Download Carl's Bear Market Survival Guide e-Book:

https://www.thinkmarkets.com/au/lp/2023-bear-market-survival-guide-ebook/

Download Carl's Bear Market Survival Guide e-Book:

https://www.thinkmarkets.com/au/lp/2023-bear-market-survival-guide-ebook/

Local Macro

As expected, the local economy was dominated by South Africa’s hosting of the BRICs summit in Sandton in the penultimate week of August. The organisers of the BRICs summit tried hard to keep the interest going but president Xi Jinping of China showed relative disinterest in the event by missing a couple of speeches that he was due to deliver and of course Russian president Vladimir Putin decided not to attend in person in case the South African authorities arrested him on behalf of the International Criminal Court.

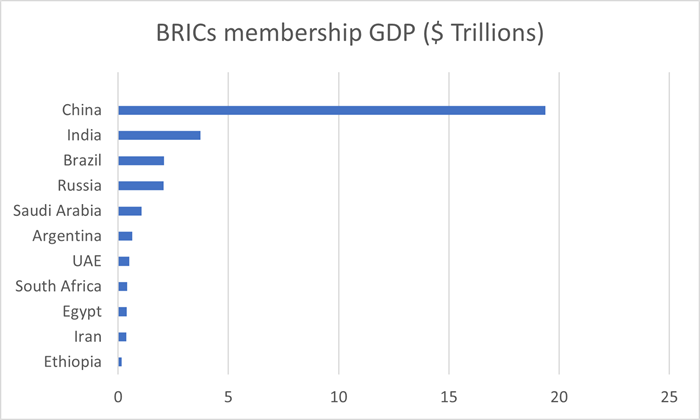

The rhetoric was predictably anti-western, replete with references to US hegemony and the like but desperately short on anything that remotely resembled actionable plans for the organisation. The highlight of the event was the announcement that six new members would be admitted to the bloc from January 1, 2024, being Argentina, Egypt, Ethiopia, Iran, Saudi Arabia and the UAE.

Click to enlarge chart

Click to enlarge chart

In some ways, BRICs is similar to the Non-Aligned Movement (NAM) and its offshoot the New International Economic Order (NIEO). Both BRICs and the NAM purport to reflect the aspirations of the developing world and the NIEO and BRICs would love to see the end of the Bretton Woods financial system that has been in place since the end of World War 2.

The NAM began life as a genuine attempt by formerly downtrodden and colonized countries to shake off the yoke of paternalistic aid and philanthropy and replace it with meaningful trade. But it quickly became hijacked by Soviet surrogates such as Cuba, which refused to denounce the USSR for invading Afghanistan in 1979, thus losing major credibility.

But at least most of the NAM members were relatively poor and sought support from whatever quarter it was offered.

Not so with BRICs. This grouping didn’t come about via its members wanting it to happen. It was catalyzed by Jim O’Neill, Global Head of Research at Goldman Sachs, who in November 2001 penned a research note entitled “Building Better Global Economic BRICs”. Without O’Neill coining the acronym BRIC, it is doubtful that the grouping would ever have materialised.

O’Neill’s findings can be summarised as follows:

- In 2001 and 2002, real GDP growth in large emerging market economies will exceed that of the G7.

- At end-2000, GDP in US$ on a PPP basis in Brazil, Russia, India and China (BRIC) was about 23.3% of world GDP. On a current GDP basis, BRIC share of world GDP is 8%.

- Using current GDP, China’s GDP is bigger than that of Italy.

- Over the next 10 years, the weight of the BRICs and especially China in world GDP will grow, raising important issues about the global economic impact of fiscal and monetary policy in the BRICs.

- In line with these prospects, world policymaking forums should be re-organised, and in particular, the G7 should be adjusted to incorporate BRIC representatives.

So far, so good and pretty much everything that O’Neill predicted has come to pass, with the notable exception of the adjustment of the G7; that remains staunchly a developed-world body. This has stuck in the craw of China particularly, which sees itself as a world leader and moreover, one which eschews the whole concept of a rules-based global order. The G7 has never formally invited China to join the organisation, nor is it likely to do so in the foreseeable future. China gets irritated by remarks from the G7 condemning China’s treatment of the Uighers in Xingjiang province and the crackdowns on democracy in Hong Kong. However, China is a member of the much broader grouping G20.

It is unclear exactly what BRICs is. It is much easier to determine what it is not. For example, it is not a trading bloc such as the European Free Trade Association (EFTA) or Gulf Cooperation Council (GCC) or southern Common Market (Mercosur). All of the BRICs countries, including those in the expanded list, trade with China, but few if any trade with each other. And while there should, logically, be ample space in which to trade with each other, this has never been a critical feature of membership since inception. Once again, it all comes down to the raison d’etre for BRICs existence.

