Market Sentiment

“On a long enough time horizon, the survival rate for everyone drops to zero”-Chuck Palahniuk, Fight Club 1996

The S&P 500 (SPX500) keeps on hitting new highs, shrugging off weak or indifferent US economic data.

The price of Bitcoin continues to surge since the start of the year. there appears to be no end in sight for this bullish run.

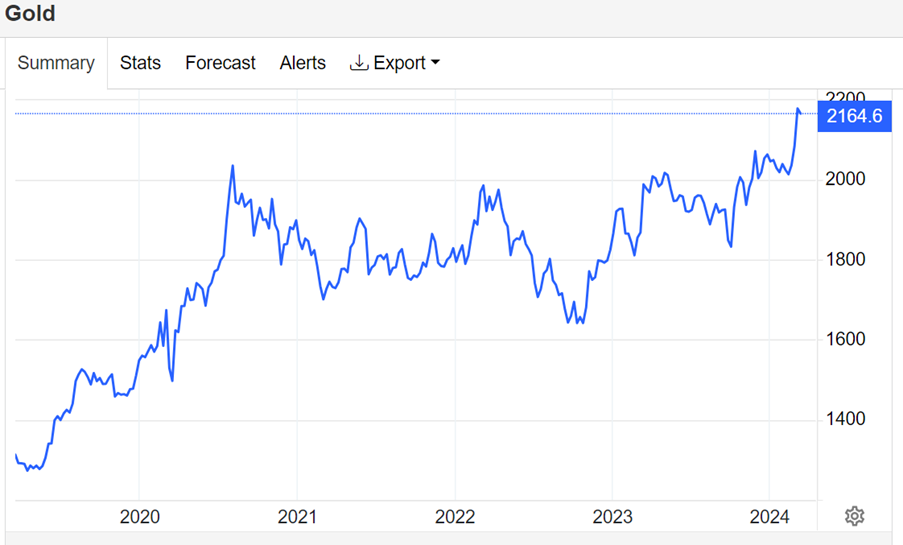

Gold has also been moving upwards recently but came back off its highs in response to the recent US CPI reading. Gold prices eased to $2 150/oz, down from highs of $2 190/oz. The move followed a bounce in US Treasury yields after the US CPI report, which showed another sticky inflation reading.

The reading is likely to add pressure to the US Federal Reserve (The Fed) to offer a more hawkish tone than seen at Fed chairman Jerome Powell’s hearing earlier this month and the dovish focus of the December meeting.

Local Macro

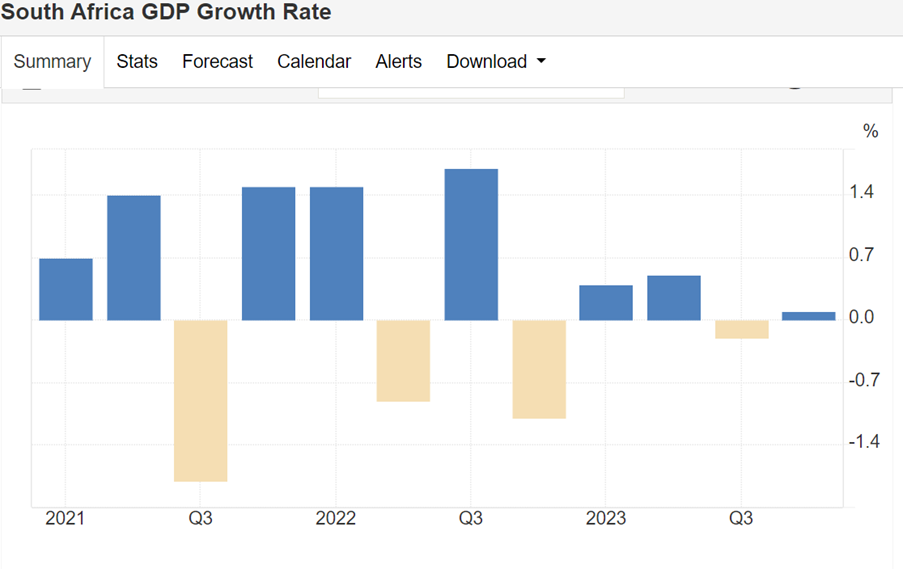

SA GDP growth slowed to just 0.6% in calendar 2023 from 1.9% in 2022. Unlike the UK, which appears to have slipped into recession in the final quarter of last year, SA just managed to avoid the same fate. Fourth quarter GDP growth in SA was 0.1% compared with the previous quarter, which shrank by 0.2%.

