A snapshot of overnight moves and a look to the upcoming Australasian session for 28 October.

Market Moves

Wrap

US markets were mixed as investors continued to grapple with the likely impact of a new wave of COVID-19 lockdowns in a number of countries, lingering uncertainty surrounding the impending US Presidential Election, and the size and timing of any potential US fiscal stimulus package.

The tech-heavy NASDAQ bucked the trend by logging a commendable 0.64% gain. In contrast, the benchmark S&P500 fell 0.30%, and the blue chip-laden Dow Jones Industrial Index lost 0.80%. Earlier, European stocks suffered another day of losses, as the German DAX dipped 0.93% and the French CAC fell 1.77%. In the UK, the FTSE100 also lost 1.09%.

Metals prices on the LME were generally higher though. Nickel lead the gainers with a 1.82% move, Copper, Lead, Tin, and Zinc each saw gains of less than 0.5%. Aluminium (-0.11%) and Steel Rebar (-0.34%) were the only losers. Copper saw a 0.16% loss in New York.

Iron Ore prices are 0.54% lower in early trading in the benchmark February 21 contract on the Chinese Dalian Exchange, but were 0.70% higher to US$113.37/t in the Singapore-based $US price.

Precious metals edged higher. Spot Gold rose 0.23% to US$1906.50/oz, whilst Silver gained 0.29% to US$24.30/oz.

Energy commodities were also higher. West Texas Crude added 0.85% to US$38.80/barrel, Brent gained 0.64% to US$40.72/barrel, and Natural Gas was 1.88% higher.

In currency moves, the Australian Dollar was just 0.03% lower to 0.7114 as the US Dollar Index advanced 0.02%.

Risk-off bonds were higher for a second session, with the yields on the US 10 year Treasury Notes falling 3.2bp to 0.775%.

So, with few clear leads in terms of risk-on and risk-off assets overnight, where did the ASX200 Share Price Index end up? Well, it had a lacklustre session, closing at 6020 compared to an overnight session high of 6072 and a low of 6011.

That's a 31 point discount to yesterday's ASX 200 close of 6051, and predictive of approximately a 0.3% fall at the open for the S&P ASX200. Note though, US futures are trading approximately 0.6% lower than their New York close, so we might see even sharper falls at 10am AEDT.

AU Companies

Afterpay (APT)

This morning the company reported its first quarter update. Underlying sales volumes increased by 115% to $4.1b compared to the previous corresponding period, and were 9% higher than the previous quarter. Active customers increased 98% (compared to the same period a year ago), and merchants were up 70%.

Afterpay noted that momentum towards the end of FY20 remained strong. But, despite the barrage of high double digit gains reported, the market might focus instead on anaemic 9% quarter on quarter growth in underlying sales, which conspicuously was the only quarter-to-quarter comparison disclosed in the update.

Ex-Dividend Stocks

29 October

Qualitas Real Estate Income (QRI) $0.008, 0% franked

Perpetual Credit Income T (PCI) $0.003, 0% franked

Gryphon Capital Income T (GCI) $0.007, 0% franked

Rectifier Technologies (RFT) $0.001, 100% franked

Broker Moves

| Australia and New Zealand Banking Group |

ANZ |

Jefferies lowers Australia and New Zealand Banking Group (ANZ) price target from $11.90 to $11.70. |

| Bendigo and Adelaide Bank |

BEN |

Jefferies raises Bendigo and Adelaide Bank (BEN) price target from $3.90 to $5.21. |

| Coca-Cola Amatil |

CCL |

JP Morgan downgrades Coca-Cola Amatil (CCL) rating from overweight to neutral. |

| Qantas Airways |

QAN |

Jefferies raises Qantas Airways (QAN) price target from $4.90 to $5.25. |

| Shopping Centres Australasia Property Group |

SCP |

Jefferies raises Shopping Centres Australasia Property Group (SCP) price target from $2.17 to $2.29. |

Macro Economy

Today, we'll see data on Australian consumer inflation with the release of the Consumer Price Index.

Below is a summary of the key macroeconomic data releases from the past 24 hours.

USA

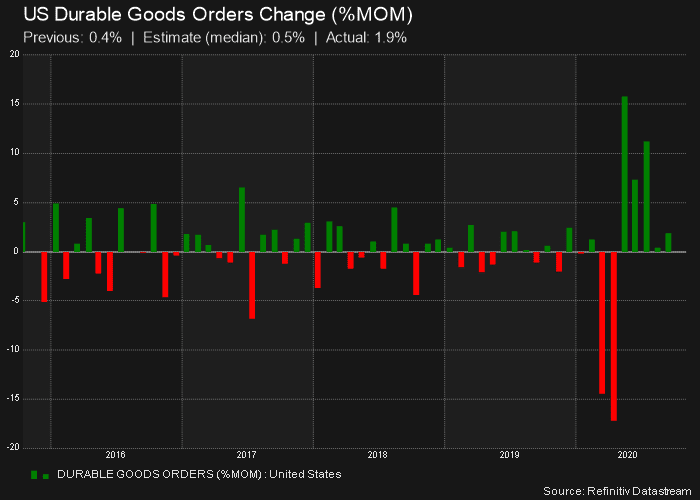

Orders for capital intensive goods that are expected to last greater than 3 years (durable goods) increased 1.9% in September compared August's 0.4% (revised up to 0.5%) gain. This was well ahead of expectations of an increase of just 0.5%.

The result was driven by a 4.1% improvement in orders for transportation equipment, which rebounded from a 0.9% decline in August. Orders for motor vehicles and parts was another big gainer, increasing 1.5% compared to August's 4.1% decline. Not surprisingly though, orders for civilian aircraft remained at zero for the third straight month

Core durable goods, that is, excluding transportation-related goods increased by 0.8% compared to 0.6% the prior month, and ahead of expectations for a 0.3% increase. Excluding defence related goods, orders increased by 1% which was better than expectations for a 0.5% increase.

That data shows that the US economy likely closed out the third quarter on a strong footing.

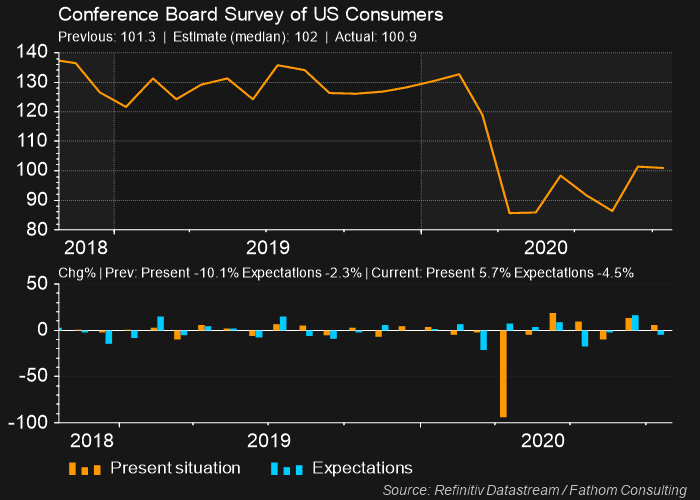

The Conference Board reported that US consumer confidence declined slightly in October. The Consumer Confidence Index dipped to 100.9 in October from 101.3 in September. This was below expectations for a reading of 102.

The Present Situation Index, which is based on consumers' assessment of current business and employment markets, increased to 104.6 from 98.9 in September. However, the Expectations Index, which is based on consumers' short-term outlook, decreased to 98.4 from 102.9 in September.

Back