Is it an organisation representing the poor and downtrodden masses in the developing world? Certainly not, with China and Russia especially and now with Saudi Arabia and Iran included. Any resemblance to the NAM has now become extremely blurred.

Is it still seen as an attractive investment grouping? Well, like the curate’s egg, it’s good in parts. However, China’s economic growth rate has fallen back markedly in recent times due to several factors that were not so apparent in 2001. Firstly, as a direct consequence of its former one-child policy, China is now reaping the whirlwind of a demographic “time-bomb”. It is estimated that the Chinese population may halve between now and 2050. The movement of people from the rural to the urban areas over many decades was the main engine for growth in the China economy up util about a decade ago. But with a declining population, that has fizzled out now.

Secondly, the country has been unable to transition away from being the world’s manufacturer to being more of a consumption-based economy. Its HCE/GDP ratio of around 40% is extremely low by world standards and despite great efforts in the field of monetary policy to stimulate consumer demand, Chinese consumers are not biting. The reason is easy to understand; China’s social welfare system isn’t wonderful, and the average Chinese person must make provision for his or her retirement at the expense of current consumption. The recent relaxation of birth control, which now allows families to have up to three children is too little too late. Chinese families have become more westernised over the years and as they have urbanised, they see less of a need for large families.

Thirdly, debt in the Chinese system, at a government, municipal and especially at a real estate level, has become unsustainable. Opinions vary, but a recent Reuters estimate put China’s total debt/GDP at 250%, not quite as high as Japan but certainly uncomfortable. Goldman Sachs estimates total government debt, including municipal debt and shadow banking debt at $23 trillion. Beijing maintains its stance that this is still manageable, but it no longer has the capacity to trade it way out of the situation as it did in the wake of the Global Financial Crisis. Indeed, the very large infrastructure boom of the last decade in China was primarily responsible for amassing such a huge debt pile. In many ways, there is an eery similarity between China today and Japan of the 1980s. The “Japanification” of the Chinese economy appears to be well underway.

And then lastly, partly due to efforts to reduce debt but more to do with lack of demand for its products in the west, China is now suffering deflation, both at a PPI and CPI level. This is affecting consumer demand and GDP growth is forecast to fall to around only 3.5% this year. Thus, China desperately needs the west to come back buying its goods with a vengeance. But that is unlikely to happen, as many countries in the have restructured their supply chains to become less reliant on China in future.

Russia has largely become un-investable since its illegal invasion of Ukraine. EU and other economic sanctions are strangling the Russian economy, which is further being crippled by the huge cost of maintaining the war in Ukraine. Interest rates were recently hiked by 3.5 percentage point by the Russian Central Bank in a vain attempt to halt the rapid depreciation of the rouble but this will further dampen consumer and other demand in the Russian economy. Traditionally, most wars tend to boost economic activity, at least in the short term. But Russia has never been able to convert its military-industrial intellectual property into tangible civilian areas. Thus, over time, even the short-term benefits of a war economy will dissipate. Sanctions will exacerbate that decline.

Even stripping out the impact of the current geopolitical problems that Russia has created for itself, Russian GDP growth has been in a secular downtrend since 2001.

Of all the big players in BRICs, India has managed to not only keep its head above water and largely avoid economic catastrophes but has tended to flourish since the BRIC acronym was coined. GDP growth since the inception of BRIC has been impressive, touching 10% on a number of occasions.

Unlike China, India has never been burdened with a one-child policy, nor has its economy had to rely on exports for growth. Its economy is driven by consumer demand and agriculture and is at a far earlier stage of development than China. It is also nearly self-sufficient in food production, unlike China, which imports most of its food. Agriculture is very important to India, with around 60% of the Indian population being employed in the agricultural sector and agriculture contributing almost 20% of GDP.

However, it is ridden with bureaucracy and getting anything done in India can take ages. But this will change over time, as India gradually assumed the position on most populous nation on earth.

Of the four substantial and original components of BRICs, Brazil has been a relative laggard in terms of growth. According to the World Bank, "structural bottlenecks resulted in a meagre average GDP growth (0.6%) over the past decade, despite favourable demographics. Productivity growth remains weak, due to a complex tax system, a cumbersome business environment that discourages entrepreneurship, slow and unequal human capital accumulation, ineffective State intervention policies (at the sectoral level), low savings, and compressed public investment to accommodate higher current spending and increasing pension obligations".

