Local Macro

Following the historic Springbok victory in the Rugby World Cup in Paris at the weekend, it’s back to business with a thump this week in South Africa. The big feature this week is the Medium-Term Budget Policy Statement (MTBPS), delivered by the Minister of Finance, Enoch Godongwana, last Wednesday, 1 November.

The task facing the minister was truly daunting. He faced a budget shortfall. The solutions to overcome this problem were to raise taxes, reduce spending, or increase borrowing. Ultimately, his choice was to increase borrowing.

Raising taxes before the 2024 election would not be ideal, although many observers thought it was a distinct possibility. Cutting down on unnecessary expenses, while a cardinal principle in governance, is difficult to achieve in practice. Government debt to GDP will soon hit 77% and interest payments on this debt will consume over 22% of expenditure – far more than the budget for education, police, or healthcare.

The forecast growth in 2024 is 0.8%, down from the previous rate of 0.9%, and nowhere near what is required for a developing economy. The Minister talked about enhanced participation of the private sector in the economy but gave no further details.

Global Macro

Two main factors are at work on the global economic front this week; major central banks are making interest rate decisions, while the oil price remains weak, even in the face of continuing tensions in the Middle East surrounding the Israeli/Hamas conflict. There can be little doubt that interest rates are destined to stay higher for longer, the only question being when will they peak and begin to fall

Source: Trading Economics

Source: Trading Economics

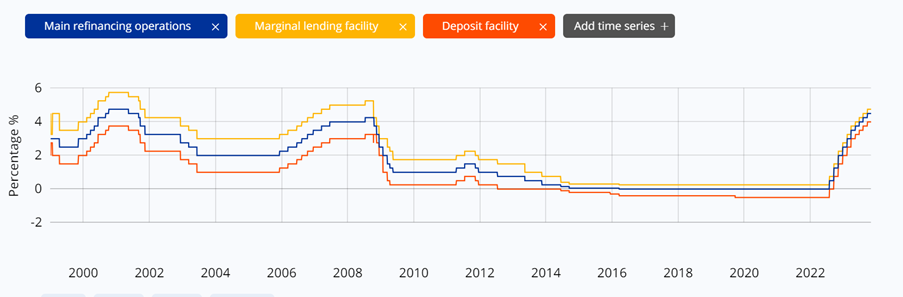

On 26 October 2023, The Governing Council of the European Central Bank (ECB) decided to keep the three key ECB interest rates unchanged. Inflation is still expected to stay high, and domestic price pressures remain strong. At the same time, inflation dropped markedly in September, due to strong base effects and most measures of underlying inflation have continued to ease. The Governing Council’s past interest rate increases continue to be transmitted forcefully into financing conditions. This is increasingly dampening demand and thereby helps push down inflation.

The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility remain unchanged at 4.50%, 4.75% and 4.00% respectively.

Source: ECB

Source: ECB

The US Federal Reserve (The Fed) is meeting this week to discuss and set US interest rates. At its Federal Open Market Committee (FOMC) meeting last 1 November, the Fed decided to leave rates steady.

“The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 5-1/4 to 5-1/2 percent. The Committee will continue to assess additional information and its implications for monetary policy. In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. In addition, the Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage-backed securities, as described in its previously announced plans. The Committee is strongly committed to returning inflation to its 2 percent objective.”

The Bank of England (BoE) met last 2 November to determine the UK’s policy rate. It sems likely that it will follow the lead of the ECB and continue to pause rate increases. Having said that, all indications coming out of the BoE are that interest rates are likely to stay higher for longer.

The BoE’s Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment.

At its meeting last 20 September 2023, the MPC voted by a majority of 5–4 to maintain bank rates at 5.25%. Four members preferred to increase Bank Rate by 0.25 percentage points, to 5.5%. The Committee also voted unanimously to reduce the stock of UK government bond purchases held for monetary policy purposes, and financed by the issuance of central bank reserves, by £100 billion over the next twelve months, to a total of £658 billion.

Featured Stock

Clicks, the largest retailer of pharmaceuticals and related products, released reasonable full-year results for the year to end August last month. Turnover grew by 5.1% to R41.6 billion while the gross margin grew by 10.5% to R9.3 billion. Headline earnings per share (HEPS) rose by 1.1% to 1 044.5c and the dividend was increased by 2.8% to 185 cents per share.

Although impacted to an extent by loadshedding, Clicks was far less exposed than the food retailers, as it doesn’t have much in the way of refrigerators in its stores that require to be kept going by diesel generators.

The group opened its 850th store during the financial year and its 711th pharmacy.

While the share price has come off a lot from its peak of a couple of years ago, it is still expensive, especially relative to its comparatively low earnings growth. Nevertheless, investors appear to like it because of its solid track record and its ability to generate cash.

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.