badly on current polling intentions.

It is not clear what the impact on the London Stock Exchange will be in the wake of the election result, but markets don’t like uncertainty. The likelihood of a strong showing by the opposition Labour Party appears to be growing, as shown in the long-term graph below. The London Stock Exchange appears to have absorbed this likelihood without any particular concern, judging from the relatively stable performance of the FTSE 100 (UK100) index over the past couple of years.

The opposition Labour Party has an almost 20-point lead. If replicated in a general election, that would translate into a landslide victory for Labour. The other main feature of this poll is the very strong showing of the Reform Party, which is currently polling at 12%, slightly ahead of the Liberal Democrats. But because Britain has a First Past the Post electoral system, rather than proportional representation, a strong showing by minority parties such as Reform or the Liberal Democrats doesn’t translate into a significant number of seats in the House of Commons.

A better indication of what may happen in the UK general election will occur in the local government elections in England on 2 May.

Fitch Ratings has revised its outlook on China’s debt to negative from stable. This follows a similar action by Moodys in December last year. The ratings agency fears that China will increase its debt levels further in order to pull the Chinese economy out of a real-estate-driven slowdown.

Needless to say, Chinese authorities are unhappy about this de-rating as they attempt to boost confidence and stem capital outflows.

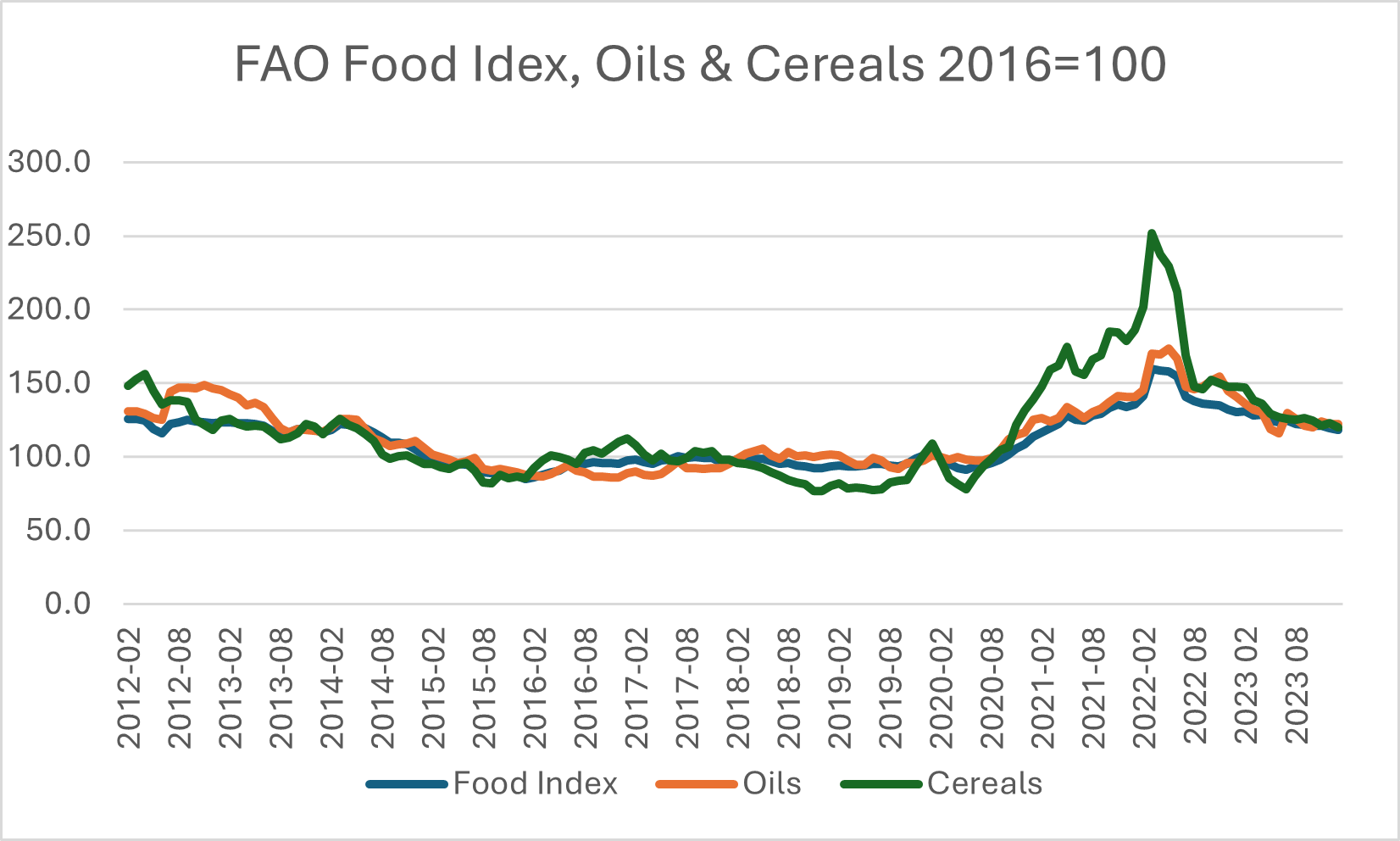

The cocoa price continues to rise, reflecting the worsening supply situation in West Africa due to the combined effects of climate change and El Nino. Other soft commodities are also suffering because of El Nino, though this is not reflected in USD-denominated prices of cereals and vegetable oils, as shown in the latest UN Food & Agricultural Organisation (FAO) food index charts. Cereal production generally hasn’t been as badly affected by El Nino as originally feared. But certain Southern Africa countries have been ravaged by drought and crop yields are right down.

