A snapshot of overnight moves and a look to the upcoming Australasian session for 26 October.

Market Moves

Wrap

US markets edged higher again, but not enough to stave off a weekly decline for each of the three major US indices.

The week was heavily influenced lingering fears about the impact of the Coronavirus pandemic as rising case counts in both the US and Europe threatened to derail the fledgling recovery. Another key issue on investors mind, and certainly the case on Friday, is the likely timing and potential size of the next US fiscal stimulus package. There was little new information on either factor as the trading week ended.

For the session, the tech-heavy NASDAQ paced gains, it closed up 0.37%, while the benchmark S&P500 rose 0.34%, and the blue chip-laden Dow Jones Industrial Index lost 0.10%. Earlier, European stocks were far more upbeat, as the German DAX improved 0.82% and the French CAC popped 1.20%. In the UK, the FTSE100 ended the session 1.29% higher.

Metals prices on the LME were broadly weaker. Nickel was the worst performer with a 1.22% fall, but the rest were not far behind. Copper also saw a 0.56% loss in New York.

Iron Ore prices were sharply lower by 4% on Friday, and another 2.48% in early trading in the benchmark February 21 contract on the Chinese Dalian Exchange. To blame, a continued rise in Chinese port stocks, and stagnating blast furnace utilisation rates. Elsewhere, Brazilian mining company Vale SA said Friday that it is on track to reach its goal of producing 400 million tonnes of iron ore by the end of 2022 or early 2023, this is about 10% higher than its current production. Iron ore prices were 3.30% lower at US$113.07/t on the benchmark November contract in Singapore.

Precious metals were subdued. Spot Gold fell 0.23% to US$1900.80/oz, whilst Silver lost 0.49% to US$24.58/oz.

Energy commodities harder hit. West Texas Crude dipped 1.98% to US$39.85/barrel, Brent lost 1.60% to US$41.77/barrel, and Natural Gas was 1.63% lower.

In currency moves, the Australian Dollar improved 0.22% to 0.7135 as the US Dollar Index declined 0.20%.

Risk-off bonds bounced back after massive weekly losses, with the yields on the US 10 year Treasury Notes falling 2bp to 0.842%. This after starting the week at 0.746%

So, with few clear leads in terms of risk-on and risk-off assets overnight, where did the ASX200 Share Price Index end up? Well, it actually had a rather robust session, closing at 6179 compared to an overnight session high of 6184 and a low of 6139.

That's a 12 point premium to Friday's ASX 200 close of 6167, and predictive of approximately a 0.2% rise at the open for the S&P ASX200.

AU Companies

Coca Cola Amatil (CCL)

This morning the company reported that it had received a non-binding indicative proposal from Coca Cola European Partners to acquire all of its shares for a consideration of $12.75 per share.

This represents a premium of 23% compared to CCL's one-week volume weighted average. The company said that a formal recommendation from the Board based upon independend advice would be forthcoming.

Ex-Dividend Stocks

27 October, Clover Corporation (CLV) $0.025, 100% franked

29 October, Rectifier Technologies (RFT) $0.001, 100% franked

Broker Moves

| Australia And New Zealand Banking Group |

ANZ |

Zacks upgrades Australia And New Zealand Banking Group (ANZ) rating from hold to buy. Retains $21.00 price target. |

| BHP Group |

BHP |

Jefferies retains buy rating on BHP Group (BHP). Retains $45.00 price target. No change to rating or target after reviewing after September quarter production report, but lowers earnings estimates for FY21 by 1.5%. |

| CSL |

CSL |

Zacks downgrades CSL (CSL) rating from buy to hold. |

Macro Economy

It's a quiet day on the local economic data front, but later this evening we'll see data on New Home Sales in the US.

Below is a summary of the key macroeconomic data releases since our last update on Friday.

Australia

The preliminary, or 'flash', IHS Markit purchasing managers index (PMI) was 53.6 in October compared to 51.1 in September. Looking at the sub-indices, the flash Manufacturing PMI was 54.2 in October compared to 55.4 in September, and the flash Services PMI was 53.8 in October compared to 50.8 in September. Readings above 50.0 signal an improvement in business activity on the previous month while readings below 50.0 show deterioration.

Business activity growth accelerated at the start of the fourth quarter, led by the service sector. Business confidence was the strongest for over two years amid further expectations of market conditions returning to normal. However, the survey continued to indicate a surplus in operating capacity, which weighed on the labour market. Employment subsequently contracted. Meanwhile, input cost inflation accelerated sharply.

USA

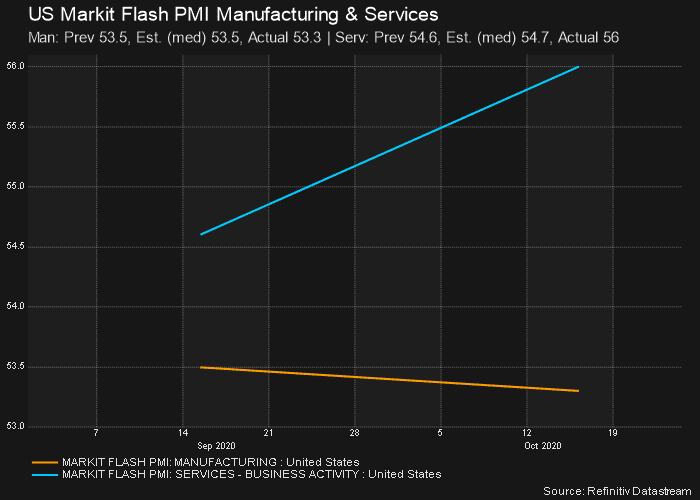

The flash IHS Markit purchasing managers index (PMI) for October is 55.5 versus 54.3 in September. Looking at the sub-indices, the flash Services PMI was 56.0 in October compared to 54.6 in September and better than the 54.7 the market was expecting, and the flash Manufacturing PMI was 53.5 in October compared to 53.2 in September but worse than the 53.5 the market was expecting.

Although the upturn in activity improved, the pace of new business growth eased slightly in October. Slower expansions in new orders were seen among manufacturers and service providers, with some firms stating that the ongoing impact of the coronavirus pandemic had weighed on demand.

Other companies noted that a number of clients were holding back on placing orders until after the upcoming presidential election. Nonetheless, the rise in new business remained solid overall and was the second-fastest since March 2019.

Back