The stock markets have started the new week little changed after Friday’s session was ended on the front-foot in what a was very choppy week. The positive session on Friday helped to keep the safe-haven dollar under pressure and support the major currency pairs, as investors continued to play the ongoing “reflation trade.” Copper has rallied to a fresh 2021, in yet another risk-on sign. Cryptos, which tumbled last week, have rebounded sharply at the start of Monday’s session with Bitcoin up nearly 8% at just shy of $52900. Gold and silver, which lost their shine towards the end of the week, were flat. Crude oil has dropped however as virus cases in India hit 1 million in just three day, with investors worried that demand from one of the world’s largest consumers will be hurt as a result.

When in doubt, buy risk is what the market finally decided on last week after indecisive price action had dominated earlier in the week. Stronger data and faster Covid vaccinations continued to keep sentiment positive after the markets were tested a few times with bearish catalysts, including news of Biden’s capital gains tax proposals and the upsurge in virus cases in India and a few other places.

In the week ahead we have policy meetings from the Bank of Japan and more significantly the Fed Reserve, as well as lots of data and earnings all to look forward to. Could the Fed finally put an end to the dollar’s bearish trend this month with a surprisingly hawkish policy meeting? Time will tell. In addition to macro events, the week ahead is filled with plenty of company earnings from major household names, including most of the big tech giants such as Apple and Amazon. It is going to be a very busy week indeed.

Fed to follow footsteps of BOC?