Zimbabwe is the latest southern African country to declare a state of disaster, following the devastating drought exacerbated by the El Nino effect. This follows similar proclamations by Malawi and Zambia.

In a separate announcement, the Zimbabwe Reserve Bank launched a new, gold and foreign currency-backed currency called rr Gold (ZiG). The intention is to reduce the crippling rate of inflation in Zimbabwe to something more manageable. The ZiG will circulate alongside other foreign currencies in Zimbabwe. The Zimbabwe Reserve Bank also announced that its main interest rate would be set at 20%, down from the previous 130%.

Featured Stock

Truworths is an old-established clothing, footwear, textiles & apparel (CFTA) retailer, with operations in southern Africa and the UK/Europe (with Office). Most of its sales are targeted at a slightly more affluent consumer and in South Africa, it is the leading credit-oriented CFTA retailer, with the bulk of its sales until recently being made on credit. Of the three main JSE-listed CFTA retailers, Truworths is the smallest, being significantly smaller in terms of turnover, profit and market capitalisation than Mr Price or TFG.

During the 26 weeks to 31 December 2023, group retail sales increased by 8.2% to R12.2 billion compared to the first 26 weeks (from 4 July 2022 to 1 January 2023) of the 2023 financial period. Account sales comprised 48% (Dec 2022: 52%) of group retail sales, with account sales unchanged and cash sales increasing by 17%, relative to the prior period. This highlights that consumers are debt-averse due to the historically high interest rates.

Retail sales for the group’s UK-based Office segment increased in pound terms by 15.6% to £162 million relative to the prior period’s £140 million. In rand terms, retail sales for Office increased by 33.1% to R3.8 billion. Online sales contributed approximately 47% of Office’s retail sales in the current period, increasing from 44% in the prior period.

The group’s gross profit margin increased to 53.6% (Dec 2022: 53.5%). Truworths Africa’s gross profit margin increased to 56.6% (Dec 2022: 56.0%) and Office’s increased to 47.4% (Dec 2022: 46.6%).

Group trading profit, which excludes interest income, increased 1.5% to R2.2 billion. The trading margin decreased to 18.8% from 20.1% in the prior period. Other income decreased 18.1% compared to the prior period. Excluding the reversal of previously recognised IFRS 16 impairment losses from both periods as well as the insurance claim payments received in the prior period relating to the civil unrest in South Africa during July 2021, other income increased by 1.0%.

Group net debt decreased from R854 million at the prior period end to R124 million at the current period end. Net debt to equity and net debt to EBITDA decreased to 1.4% (Dec 2022: 11.8%) and 0.0 times (Dec 2022: 0.1 times), respectively. The cash realisation rate which is a measure of how profits are converted into cash, was 93% for the current period (Dec 2022: 56%).

Finance costs increased by 36.7% to R216 million (Dec 2022: R158 million), due to higher borrowing levels together with higher interest rates in the Truworths Africa segment to fund working capital requirements, as well as an increase in IFRS 16 finance costs due to new and renewed leases.

Both headline earnings per share (HEPS) and diluted HEPS (DHEPS) for the current period increased by 3.6% to 512.6 cents and 504.8 cents, respectively, compared to the prior period’s 494.6 cents and 487.4 cents, respectively. An interim dividend of 332 cents per share has been declared (Dec 2022: 320 cents per share), maintaining the dividend cover at 1.5 times.

Group net debt decreased from R854 million at the prior period end to R124 million at the current period end. Net debt to equity and net debt to EBITDA decreased to 1.4% (Dec 2022: 11.8%) and 0.0 times (Dec 2022: 0.1 times), respectively. The cash realisation rate which is a measure of how profits are converted into cash, was 93% for the current period (Dec 2022: 56%).

Sustained pressure on the discretionary spending of South Africans, electricity load shedding, ongoing port congestion and international shipping disruption remain risks to the trading performance in the second half of the financial year. Global shipping disruption has also affected the delivery of imported merchandise for the first half of the winter season (January to March 2024).

As far as Office is concerned, current indicators show that interest rates and inflation are expected to decline in the 2024 calendar year, which should benefit UK consumer disposable income. Trading space is projected to increase by 12% for the 2024 financial period.

Truworths is relatively cheap, on a PE ratio of 8.4x at the current share price of 7 453c. But it’s been cheap for a while now and may remain so until interest rates start declining sustainably, allowing Truworths to get the full benefit of its credit book once again.

Ready to trade? Log in to ThinkPortal now!

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.