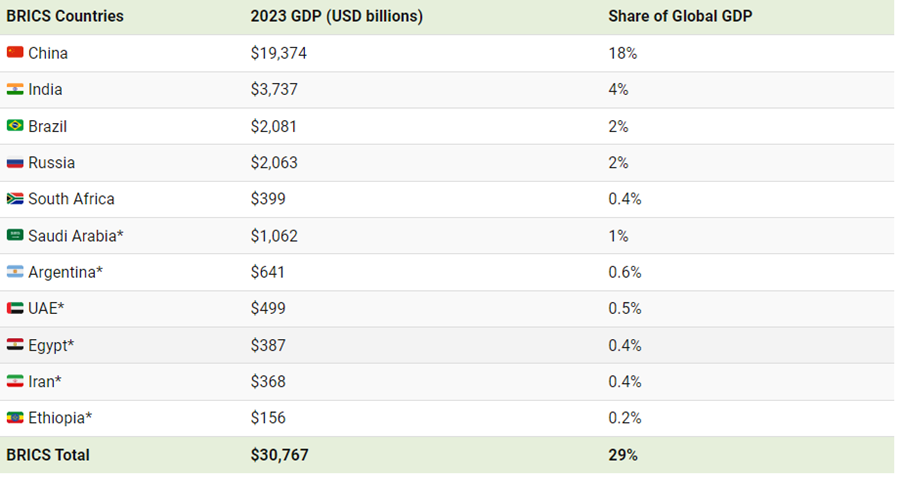

Although positive, this is still anaemic growth and is nowhere near where SA needs to be, especially if it is ever to make any meaningful inroads into its pernicious unemployment situation. Relative to the other members of the enlarged BRICs grouping, SA is one of the smallest economies, ranking alongside Egypt and Iran.

Global Macro

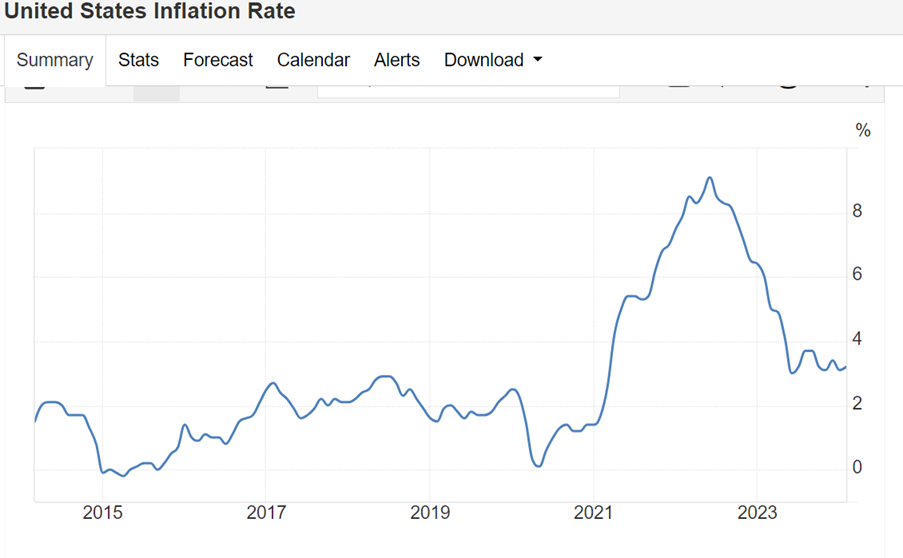

US inflation slightly exceeded expectations in February, although it remains well-contained, albeit still above the desired 2%. The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.4 percent in February on a seasonally adjusted basis, after rising 0.3 percent in January.

Over the last 12 months, the All Items index increased by 3.2 percent before seasonal adjustment.

According to the Federal Reserve Bank of New York, US household debt reached $17.5 trillion in the fourth quarter of 2023 and delinquency rates rose. Total household debt rose by $212 billion to reach $17.5 trillion in the fourth quarter of 2023, according to the latest Quarterly Report on Household Debt and Credit.

Credit card balances increased by $50 billion to $1.13 trillion over the quarter, while mortgage balances rose by $112 billion to $12.25 trillion. Auto loan balances rose by $12 billion to $1.61 trillion, continuing an upward trajectory seen since 2011. Delinquency transition rates increased for all debt types except for student loans.

