Download Carl's Bear Market Survival Guide e-Book:

https://www.thinkmarkets.com/au/lp/2023-bear-market-survival-guide-ebook/

It appears the US banking crisis of 2023 is about to claim another victim. Shares in PacWest (NYSE: PACW) are trading around 50% lower in after-hours trading as company insiders confirmed the bank was assessing its options for a potential recapitalization or sale.

Download Carl's Bear Market Survival Guide e-Book:

https://www.thinkmarkets.com/au/lp/2023-bear-market-survival-guide-ebook/

It appears the US banking crisis of 2023 is about to claim another victim. Shares in PacWest (NYSE: PACW) are trading around 50% lower in after-hours trading as company insiders confirmed the bank was assessing its options for a potential recapitalization or sale.

If PacWest does go under, it will join a growing list of casualties in the current crisis which started in March following the collapse of Silicon Valley Bank. First Republic was added to the scrap heap last week as it was forcibly sold to JP Morgan, the same occurred with Credit Suisse and UBS showing effects are being felt outside of the US, and Signature bank also lost its battle for survival in March.

So far, regulators have backstopped depositors by insuring their savings – even in excess of previously mandated limits. Apart from the obvious loss in capital by investors who owned stock in the affected companies, there are likely to be serious and ongoing ramifications of recent collapses at a time when the US economy is facing great strain from high inflation and rising interest rates.

The US regional and community banking system performs an important role in the distribution of credit to small and medium enterprises (SMEs) within the US economy. Credit is the lifeblood of any modern economy. Businesses borrow to invest in increasing their productivity. Businesses make profits which are distributed to stakeholders, used to pay taxes, and most importantly, to pay wages to workers who then go out and spend at other businesses. Economists predict the problems in the regional banking system could lead to a sharp contraction in the flow of credit to SMEs.

If credit suddenly tightens in the US economy, recent Federal Reserve interest rate increases could not have come at a worse time and threaten to tip the US economy into recession.

How did we get here?

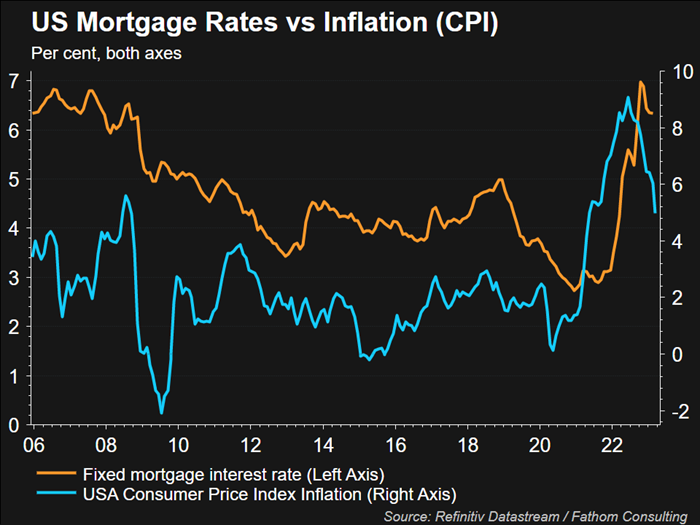

Much of the problem within the US banking sector stemmed from the inability of smaller banks to manage the sharp increase in official interest rates over the last 15 months. Banking 101 suggests you take depositors' funds and use these as collateral to create loans, and to invest any surplus in safe assets which offer reliable yields such as government backed notes and bonds. The spread between the interest rate you pay on deposits, versus what you earn on loans and investments is your profit. Banks have been doing this for hundreds of years and will likely be doing it for hundreds more!

There's nothing unusual about this model, or really even inherently risky – nearly all the time! The pandemic, and the shockwaves it sent through economies and financial markets afterwards, created a perfect storm of risk for many banks. It turns out, one of the key pillars of the model, that is invest in safe assets with reliable yields, didn't work this time…and

bankers and regulators didn't see it coming.

To assist economies to repair after the devastating fallout of the pandemic, central banks all around the world slashed interest rates to zero, and for some, even into negative territory. Messaging from central banks, including the Federal Reserve, was rates would stay low for a prolonged period of time. There was indeed a window of 12-18 months where banks were buying those safe government-backed securities at yields next to zero with a view that yields would hang around there for quite some time.

But there was a catch. Well, a couple of catches, really. Firstly, one must remember the inverse relationship between bond prices and bond yields. That is, when bond yields are very low as they were after the pandemic, bond prices were correspondingly very high. This isn't necessarily a bad thing if you intend to hold your bonds to maturity. Bond maturities are typically 1, 2, 5, 10 and 30-years, give or take, depending on which country you're investing it (bills are shorter term, notes medium term, and bonds longer term, but let's just stick with "bonds" as a generic term for all fixed interest for now!).

