Gold was up 1% at the time of writing as it rose for the second consecutive day after halting its selling last week. The metal was supported by falling bond yields and a mostly weaker US dollar, as investors looked forward to the publication of the ISM services PMI later on and FOMC meeting minutes on Wednesday. Overall, sentiment towards all risk assets, including gold and silver, remained positive as major central bank have repeatedly dismissed talks of withdrawing QE or raising rates prematurely. The ongoing supply of cheap central bank money is therefore continuing to provide support, with investors happy to buy the dip in precious metals after their recent weakness.

In June, gold had sold off sharply in response to the Fed’s hawkish policy decision, which erased the entire gains it had made during May. But it has since managed to stabilise and has impressively risen despite the stronger US jobs report on Friday. The positive reaction suggests gold investors are relieved that wages didn’t rise more than expected, giving the Fed more time to keep its current policy stance intact. Meanwhile other major central banks have also made it clear that higher rates of inflation will not last long given that prices have been boosted as a result of supply chain disruptions and other temporary factors.

As I mentioned in our

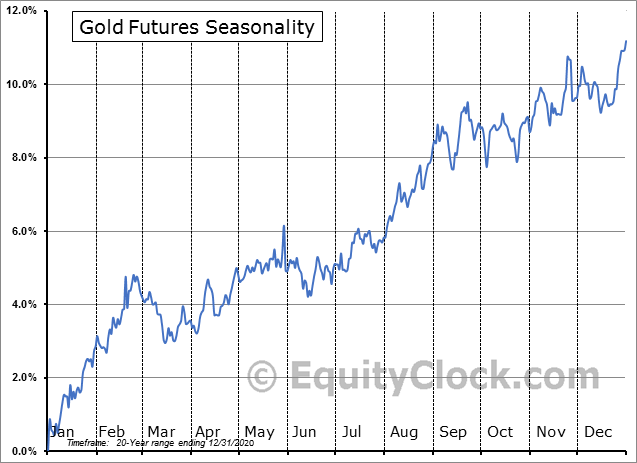

quarterly outlook guide, the gold market should have expected the Fed to turn hawkish, like the equity markets. Another reason why I am still keen on precious metals is this: gold was on the rise before the pandemic, when central bank policy was nowhere near this loose. The metal had hit a high of $1703 in early 2020, before initially selling off and then rebounding sharply with every other risk asset as central banks and governments unleashed record stimulus measures. Now back at around $1810 (when this report was written), gold was only around $110 more expensive than just before lockdowns started. Is it not reasonable to expect that with vast stimulus measures still in place that gold should be much higher? Of course, you could argue that gold has already gone considerably higher before topping out last August as yields bounced back, so it has done what it should have. Still, the fact that all other major assets classes are holding onto much of their stimulus-driven gains, gold looks massively undervalued in that regard. Gold bulls would also point to seasonality factors, with the yellow precious metal historically doing well during the third quarter.

Source: EquityClock.com

Meanwhile in so far as the very short-term is concerned, investors are looking forward to find out what the Fed discussed in greater detail when the minutes from the FOMC’s last policy meeting are released Wednesday. Today, investors were awaiting the publication of the ISM services PMI, due for publication at 15:00 BST. The PMI was expected to moderate to 63.4 from 64.0, but the devil will be in the details – specifically the employment and prices paid components. If these components are not too inflationary, then the greenback could fall across the board, potentially leading to further gains for gold later on.

With gold breaking through the upper resistance of the short-term consolidation around $1790-$1797, the path of least resistance is now back to the upside. Potential dips back this area will likely be supported on the first retest.

Source: ThinkMarkets and TradingView.com

At the time of writing, gold was testing the next area of trouble around the $1810 area, formerly support. If resistance holds here, then a re-test of the above-mentioned broken resistance at $1790-97 would become likely. But ideally, what the bulls would like to see is a clean break above here. In this potential scenario, gold would then pave the way for a possible move towards $1850, which is where the 61.8% Fibonacci level converges with prior support/resistance.