This is a potentially worrying statistic for the US Federal Reserve (The Fed), as it contemplates its next move with respect to interest rates in America. The US consumer has always appeared highly resilient, but with credit card debt rising so rapidly, accompanied by an uptick in delinquencies, the US consumer may be feeling stress.

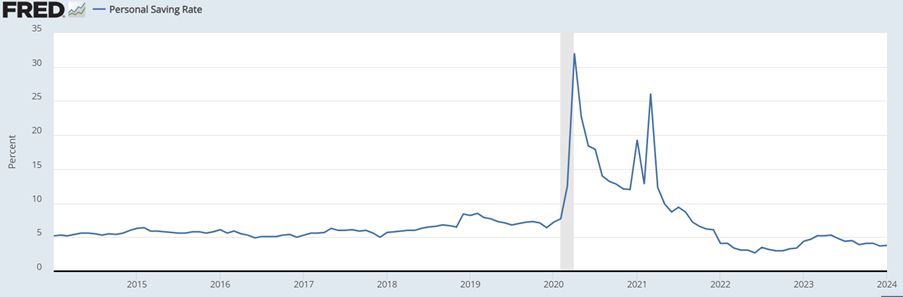

Additionally, the US personal savings rate is at an historical low of 3.8% of GDP, a far cry from the heady days of 2020/21 during the Covid pandemic, when savings rates soared to record levels. So, US consumers appear to have not only exhausted their savings but are now increasingly using their credit cards to make ends meet.

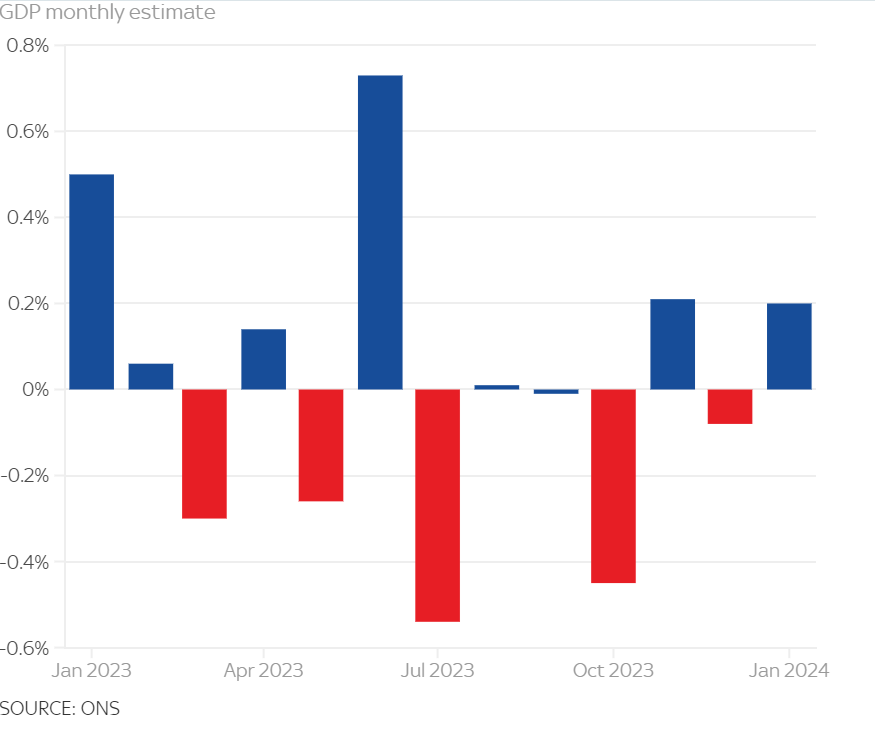

In the UK, January’s GDP number was released on 13 March and indicated a turnaround from the technical recession that occurred in the last two quarters of 2023. According to the Office for National Statistics (ONS), UK GDP rose by 0.2% quarter on quarter in January. If this trend carries through until February, this will likely result in 2023’s technical recession being one of the shortest in Britain’s history.

In the 2024 UK Spring Budget, the British Chancellor of the Exchequer set out the government’s plans for taxing, borrowing and spending. Easing the tax burden was central to the decision-making, but with the UK in recession, it was a difficult task.

