A snapshot of overnight moves and a look to the upcoming Australasian session for 26 August.

Market Moves

Wrap

US markets were broadly higher as gains in tech stocks defied weaker than expected consumer confidence data (see Macro Economy).

The tech-heavy NASDAQ was once again the leader, it closed up 0.76%, the benchmark S&P500 gained 0.36%, but the blue chip-laden Dow Jones Industrial Index fell 0.21%.

Risk on assets were mainly in favour, helping metals prices on the LME higher. Aluminium, Copper, Lead, Nickel, and Zinc each saw approximately 0.5-1.0% gains. Copper also saw a 0.51% gain in New York.

Iron Ore prices were weaker though. The September contract on the Chinese Dalian Exchange fell 1.89%, whilst iron ore traded 2.60% lower in the Singapore-based $US price.

Precious metals had a very quiet session. Spot Gold rose 0.07% to US$1927.68/oz, whilst Silver gained 0.02% to US$26.42/oz.

Energy commodities were the standouts on Monday. West Texas Crude added 2.30% to US$43.45/barrel, Brent gained 1.92% to US$46.29/barrel, whilst Natural Gas was 1.67% lower.

In currency moves, the Australian Dollar retreated improved 0.40% to 0.7194 as the US Dollar Index declined 0.30%.

Risk off bonds rose fell, with the yields on the US 10 year Treasury Notes rising falling 3.4bp to 0.688%.

So with a reasonably clear risk on move in overseas drivers, where did the ASX200 Share Price Index end up? Well, it had a most lacklustre session, closing at 6094 compared to an overnight session high of 6144 and a low of 6073.

That's a 67.4 point discount to yesterday's ASX 200 close of 6161.4, and predictive of approximately a 0.5% fall at the open for the S&P ASX200.

AU Companies

Whispir (WSP)

The company reported this morning that it had enjoyed higher recurring revenue, customer growth and customer retention.

The software and communications company delivered a 34% increase in recurring revenue to $42.2m, ahead of prospectus forecasts, but not enough stave off a loss of $5.6m. This loss was however an improvement of 25.5% over the previous corresponding period (PCP).

Various

Other companies reporting this morning include:

Adbri (ABC), AMA Group (AMA), Bravura Solutions (BVS), Cardno (CDD), Cleanaway Waste Management (CWY), Japara Healthcare (JHC), Macmahon (MAH), Perseus Mining (PRU), Readytech (RDY), Seven Group (SVW), and Worley (WOR).

Broker Moves

| Ansell |

ANN |

Citi raises Ansell (ANN) price target from $35.00 to $41.00. |

| Bingo Industries |

BIN |

Citi lowers Bingo Industries (BIN) price target from $3.00 to $2.80. |

| Integral Diagnostics |

IDX |

Citi raises Integral Diagnostics (IDX) price target from $4.90 to $5.35. |

| Integral Diagnostics |

IDX |

Jefferies raises Integral Diagnostics (IDX) price target from $4.00 to $4.10. |

| Opthea |

OPT |

Goldman Sachs retains buy rating on Opthea (OPT). Retains $5.20 price target. Notes strong balance sheet and prospective clinical trial pipeline. |

| Qube |

QUB |

Jefferies raises Qube (QUB) price target from $2.85 to $2.91. |

| Seven Group |

SVW |

Jefferies raises Seven Group (SVW) price target from $0.070 to $0.140. |

| ST Barbara |

SBM |

Goldman Sachs raises ST Barbara (SBM) price target from $4.30 to $4.40. Retains buy rating. Expects operational environment to continue to improve. Sees lower costs to support margins. |

| Stockland |

SGP |

Jefferies downgrades Stockland (SGP) rating from buy to hold. Raises price target from $3.81 to $4.11. |

| Super Retail Group |

SUL |

Goldman Sachs raises Super Retail Group (SUL) price target from $10.30 to $11.60. Retains buy rating. Broker is impressed with management's ability to defensively position the business. Upgrades EPS estimates for FY21 by 6% and FY22 by 11.5%. |

| Western Areas |

WSA |

Citi lowers Western Areas (WSA) price target from $2.70 to $2.65. |

| Xero |

XRO |

Jefferies raises Xero (XRO) price target from $81.24 to $92.86. Retains hold rating. |

Macro Economy

Today, we'll see data on Australian construction work at 9.30am EST. Later this evening, we'll see some key data on the US economy in the form of durable goods orders.

Below is a summary of the key macroeconomic data releases from the past 24 hours.

USA

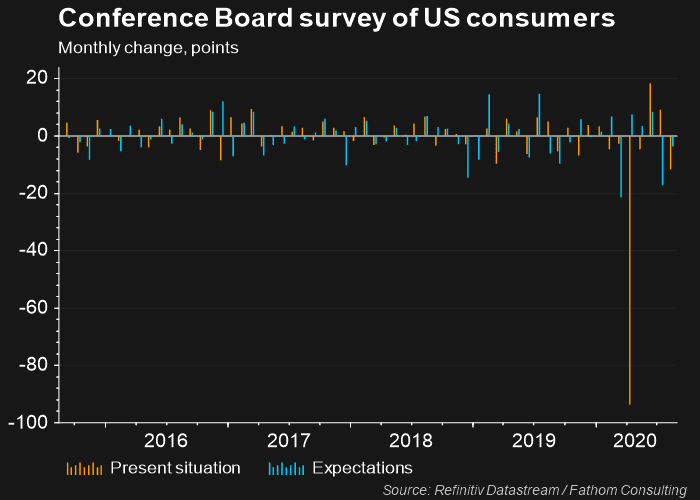

The Conference Board reported Monday that US consumer confidence likely fell in August. The CB Consumer Confidence Index plunged to 84.8 compared to 91.7 in July.

Consumers' opinion of their current situation were hardest hit, as the Present Situation Index fell to 84.2 from 95.9. If there was a positive in the report, it was that the Expectation Index fell at a more modest rate, dropping to 85.2 from 88.9.

According to Conference Board, consumers noted that both business and employment conditions had deteriorated over the past month.

-United-States.png.aspx)

Sales of new single-family houses in July increased to 901k, according to the US Census Bureau and Department of Housing. This was nearly 14% higher than June and well ahead of the 785k figure markets were expecting.

The data follows up better than expected numbers on building permits and housing starts released last week, and continues a trend of substantial strength in the US housing market.