President Luiz Inacio Lula da Silva is at last managing to extract some good news out of the Brazilian economy, since experiencing something of a baptism of fire in his third term after beating incumbent Jair Bolsonaro last year. He has managed to strike a balance between keeping the poorest of the poor relatively happy without necessarily alienating the powerful business community. Growth in the first quarter of the year was a relatively modest 1.9% but is forecast to be 2.5% in the second quarter. Fitch recently upgraded Brazil’s credit rating to BB from BB, recognizing the government’s many reforms.

And then there’s South Africa. An incongruous inclusion at best, it’s been a member of BRICs since 2010. Compared with the other four original members, it’s almost inconsequential. In terms of economic growth, one must go back to the pre-democracy era of the 1960s to find any decent, sustainable growth. The country has flirted with recession in recent years and lost its investment grade rating just before the Sars-CoV-2 pandemic, since when it has dropped further into sub-investment grade. It has the dubious distinction of having the highest persistent rate of unemployment in the world and seems unable to fix its creaking electricity system that suffers daily cuts, referred to as “loadshedding”. Infrastructure spend as a proportion of GDP has collapsed to near-maintenance only levels and the government appears to have no idea how to remedy this.

National elections will be held next year, and it is widely anticipated the governing African National Congress (ANC) will lose its overall majority, resulting in a potential hung parliament.

South Africa’s foreign policy appears to have no discernible direction, other than wanting to run with the hares and hunt with the hounds. But its ability to appease the concerns of the US especially is wearing very thin, with regular allegations of collaboration with the Russians on sensitive areas such as arms and ammunition. It would indeed be a great pity if South Africa lost access to US markets in terms of the African Growth & Opportunity Act (AGOA). Its trade with the other countries of BRICs would in no way make up for the loss of trade if South Africa was no longer part of AGOA.

Long-time BBC journalist Andrew Harding encapsulated the mood of South Africans well in a farewell note after living in Johannesburg for 15 years; "This is a nation lulled by a sense of its own exceptionalism. Its history of overcoming impossible odds".

So what do the new members of BRICs bring to the party? Not much. Let’s start with Argentina, a jaded old second-world economy that’s had more than its fair share of political and economic upheavals in the past few decades. But in the early 1950s, Argentina was at the forefront of scientific research into nuclear fusion with its short-lived Huemul project.

The economy today is struggling with hyperinflation, but Argentines are used to this state of affairs and have for many years been avid hoarders of physical US dollars in an attempt to immortalize their savings. And successive governments have been addicted to debt but are not so happy to repay it to the IMF and other bodies when required to do so. Membership of BRICs may therefore be seen as a way of tapping China and the BRICs Development Bank (effectively the same thing) for more debt.

But an interesting new political event happened very recently in Argentina-the very strong showing in early primary polling for the presidential election by extreme right-wing parties. The surprise front-runner in the race to replace incumbent president Alberto Fernandez is a populist by the name of Javier Milei. Milei scored 30% of the vote in the first primary held on Sunday 20 August. Second place, not far behind on 28% was another extreme right-winger called Patricia Bullrich. Combined, the two far-right parties polled 58%. On Friday 25 August, as BRICs announced Argentina’s membership of the organisation, Milei was having a virtual meeting with the IMF, describing how he intended to restructure the Argentine economy if he becomes president. One of the things he intends doing is dollarizing Argentina-i.e., replacing the peso with the US dollar as the country’s official currency. Such a move is hardly likely to go down well with China within the BRICs framework.

But a lot can happen between now and October 22 when the final runoff for the presidency takes place.

Egypt and Ethiopia are unsurprising additions to BRICs, especially Ethiopia, which is an avowed Chinese surrogate in the Horn of Africa. China has poured lots of infrastructure-related funds into Ethiopia over many years and although it is still one of the world’s poorest countries, the incidence of extreme poverty has been reduced considerably. Egypt was a strong supporter of the old NAM and its leader at the time, Gamal Abdel Nasser, was one of the founding fathers of the organisation in the 1950s.

Then there are the three oil giants of Iran, Saudi Arabia, and the UAE. Iran and Saudi Arabia have been bitter enemies pretty much ever since the Shi’ite theocracy came to power in Iran. Both countries vie for supremacy in the middle east, even though Saudi Arabia is a significantly larger economy than Iran. But recently there has been a thaw in the relations between the two but it is unknown how long this fragile peace will last.