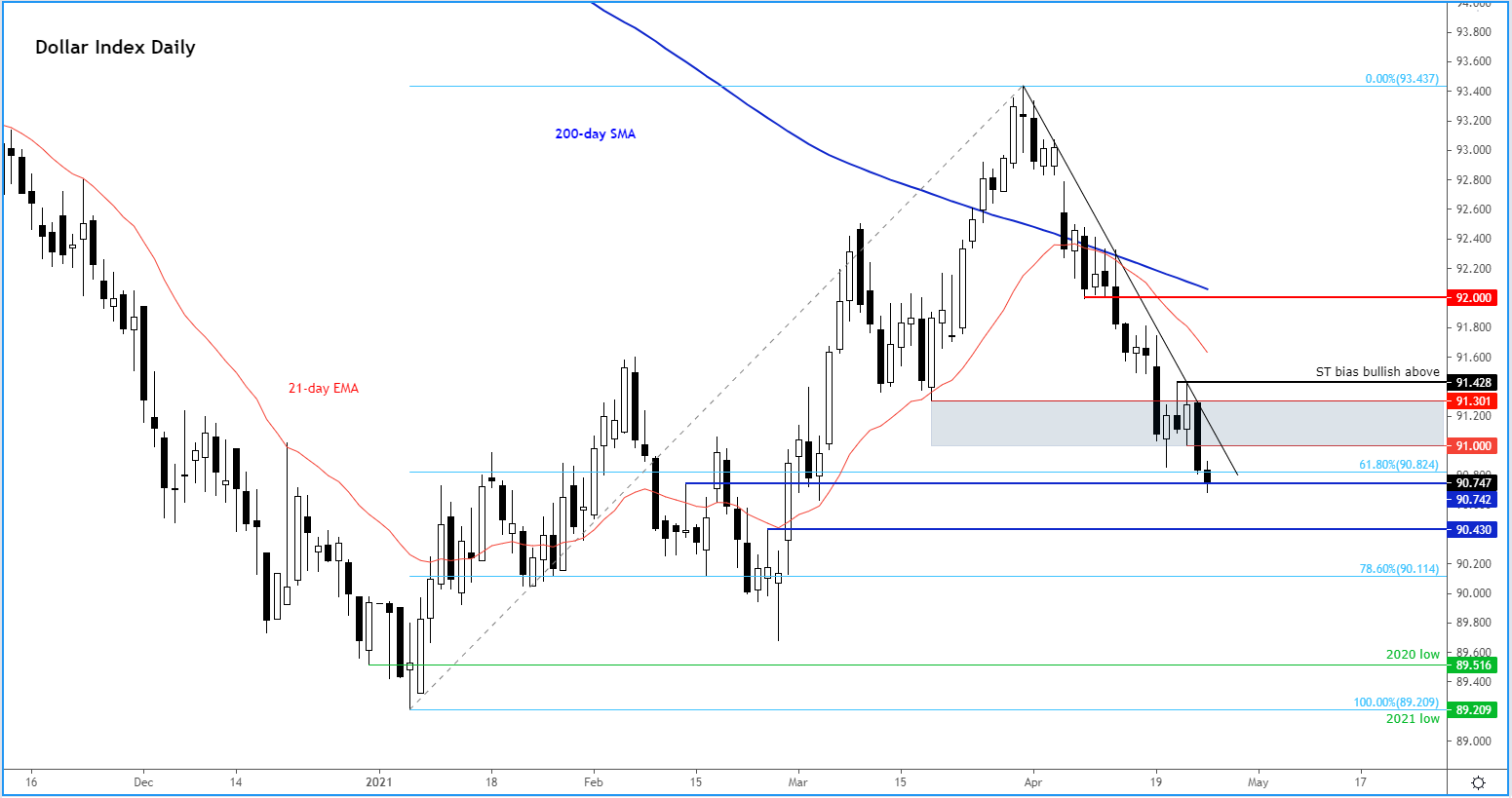

Investors will be looking forward to the FOMC policy meeting on Wednesday. Jay Powell and his colleagues are widely expected to leave monetary policy unchanged and re-affirm that there will be no shift in stance until “substantial further progress” on the recovery is made. At the FOMC’s March meeting, the dot plots suggested that the start-point for lift-off in interest rates would be in 2024. Although there won’t be any updates to the dot plots at this meeting, investors will be wondering whether the Fed will deliver a surprise like the BOC did last week and suggest a quicker policy tightening. If that’s the case, then it will most likely underpin the dollar after the greenback’s weak start to Q2 despite mostly positive news from the world’s largest economy. The US economy is in a much better position compared to a few months ago, thanks to government stimulus and the fast pace of Covid vaccinations. So far, the strength of US data hasn’t prevented the Fed from keeping the QE taps wide open. But if the improvement in data persists then it will only be a matter of time before the Fed tapers its emergency stimulus measures. Against this backdrop, the dollar could be on the verge of a comeback soon, especially against currencies where the central bank is more dovish. Watch out for a potential rebound in US bond yields, too. This could keep gold under pressure.

Source: ThinkMarkets and TradingView.com

With employment improving and inflation likely to rise well above the 2% target and stay there for a while, the Fed could start tapering asset purchases before the end of the year and then start hiking rates before 2024, possibly in in the first half of 2023.

FAAMG and other tech stocks face key risks

The so-called FAAMG group of US technology stocks (Facebook, Apple, Amazon, Microsoft, and Google), which represent a quarter of the S&P 500’s market capitalization, will be reporting their results in the next few days. Their quarterly numbers and outlooks will have significant impact on the S&P 500 and obviously the tech-heavy Nasdaq indices. The tech sector was among the biggest beneficiaries of the lockdown but as Netflix and Intel reminded us last week, past performance is not necessarily a good indicator for the future.

Working from home may soon become a thing of the past for many employees and other pandemic-driven consumer preferences are going to evolve. This might have major implications, especially for the technology sector. For example, companies with subscription-based services might struggle to win new customers the same way they did during lockdown when people stayed at home mostly and purchased services online. Taking Netflix as an example, its subscriber growth slowed far faster than anticipated in Q1 and was the smallest first quarter gain in four years. Its shares slumped, even though it reported better-than-expected top and bottom lines. So, it is going to become increasingly difficult for these types of companies that excelled last year to keep up pace. Investors will be focusing on what company execs will be highlighting about the changing behaviour of consumers in their quarterly reports and earnings calls, than just merely concentrating on the top and bottom lines.

