Stocks end week on the front-foot as S&P 500 eyes breakout. But will this prove to be a bull trap, given the technical "death crossover" signal, as well as macro concerns such as Ukraine-Russia conflict, soaring inflation and Fed tightening?

Stock markets recovered from a weaker start to the new week, with major indices trimming their losses by mid-morning London session on Monday. Crude oil rose nearly 4%, aluminium added 1.7% while gold was up only modestly. The focus continues to remain on the situation between Ukraine and Russia.

On that front, no agreements have been reached yet in negotiations with Ukraine, while there needs to be significant progress made first before a possible meeting between Putin and Zelensky, according to Kremlin. Last week, hopes over a possible deal had lifted sentiment in the market. Russia’s negotiator on Friday, for example, said that the two sides were now 'halfway there' on the issue of Ukraine's demilitarization, and that on the issues where their views are most-closely aligned is Ukraine's neutral status and not joining NATO. Let’s see if the gap closes in the days ahead, but it doesn’t look promising.

Stocks end week on the front-foot

If you look at the financial markets over the past week or so, it is as if the Ukraine war never happened, or the Fed was not very hawkish. Stock markets roared back higher to close solidly in the black last week. This was the second consecutive weekly positive close for European indices, but the first one for Wall Street and Asia Pacific (APAC) markets. STOXX Europe 600 erased all the losses it had suffered since the invasion of Ukraine began. Risk-sensitive commodity dollars surged higher, while safe-haven Japanese yen and gold slumped. Yen pairs had a wonderful week. Cryptocurrencies traded mostly higher. Crude oil bounced sharply off the lows but still ended lower for the second consecutive week. But that rebound has continued into the new week with Brent reaching $111 and WTI $108 per barrel. Oil prices must be watched closely given ongoing concerns over soaring inflation, as any further sustained pressure will intensify those concerns and potentially have repercussions elsewhere in the financial markets.

Watch FedSpeak

As well as the ongoing situation in Ukraine, the focus in the week ahead will also be on Fedspeak, with Powell speaking on both Monday and Wednesday. The Fed has signalled a much stronger appetite to combat inflation, indicating a further 6 rate increases in 2022. Judging by comments from some of the Fed officials that have spoken, there is a possibility that we may even see a 50 basis point increase in May. Let’s see if there is much appetite for that, and what plans they might have for running down the central bank’s $8.9 trillion balance sheet.

In terms of macro data, the highlights include durable goods orders and housing market data. From the UK, we have CPI and retail sales, while in Switzerland, the SNB will be making a “decision” on interest rates. Hint: no rate increases are coming. Another set of key data will be the latest PMI numbers, due on Wednesday from Eurozone.

Economic data highlights

Monday 21 March

Tuesday 22 March

- Central bank speech: ECB’s Lagarde, FOMC’ Williams, SNB’s Jordan and MPC’s Cunliffe

Wednesday 23 March

- UK spring statement and Consumer Price Index (CPI) for February

- Central bank speech: BoE’s Bailey, FOMC’s Powell and Bullard

Thursday 24 March

- SNB rate decision

- Flash PMIs from France, Germany and UK

- US durable goods orders, jobless claims and flash PMIs

Friday 25 March

- UK retail sales

- German Ifo

S&P 500 breakout vs. death cross

A lot was made of the S&P’s so-called “death-cross,” but we haven’t seen much downside action. The “death cross” on the S&P describes the fact the 50-day has fallen beneath the 200-day moving average. This usually happens as a result of a correction or sell-off, which makes it a bit of a lagging indicator. Nonetheless, it provides an objective signal, telling traders that the market is no longer in an uptrend. As such, some traders and fund managers would be less inclined or unwilling to look for long trades in such a market. Others might even use this signal to look for short trades. So, it has some important implications. But by the time the moving average crossover happens, the bulk of the price move may have already taken place, as has been the case now. The bears need to see the S&P remain or go back inside its bearish channel again, otherwise the bulls will remain in charge.

Source: ThinkMarkets and TradingView.com

The South Africa Market in Focus

By Kearabilwe Nonyana

We sit in unprecedented times, and it looks like there will be no reprieve for financial market participants. Headwinds in the global markets keep on stacking up even though risk assets remain near all-time highs; even with the sell off the market still sits in bull market territory with the Benchmark ALSI sitting above the psychological level of 70000 points. The federal reserve kept to it’s timeline hiking the fed fund rate by a quarter of a percentage point. The market was anticipating this but the pace of rate hikes in future periods has elevated which is a changing dynamic in global markets. Increased risk to the inflation outlook continues to rise and there’s is no way to curb the inflation trajectory apart from resolutions to the global geopolitical tensions in Ukraine. Oil continues to trade above the $100 dollars a barrel level. JSE All Share index looks to close the week of flat and will continues to be driven by global macro-economic factors.

