On Tuesday 5 December, furniture and homewares retailer Nick Scali (NCK) reported to the market that net profit after tax (NPAT) for the six months to the end of December 31 2020 would be $40.5m, up approximately 100% on the previous corresponding period (PCP).

Management noted that better than expected container availability during November and December had facilitated increased delivery volumes. Sales were also ahead of expectations, and appeared to be accelerating in the second quarter. The company’s sales book was at an all-time high at the end of the first half, and this would likely result in significant revenue and profit growth into the second half.

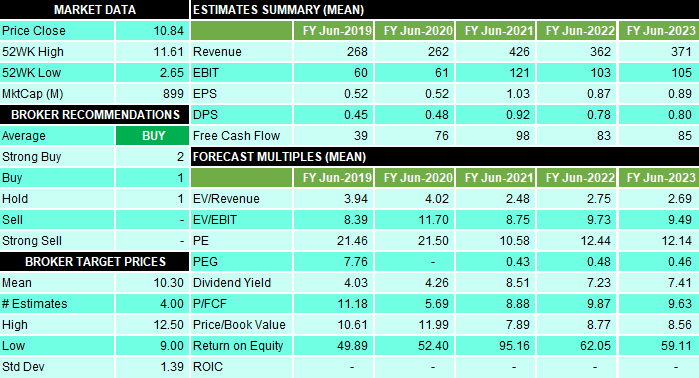

If the current momentum continues through the second half, and from the company's comments, we cannot see any reason why this shouldn’t be the case, NCK could earn $1.00-$1.05 per share for FY21. This puts the company on a price to earnings ratio of around 10.6, and a dividend yield (assuming the current 90% payout ratio) of around 8.5% fully franked.

Tuesday's profit upgrade follows a trading update in October which flagged better sales, and the company's full year 2019 results which also beat expectations. This implies that: 1. We are seeing a pandemic-induced bump in sales as consumers reallocate travel budgets to home refurbishment, and 2. Management's exemplary track record of executing NCK's superior business model continues despite the uncertainty created by the Coronavirus crisis.

Certainly, just looking at the fundamental numbers, the company remains a compelling investment case despite its recent post-upgrade price rise. It is neither expensive compared to its peers, nor compared to the broader ASX200 which has a PE ratio of around 20 and a dividend yield of approximately 4%. NCK has an outstanding track record of increasing its earnings and dividends over the last 5-years, and its return on equity is nothing short of extraordinary. Return on equity is a measure of management's ability to extract net profit from investors' capital. At over 50% on average for the last 3-years, NCK is the market leader on this metric.

The risks to the ongoing strong performance of NCK depend mainly on the sustainability of the recent upswing in consumer spending on home refurbishment and improvement. Without a doubt, NCK is unlikely to continue to double its profits each year. We are surely going to see an eventual moderation in the diversion of discretionary spending away from overseas travel towards spending on the home. However, given the continued dire Coronavirus situation in major North American, European, and Asian travel destinations, and despite the likely roll out of vaccines in 2021, we expect consumer spending on home refurbishment to remain at elevated levels into FY22 before normalising in FY23. This will likely be supported by a robust recovery in the Australian economy through FY21 and FY22 as interest rates remain near record lows, and as the Federal Government continues to provide stimulus.

We do see earnings growth moderating somewhat in FY22 and FY23, but expect earnings to remain at a significantly elevated levels compared to FY20. Despite the expected moderation in earnings growth, the investment case, based upon valuation (PE: FY22 12.4 & FY23 12.1), and yield (FY22 7.2% & FY23 7.4%) alone remains compelling.

We also note that out of the four major brokers that we have research recommendations for, two currently have a strong buy on NCK, one has a buy, and one a hold. There are no sells or strong sells. The average price target for the brokers is $10.30 with a high target of $12.50 and a low target of $9.00. We do expect however, that as more brokers return from holidays, they will likely raise their price targets for NCK.

Looking to the chart of NCK, it is in a clear short term and long term uptrend. The recent upswing has taken it above a clear consolidation zone between $7.66 and $9.96. This area should now act as an area of support, and therefore offers investors a potential zone to buy into any pullbacks.

We initially covered NCK as a potential buy on 23 July 2020, and reiterated a potential buy on 29 September 2020 and on 2 December 2020. Our current position is that investors should consider holding existing positions in NCK, or may wish to purchase on any potential pullbacks in the price to around $10. Our 12-month price target for NCK is $12.20.