Another big risk facing US companies is tougher regulations and higher taxes for the richest Americans. President Joe Biden and the Democratically-controlled Congress will be keen to regulate tech giants, with regulators continuing to pursue anti-trust actions against the likes of Apple and Alphabet. Meanwhile Biden’s proposal of nearly doubling levies on capital gains for people earning more than $1m could provide a massive blow to the equity markets, if it ultimately passes in a form similar to the initial proposal. It could discourage the richest Americans who are likely to own shares from allocating money towards long-term investments. They might sell shares before the tax increase becomes low, potentially derailing the stock market rally.

Meanwhile, as global lockdown measures are slowly likely to ease, things will hopefully return to more normal ways in the coming months. The US economy is likely to rebound strongly, and inflation will probably heat up as a result, requiring tighter monetary policy as a result. If the Fed were to start tapering bond purchases later in the year, this will likely put upward pressure on bond yields. Rising yields are seen as negative for the growth stocks, whose dividend yields are comparatively lower than what you would get from fixed income.

So, the technology sector may not perform as spectacularly as it did last year and there is a risk even, we could see a reversal in shares of tech giants as investors worry about rising borrowing costs, tougher regulations, higher taxes and lower earnings potential in the coming quarters.

Macroeconomic and earnings highlights

Monday

South African Markets in Focus

By Kearabilwe Nonyana

This week of trade was one of the choppier weeks in recent memory. The markets continue to lack direction as market participants continue to digest these elevated levels global risk assets are priced. In a slue of mining operational updates across the industrial mineral complex we have seen incredible production numbers from the miners in the country and seeing commodity prices at record highs you can surely start to deduce the incredible revenue performances these companies will have and with great cost containment that will result in incredible earnings in quarters going forward. Retailers’ results show of a resilient consumer through tough times as inflation numbers have ticked up into the SARB target band of 3%-6% inflation came in at 3.2% as administered price start affecting the consumer it will be good to see if this has any sizable impact on the inflation retailers can pass on to consumers before it starts affecting demand. The local JSE TOP 40 took a breather to give back some of the gains of the past few weeks to see it come of almost 5% from the record levels set a week and a half ago.

The week ahead

There is very little on our local economic calendar; on the 29/04/2021 the Stats SA will release PPI data to indicate how much price increase’s manufacturers are experiencing. This will be an indication if we will see an increase in inflation for consumers in later quarters. On the global markets side the rumours of tax increases in the US should not be a surprise to markets as all the fiscal stimuli would have to be paid for in future years ; what will be important for markets is to understand the details in these proposed capital gains tax increases. This will affect our local markets as this could be an indication that future taxes may be levied by our government on corporates as well as individuals further exacerbating the pressures felt by the economy. On Wednesday the 28

th of April, the FOMC meeting will conclude, and the US interest rates will be determined. I do not anticipate any changes in tone from the Fed Chairman or changes in policy stance. As the Fed chair speaks of transitory inflation and their willingness to look over short term inflation in order to protect the economy, I believe this will continue.

Stock pick of the week: Sibanye-Stillwater

PGM metals Palladium is back in the fore. As Automotive demand remains strong and the increased focus in CO 2 emissions in Europe and in China has caused a surge in the price of palladium which is used as an auto catalyst in diesel cars as a way of reducing CO 2 emissions. Even though Nornickel the biggest producer of Palladium is bringing back two suspended operations that were suspended in February the fundamentals of the metal remain sold with a great demand for the metal which bodes well for SSW. One Of the other elements which is important is the metals mix in SSW business you are exposed to gold as an inflation hedge and a metal with high operating leverage and the relatively low P/E ratio at 6.5 and a forward P/E of 4.57% bodes well for SSW as a stock to look out for.

Corporate Action

Corporate Action