The Week Ahead

21/03/2022

On Monday South Africa celebrates Human Rights Day and the local bourse will be closed.

23/02/2022

Headline CPI Data

Our CPI data will be released on Wednesday the 23

rd of March 2022 inflation has been trending upwards in the last quarter with the first reprieve in the previous month inflation. Inflation was close to the upper end of the target band of 3-6% but never breached that number. The inflationary numbers are primarily driven by supply side disruptions in the energy market as well as increases in administered prices. Inflation expectations are still not anchored around the mid-point of the target band and future expectations of headline inflation are being revised to the upside bring in to question the pace at which the SARB will want to raise rates. One risk factor that is quiet concerning for me is the implied increase in wheat which will increase the rate at which the food price inflation affects the index and will lead to socio economic factors which might hamper growth in the country in later periods. What is being anticipated locally is that interest rates will increase at the next MPC meeting what is being considered is the quantum of the rate increase and FRA’s are considering a rate hike in excess of 50 basis points which is implying an increase in the pace.

South African FX

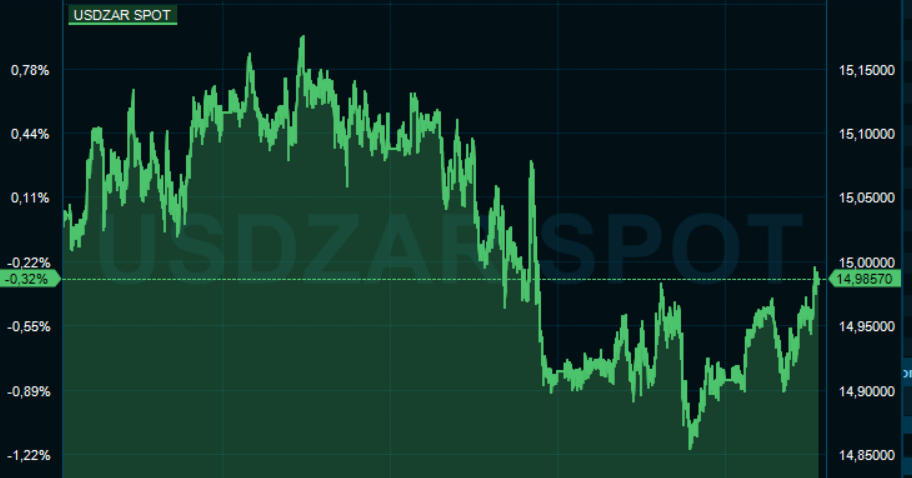

Our local unit continues to remain very strong with the risk aversion at its highest and risk to the upside with rising Covid cases in Asia, Geopolitical tensions , Fed interest rate hikes and upward revisions to inflation the rand remains quite robust and has not been spurned as the proxy for risk assets for it to remain as robust speaks to strength in our terms of trade(The difference between our import prices and export prices) and the value still to be extracted in our capital markets. In the first quarter there has been a net foreign inflow on to our local bourse as trading volumes on our local exchange improves.

USD/ZAR Spot

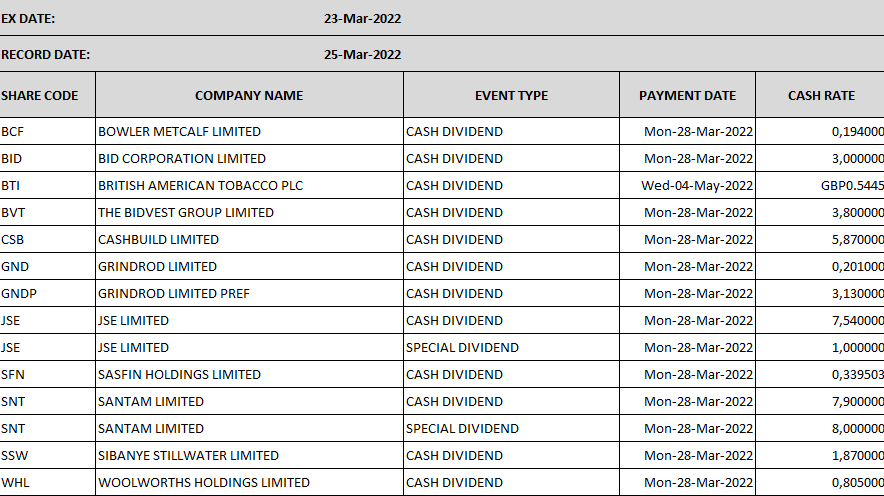

Corporate actions

Corporate actions

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.

Learn and earn more today.

Visit our Education Centre