Saudi Arabia still fears an attack from Iran or one of its surrogates such as the Houthi insurgents in Yemen. The US has shown a large degree of indifference towards Saudi Arabia and its security ever since it became far less dependent on Saudi oil. Nevertheless, negotiations are taking place between the US, Saudi and Israel, the goal being to get America to provide further security for Saudi while at the same time Israel would make meaningful concessions to the Palestinians.

It will be interesting to observe if China can manage to keep the peace between Iran and Saudi once they are both members of BRICs. Iran is labouring under US and EU sanctions, so it is understandable why it would hate the west. Saudi Arabia, on the other hand, has good relations with the west and is probably keen to preserve those.

Ultimately, BRICs is a political grouping and moreover one which actively seeks to usurp the long-established power of the US and the western world. I wish them the very best of luck in keeping the internal peace in the organisation, especially once it expands its membership base. They’ll need it.

South African consumer price inflation (CPI) fell back to 4.7% in July, its lowest point in two years. It’s now approaching the mid-point of the SA Reserve Bank’s target range and gives the SARB’s Monetary Policy Committee ammunition to thinking about further pausing rate hikes or even cutting. Much depends on the sustainability of this downwards trajectory in inflation.

Global Macro

In the US, the annual junket of central bankers took place in Jackson Hole, Wyoming. US Federal Reserve chairman Jerome Powell hedged his bets by stating that while he acknowledged that the Fed’s current position with interest rates was restrictive, there was unlikely to be any relief on rates until he was satisfied that inflation was firmly on a downwards trajectory.

European Central Bank (ECB) president Christine Lagarde gave a similar outlook for Euro area rates.

The UK’s services flash PMI dipped below 50 and the manufacturing PMI remains well below 50, suggesting that the UK economy is struggling somewhat. Wage inflation is significantly higher than CPI. Consumers are really starting to feel the pinch as short-term fixed rate mortgages start re-setting at multiples of previous levels. So, for example, mortgages taken out at 2% during the Covid -19pandemic are now re-setting at nearer 8%, a four-fold increase.

Friday sees the release of the US nonfarm payroll data for August, and this will be watched closely for further signs of strength in the jobs market.

Feature Stock - Spur Corporation (SUR)

Spur Corporation is one of the oldest consumer brands in South Africa, with a genesis that goes back to the early 1960s. And although it has differentiated its product offering over the years, Spur Steak Ranches remains by far the biggest single component of the business, providing 52% of the number of restaurants and almost 70%% of the turnover of the South African operations.

For the year to 30 June 2023, revenue rose by 27.4%, pre-tax profit rose by 51.9% and attributable profit rose by 72.2%. Headline earnings per share rose by 81.1% to 258.86c. A final dividend of 110c/share was declared, giving192c/share for the year a 51.1% increase on the previous year.

Spur has not only survived the Covid-19 pandemic but is now flourishing. It is reaping the benefit, along with other fast food/casual dining brands, of consumers’ desire to eat out more or to buy takeaway food, due to high levels of loadshedding.

Spur recently acquired Doppio Zero, a predominantly Gauteng-based casual dining chao=in and intends rolling the concept out nationwide. The RocoMama brand has been highly successful up until last year when earnings were relatively static. Spur intends remedying this with smaller RocoMamas outlets in different parts of the country.

At the current share price of 2776c, Spur is on an historic PE ratio of 10.6% which is not expensive. The dividend yield of 6.9% is very attractive.

Click to enlarge chart

Click to enlarge chart

The Spur Corporation chart shows the price is in a well-established short-term uptrend (light green ribbon) and a well-established long-term uptrend (dark green ribbon). The price action is higher peaks and higher troughs. The candles until 21 August are predominantly demand-side in nature (i.e., white bodies and/or downward pointing shadows). In combination, these technical factors demonstrate substantial excess demand for Spur Corporation shares.

The point of supply set on 22 August at 3000 is the key pressure point moving forward. The price is compressing in a consolidation below this level. The longer the price continues to trade near 3000, the greater the probability it can break through and set new highs in this short term uptrend. Stops are best set below the 14 August point of demand of 2501.

Analysts view: I am comfortable adding risk to Spur Corporation around the current price and remaining in a long position while the price continues to trade above the short-term trend ribbon.

Learn More, Earn More!

Want your portfolio questions answered? Register for next week's Live Market Analysis sessions and attend live! You can ask me about any stock, index, commodity, forex pair, or cryptocurrency you're interested in.

REGISTER:

Live Market Analysis Webinars - Thursdays 1pm AEST / Thursdays 3am UTC, Friday 1.30pm AEST / Friday 3.30am UTC

You can catch the replay of the last episode of Live Market Analysis here:

THE BULL IS BACK (if this stuff happens)!