Income tax

With the cost-of-living crisis continuing to be top of mind, the possibility of tax cuts was subject to intense speculation in the media. However, the current macroeconomic environment leaves limited room to manoeuvre. In the end, the government opted for a less costly 2 pence cut in National Insurance rates, which should save the average employee around £450 per year. This is in addition to an identical cut announced in the Autumn Statement (which took effect in January).

The move was designed to boost the numbers of people in work and simplify the “double taxation” on income (i.e. National Insurance and income tax), with the Chancellor pledging further National Insurance cuts in the future. However, personal tax thresholds remained frozen, resulting in a higher tax take overall thanks to the effects of fiscal drag.

Real estate

The main surprise was a cut in capital gains tax on residential property, from 28% to 24%. The rationale is that a lower tax rate should drive more property transactions.

Tax relief on furnished holiday lets was abolished, with the aim of freeing up more homes for long-term rental. Stamp duty relief on sales of multiple dwellings was also abolished, as a further revenue raising device.

Non-Dom taxation

The government also announced an overhaul of the tax rules for non-domiciles (Non-Doms) i.e. people living in the UK whose home for tax purposes is overseas.

From April 2025, new arrivals to the country will be exempt from UK tax on foreign income and gains for the first four years of their residency and can bring them to the UK tax-free (although they would lose their personal allowances). After four years of residency, however, they will be subject to tax on their worldwide income and gains. While there will be further consultation on how inheritance tax would be treated, there is a suggestion that worldwide inheritance tax would apply after ten years of UK residence.

In the interim, there will be transitional arrangements for current non-doms to encourage investment into the UK. This will include a 2-year period to bring wealth held overseas into the UK at a 12% rate of tax, as well as reducing their exposure to tax on foreign income to 50% in the tax year 2025/26.

In positive news for small businesses, the threshold for VAT registration was raised from £85,000 to £90,000 – potentially exempting thousands of enterprises. The government also hopes to extend the “full leasing” regime announced in November, widening the scope for tax breaks to include leased assets, provided conditions allow.

Duty on both fuel and alcohol have been frozen and will remain unchanged for the next 12 months.

Among the measures designed to boost government revenues were a new tax on vaping – and a one-off increase in tobacco “to maintain the financial incentive to choose vaping over smoking”. In addition, any air passengers travelling outside of economy class will see an increase in Air Passenger Duty, while the windfall tax on oil and gas company profits was extended until 2029.

While there was nothing new on capital gains or dividend tax, several changes to tax-free allowances announced in last year’s Autumn budget are due to take effect in April. The tax-free allowance for capital gains will be halved from £6 000 to £3 000 (having already been cut from £12 300 in 2023). Similarly, the tax-free allowance for dividends will fall from £1000 to just £500.

According to the South China Morning Post, China’s exports rose 7.1% in January and February compared to a year earlier, while imports went up 3.5%, both well more than consensus forecasts.

China is relying on high-demand exports to fuel growth and fulfil targets, with premier Xi vowing to bolster trade in his government work report.

Featured Stock

Shoprite recently released its interim results to end December 2023. Sales grew by 13.9% to R121.1 billion and on a like-for-like basis, sales growth was 6.5%. Gross profit rose by 14.7% to R28.6 billion and gross profit margin increased by 10 basis points to 23.6%. Diluted headline earnings per share (HEPS) rose by 7.6% to 621.4c and an interim dividend of 267 cents per share was declared, an increase of 7.7%

According to Nielsen IQ, the group gained R4 billion worth of South African market share in the interim period, which marks 58 months of uninterrupted market share gains in South Africa. Checkers is estimated to have a market share more than 15%, while Shoprite/Usave’s market share exceeds 20%.

While this type of high single digit growth is good in comparison with many other listed food retailers. It is below Shoprite’s longer-term averages and highlights how even an outstanding operator such as Shoprite is taking strain in this difficult economic environment.;

But there are many rays of light for the longer-term future of the group. Its home delivery system Sixty60 is the leader in the field and according to management is already highly profitable, which is an achievement in itself.

Shoprite has many other long-term irons in the fire that will likely only bear fruit properly in the long term. Examples include the clothing chain UNIQ and MediRite, the pharmacy chain.

From a valuation perspective, Shoprite isn’t cheap. But. Like that other highly rated stalwart of the food and drug sector, Clicks, it’s probably unlikely to get significantly cheaper as long as it sticks to its knitting, as it seems set fair to do.

Log in to ThinkPortal and make the most of these local and global macroeconomic insights by trading today.

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.