Bond prices depend on the prevailing interest rate versus the rate attached to the bond. If prevailing rates go up (or are expected to go up) then your fixed rate bond doesn’t look so attractive anymore. The market is going to mark down the price of your bond to compensate for its lower yield relative to those new bonds coming on the market which offer higher yields.

If you hold a bond to maturity, it generally doesn't matter what price you purchased it at. Interest rates can rise and fall as much as they like, you'll collect the yield you were happy with when you originally purchased the bond, and you'll get your money back at the end. Bonds which are held to maturity are a no-fuss, no risk, no surprises investment. Unless you're a bank.

If you're a bank, and those bonds were purchased using depositors' money, then you might have to buy those bonds back before maturity if depositors withdraw their money. It's a bad look if your ATM spits out a piece of paper saying "Sorry, we invested your money in a bond and we can't give it back because we want to hold the bond until maturity."

If you buy a bond back before maturity and rates haven’t moved since you bought it, no problems, the price of the bond will be roughly the same. Sell the bond, give the depositor their money back. If rates have changed, particularly if rates have risen, you are likely to have to sell your bond at a loss in order to raise the cash to repay your depositors.

And here in lies the problem…rates haven't remained the same since many regional banks gorged themselves on "safe" government bonds just after the pandemic.

Rates have gone up, and gone up big time.

Central banks who initially feared a sharp and protracted global recession (depression?) soon realized the supply chain chaos COVID-19 created quickly caused a massive spike in the price of…well, absolutely everything! Suddenly there were too many cashed up consumers with too few goods and services to buy. The oldest rule of economics is Demand > Supply = Price ⬆

