Both Asian and European markets have been trading in the red today after the end of the worst quarter since 2008, and the main future contracts on American indices are pointing to a lower open also after President Trump warned about a painful two weeks ahead.

Oil is still looking for a bottom as it finished its worst quarter ever down 67% YTD. NYM WTI Crude is trading at $20.11 while writing this report with a short-term target of $19.20 and longer-term target of $15 per barrel.

Gold, the classic safe haven, fell to $1,569 but rebounded to above $1,1594. It is currently flirting with $1,600 levels; breaking this level will push prices toward $1,615. On the other hand, if that level capped that bounce, gold would fall again below $1,575 again.

With the start of the new quarter and continued support from governments and central banks around the world, markets still carefully monitor the Covid-19 pandemic and its impact on investor sentiment.

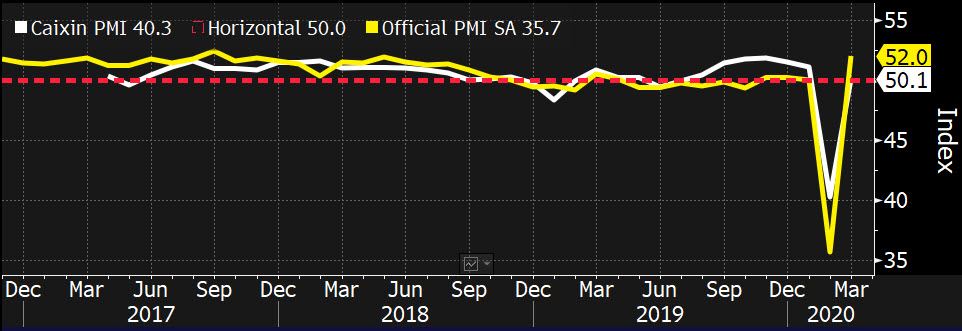

China is gradually reopening for business. Yesterday’s PMI reading showed a recovery in sentiment and a return to expansionary territory. In Europe the outbreak is reaching its peak, but in the US we are still waiting for the peak and its full impact on the markets.

It is not a V-shape recovery, China PMIs:

Source: Bloomberg

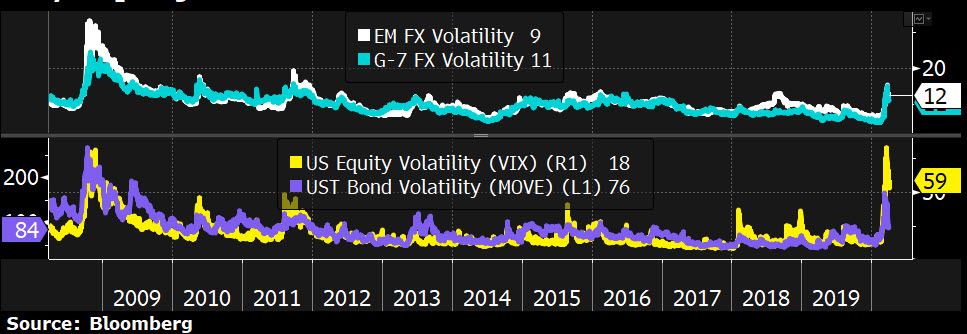

Volatility fell but it is still triple the average of the last decade; things could get worse and hopes of a V-shaped recovery is deteriorating as time passes.

G7, Emerging Markets currencies, Bonds, and equities volatility are higher than their average for the last decade:

Source: Bloomberg

Today, we are waiting the release for ISM’s manufacturing PMI for the USA. It is likely to mirror current sentiment as it is already priced into the market. However, the depth of the fall will be significant. Investors expect a reading at 44.9 (any reading above 50 means expansion, below 50 means a contraction) but we could see worse than what is expected.

Back