As UK returns to the fray for the first time in 2022, risk remains firmly on the table with the dollar also bid as investors look forward to potentially three rate hikes from the Fed this year. With stocks and dollar both higher, there hasn’t been much demand for gold or indeed the Japanese yen, with the latter falling to its lowest level since 2017 against the buck. Crude oil prices shrugged off the strength of the dollar, rising ahead of the conclusion of the OPEC+ meeting, where producers are expected to stick to the current policy of easing the cuts by 400K barrels per day in February.

OPEC+ expected to stick to planned February output increase

Crude oil, which has already recovered around 10% from its mid-December lows, may find further support in the short-term as concerns over demand eases. The OPEC+ is highly likely to increase output by 400K barrels per day over February. Anything else will come as a shock. It remains to be seen how much further will oil prices be able to recover in the weeks and months ahead. As the OPEC+ continues to ease supply curbs, the market will become increasingly less tight. There’s always the danger of China introducing fresh curbs given their zero covid policy.

Relief that Omicron not as deadly biggest driver for stocks, risk assets

The biggest driver behind the stock market rally and risk appetite in general is relief that Omicron is not as deadly as Delta, which is fuelling expectations that travel restrictions and lockdowns will be lifted soon. Omicron’s rapid spread means cases will likely peak very soon in Europe and given that it doesn’t cause too many people severe illnesses to require hospitalisation, it is boosting the prospects of herd immunity.

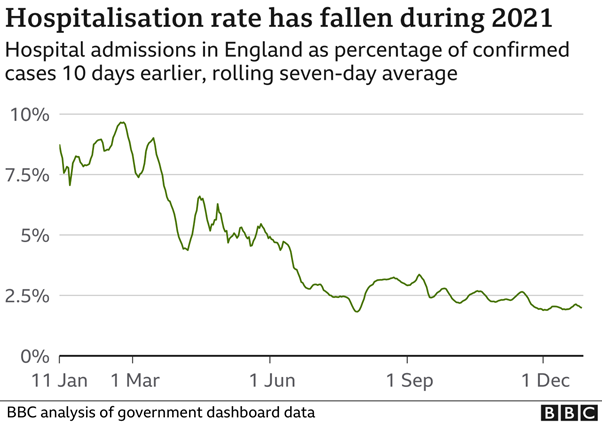

Falling hospitalisation rates in England in the face of surging Covid cases is a reflection of large immunity that has been built up, either because of vaccination or infection. There are also better treatments available for Covid for those who become severely ill. This suggests that other major developed economies will also be able to weather the storm, with the US reporting 1 million cases alone on Monday.

Value stocks could outperform growth

If infections peak soon, then the disruptions to economic activity from this current wave of the virus could be short-lived. That’s the hope anyway. Unless some new variants emerge, there might be light at the end of the tunnel. If the situation improves in the coming weeks while vaccination efforts continue around the world, then risk sentiment should remain positive.

We could see European equities rise further, with stocks in the hospitality and tourism sectors, as well as banks, doing particularly well. Indeed, Germany has removed the UK from its classification as an area of variants of concern, which means fully vaccinated UK travellers won’t need to self-isolate or provide a negative test result upon arrival in Germany. The FTSE has broken out:

Source: ThinkMarkets and TradingView.com

Source: ThinkMarkets and TradingView.com

One particular area of the stock market that could struggle is growth stocks, which carry low dividend yields and are very expensive relative to earnings. The tech-heavy Nasdaq hasn’t hit a new record high yet, despite the S&P and Dow rising to fresh unchartered territories:

Source: ThinkMarkets and TradingView.com

Source: ThinkMarkets and TradingView.com

With the Fed and other central banks likely to tighten their policies this year, we could see the sector struggle in the months ahead.

Q1 outlook

For a more detailed analysis and outlook for the first quarter, please click

HERE.