Source: ThinkMarkets and TradingView.com

Source: ThinkMarkets and TradingView.com

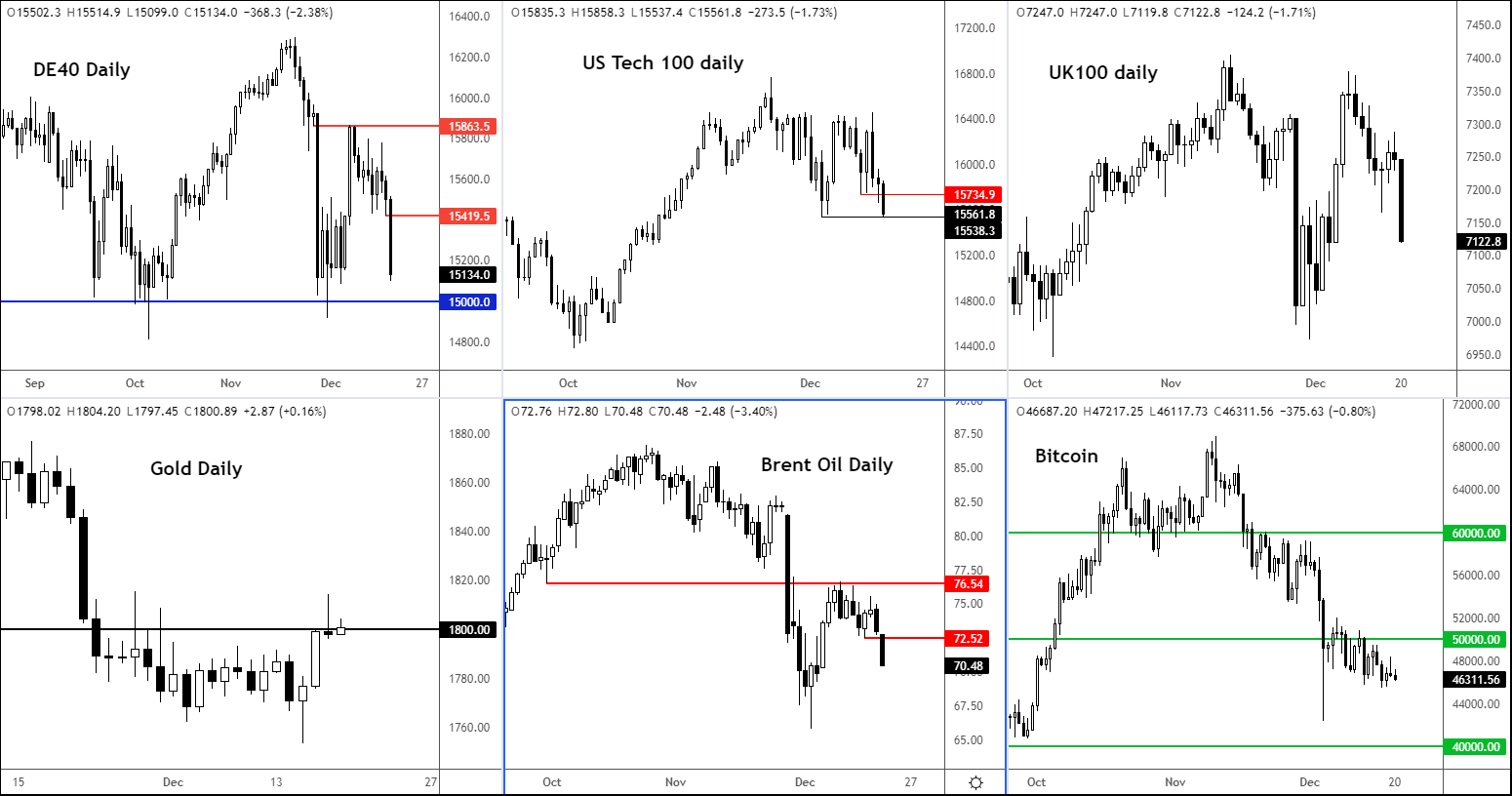

Stocks and crude oil sold off first thing Monday as the markets started the final week before Christmas with a whimper. Understandably, airlines were leading the declines, with ICAG shares falling 5% right from the off. Europe’s leading indices were down over 2%, while crude oil prices fell about 4%.

Risk appetite was non-existent this morning as investors reacted to the worsening coronavirus situation over the weekend. Further measures to curb its spread were announced by some of Europe’s largest economies – most banning UK visitors, where Omicron is spreading like wildfire. It is a critical week insofar as Christmas plans and New Year’s holidays are concerned, but already feeling the strain is the hospitality industry after the latest restrictions resulted in a wave of Christmas cancellations. As a growing list of countries accelerate vaccination and booster campaigns, the potential for more restrictions and lockdowns is there with the UK likely to up its efforts, after virus cases hit repeated highs. Also adding to the negative sentiment is concerns over US President Biden’s roughly $2 trillion economic package, which got rejected by Senator Joe Manchin.

Keep an eye on tech stocks

The week ahead is going to be rather quiet from a macro point of view, with only a handful of scheduled events to look forward to. Traders’ plans to slowly unwind ahead of the festive period have well and truly been ruined. The question of how tighter monetary policy will play out on overvalued technology stocks will be a major talking point in the weeks to come, but right now it is all about coronavirus as omicron continues to spread like wildfires. The latest measures to curb the infection rate is likely to hurt the economic activity a little, which should keep the pressure on all sorts of risk assets, including crude oil and commodity dollars. So, volatility is likely to remain elevated this week despite a quieter macro calendar. The markets will close on Friday for US and German investors in observance of Christmas eve.

As mentioned, the focus will also remain on technology stocks. The Nasdaq surrendered its entire gains made in the aftermath of the FOMC policy decision on Wednesday, and some, amid concerns that policy tightening from the Fed will reduce the appeal of lower-yielding growth stocks, especially those with overstretched valuations. Sentiment hasn’t been helped in the sector by insider selling of late.

Central banks ready to tighten

Meanwhile, all the major central banks have now decided on monetary policy – some 20 of them last week alone. Most of these central banks either tightened their respective policies in terms of interest rates or QE or announced their intensions to do so in the coming months. The Bank of England surprised with a 25 basis point rate hike when 10 was expected, leading to a rally for the pound. The Federal Reserve said its ultra-easy policy since the beginning of the pandemic is drawing to a close as it accelerated the reduction of its monthly bond purchases by $30 billion a month. The Fed’s QE will end in March and the FOMC’s projections indicate there will be three rate increases. Meanwhile, the European Central Bank announced it too is slowing bond purchases and end its pandemic emergency programme by March, although this will only be a cautious taper as it will simultaneously boost purchases under the old Asset Purchases Programme. By October, it plans to bring down net purchases to €20bn a month by October 2022.

Here’s what is on the agenda in the week ahead:

Source: ThinkMarkets and ForexFactory

Source: ThinkMarkets and ForexFactory

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

Learn and earn more today.

Visit our Education Centre