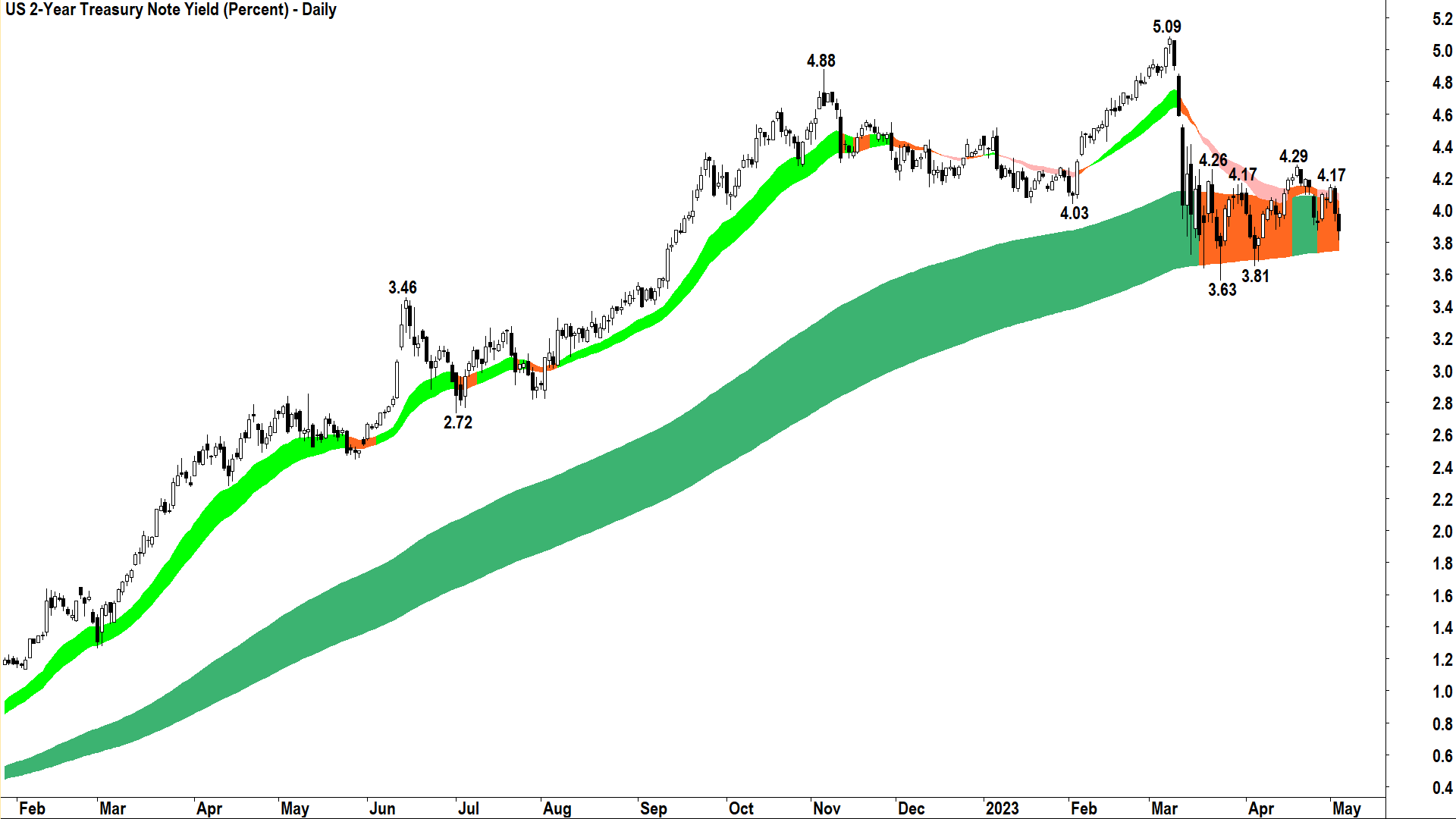

And boy did prices go ⬆! Double digit inflation rates were experienced pretty much all over the world. Central banks get more than a little cranky at even the slightest mention of the "I" word. Their main (very blunt) tool to fight inflation is higher interest rates. Up those rates went all over the world. In the US, with the Fed's latest 0.25% hike this week, a total of 5% in a little over a year.

Bond yields soared in response to the higher yields on offer, and you guessed it, bond prices tumbled. More than tumbled, they crashed. You thought 2022 was bad for your stock portfolio? Bond investors had it far worse! 2022 will go down in history as the worst year for bonds ever – and by a long shot.

Banking becomes broken

This brings us back to our unsuspecting US regional banks. Around the end of 2022, as the cost of living soared and home mortgage rates topped 7%, average Americans started to draw down on their savings – which had previously reached record levels following government stimulus in the wake of the pandemic. Silicon Valley Bank (SVB), the first domino to fall, experienced a 13% decline in deposits in the first couple of months of this year.

click on image to enlarge

click on image to enlarge

On 8 March, they reported they would take a US$1.8 billion charge as a result of being forced to sell some of their bond investments to cover withdrawals from depositors. It proposed a US$2.25 billion capital raise to cover any capital shortfalls and reduce reliance on further forced asset sales. Ratings agency Moody's promptly downgraded the company.

The next day, social media lit up with the possibility of a liquidity crunch at SVB and at least one influential venture capitalist publicly warned his peers to immediately withdraw their cash from the beleaguered bank. What followed was a good old-fashioned bank run. More deposits flew out the door, more beaten down bonds would have to be sold to cover them, and even greater losses were about to hit the SVB bottom line.

In the space of just a few weeks, but then culminating in a period of just a few hours, the very model banking is based upon unraveled. SVB shares were halted from trading on 10 March, never to return. The rest is, as they say,

history.

This week, the Federal reserve decided to ignore the developing crisis in the US regional banking sector by adding another increase to the rate spike which caused the crisis in the first place. If there is a silver lining, it is this last rate hike didn't drive bond yields any higher. In fact, it had the opposite effect.

Bond yields actually fell after the announcement of yesterday's 0.25% interest rate hike.

This is because markets are forward-looking. Yes, official interest rates at the Fed went up this week, but market rates fell. It shows the market is betting this last increase could well be the straw which breaks the camel's back. In this analogy the straw is yet another impost on consumers' and businesses' bottom lines, and the camel is the teetering US economy!

Assume the brace position?

Over the last few days, I have been monitoring the charts of the NASDAQ Regional Banking Index (KRX) and its constituents very closely. I am growing increasingly concerned these are

more closely resembling the charts of many financial stocks in 2008 during the great credit crunch which triggered the Global Financial Crisis.

click on image to enlarge

click on image to enlarge

Investors should be aware of the similarities and may wish to adjust their risks accordingly. Increasing cash levels is an obvious first step (ironically, potentially increasing deposits at the banks!). Alternatively, investors could consider adding some risk to defensive assets such as gold and bonds. Yields look set to fall further as fears of an impending recession grow – remember, lower bond yields equal higher bond prices – good if you already own bonds.

click on image to enlarge

click on image to enlarge

Gold looks particularly interesting here. As it does not have a yield, rather it usually costs fund managers to store and insure it, gold becomes more attractive as an investment in a low interest rate environment. Add in its long historical reputation as a hedge against market uncertainty, and we may well be entering a period where gold can really, um, shine!

click on image to enlarge

click on image to enlarge

Going forward I suggest investors remain alert, but not alarmed. Central banks and government regulators are aware of everything I've discussed here – it's not like I've told a bunch of secrets. Any sensible person would (should?) assume these learned scholars of finance and commerce will leverage the hard lessons they learned during the GFC, and as a result, already have the situation well in hand. Right?

But if for some reason they don't, to be forewarned is to be forearmed. I just warned you some bad stuff might still happen before this #BankingCrisis has run its course!

Learn More, Earn More!

Want your portfolio questions answered? Register for next week's Live Market Analysis sessions and attend live! You can ask me about any stock, index, commodity, forex pair, or cryptocurrency you're interested in.

REGISTER:

Live Market Analysis Webinars - Thursdays 1pm AEST / Wednesdays 3am GMT, Friday 12pm AEST / Thursdays 2am GMT

You can catch the replay of the last episode of Live Market Analysis here:

Buy Gold, sell Oil, and watch out for the banking crisis!