...amid optimism over stimulus and news that President Donald Trump may soon leave the hospital

It has been a positive start to the new week, with the major global indices, energy prices and major currency pairs all rising this morning, causing safe-haven Japanese yen to dip.

Investor sentiment has been supported by several factors:

- First, it appears as though Donald Trump’s illness is going to be short-lived and he may be discharged from hospital as soon as later today after receiving treatment for Covid-19. Whether the President have the strength to get back on the campaign trail remains to be seen, but judging by the events over the weekend and the fact Joe Biden continues to pull further ahead in the polls, I wouldn’t be surprised if he gets back to work this week.

- Optimism has also grown that a fiscal stimulus deal can be reached soon, which the economy badly needs amid growing signs that the pace of the economic recovery post lockdown has slowed down quicker than expected. Trump tweeted over the weekend that a deal needs to get done, echoing optimism from Nancy Pelosi on Friday. On a side note, should there be no agreement on the stimulus before the election is out of the way, a win for Biden mean the Democrats could then pass their original $3.4 trillion stimulus in January. This would be a much bigger package than would be possible in a potential bi-partisan agreement pre-election. So, although Trump is widely seen as business- and market-friendly, this may explain why investors do not appear to be too concerned about the rising probability of Biden winning the election, at least in so far as the short-term is concerned. It is also worth pointing out that a clear win by Biden would reduce the risk of a contested election, and thereby the uncertainty that comes with any legal battles.

- On the macro front, it has been a good day for economic data. The services PMIs across Europe (excluding Spain) pointed to improving conditions, albeit from depressed levels, while Eurozone retail sales turned out be much stronger than expected in August as investor confidence didn’t take as big a knock as had been expected by the resurgent coronavirus cases, judging by the latest Sentix Investor Confidence reading (see below for more).

Positive last week

Monday’s bullish mode comes on the back of a somewhat positive last week for risk assets, when we saw the dollar fall back after its recent recovery, while the major equity indices ended a volatile week higher, along with gold and silver. The price action was more in line with what we have seen post lockdown, as investors remained optimistic that a US government fiscal stimulus deal was likely in the coming weeks and shrugged off news that Donald Trump had caught the coronavirus, and the uncertainty this brings. Investors also largely ignored rising infection rates, as cases continued to climb across large European cities and some other parts of the world. That said, lockdown fears did cause some shares, such as travel stocks, to come under renewed pressure while demand concerns hit oil prices – which ended lower for the second week – before rebounding on Monday. Meanwhile, Trump’s illness overshadowed a mixed US jobs report on Friday, which disappointed on the headline front as ‘only’ 661 thousand non-farm jobs were added into the economy last month compared with 900 thousand expected and an upwardly revised 1.489 million jobs the month before. However, the headline disappointed mainly because of a dip in government jobs, while the private sector created more employment than expected. The unemployment rate dropped unexpectedly sharply to 7.9% from 8.4%, but this was largely a reflection of more people dropping out of the labour force.

Looking Ahead: Coronavirus, Donald Trump and stimulus hopes

Looking ahead to the rest of the week there is not an awful lot to get excited about to be honest. The economic calendar only features only a handful of scheduled macro events. But without a doubt, the main area of focus will be on the resurgent coronavirus and as investors try and figure out what Trump’s illness means for the upcoming election and the prospect of the stimulus package being signed. If there is more progress on the stimulus front, then expect the markets to push further higher, otherwise, it is difficult to see where the trigger for another rally will come from.

Brexit: significant differences remains

Meanwhile as the second wave of infections in the UK and across Europe gets stronger and needs to be monitored closely, traders will also need to pay close attention to the latest Brexit headlines as talks enter a critical stage. There were some conflicting headlines regarding to the latest round of Brexit talks last week. The long and short of it is that some progress has been made but significant differences still remain, with time fast running out. The EU's Michel Barnier said the latest round of negotiations saw some areas of progress but level playing field/state aid and fisheries are among a lot of open issues still and sees `persistent’, and ‘serious divergences' in Brexit talks. The UK’s chief Brexit negotiator David Frost added that the “gap between us is unfortunately very large” on fisheries. Mr Frost warned that without further realism and flexibility from the EU, it may become impossible to bridge those gaps. The EU-UK trade talks will continue in London in this week, followed by another round of talks in Brussels the following week.

In a nutshell

The upcoming presidential election, Brexit uncertainty and rising coronavirus cases means the road ahead will be bumpy for risk assets. It is very difficult to say which direction risk assets will be heading given these uncertainties. Without further stimulus, the markets look vulnerable. Overall, I do think the best days of the bull trend in the equity markets are over and we will see more side-ways action leading up to the elections, as investors will unlikely be in the mood to take on too much risk. This implies that the dollar may also be going side-ways, rather than trending in one or the other direction.

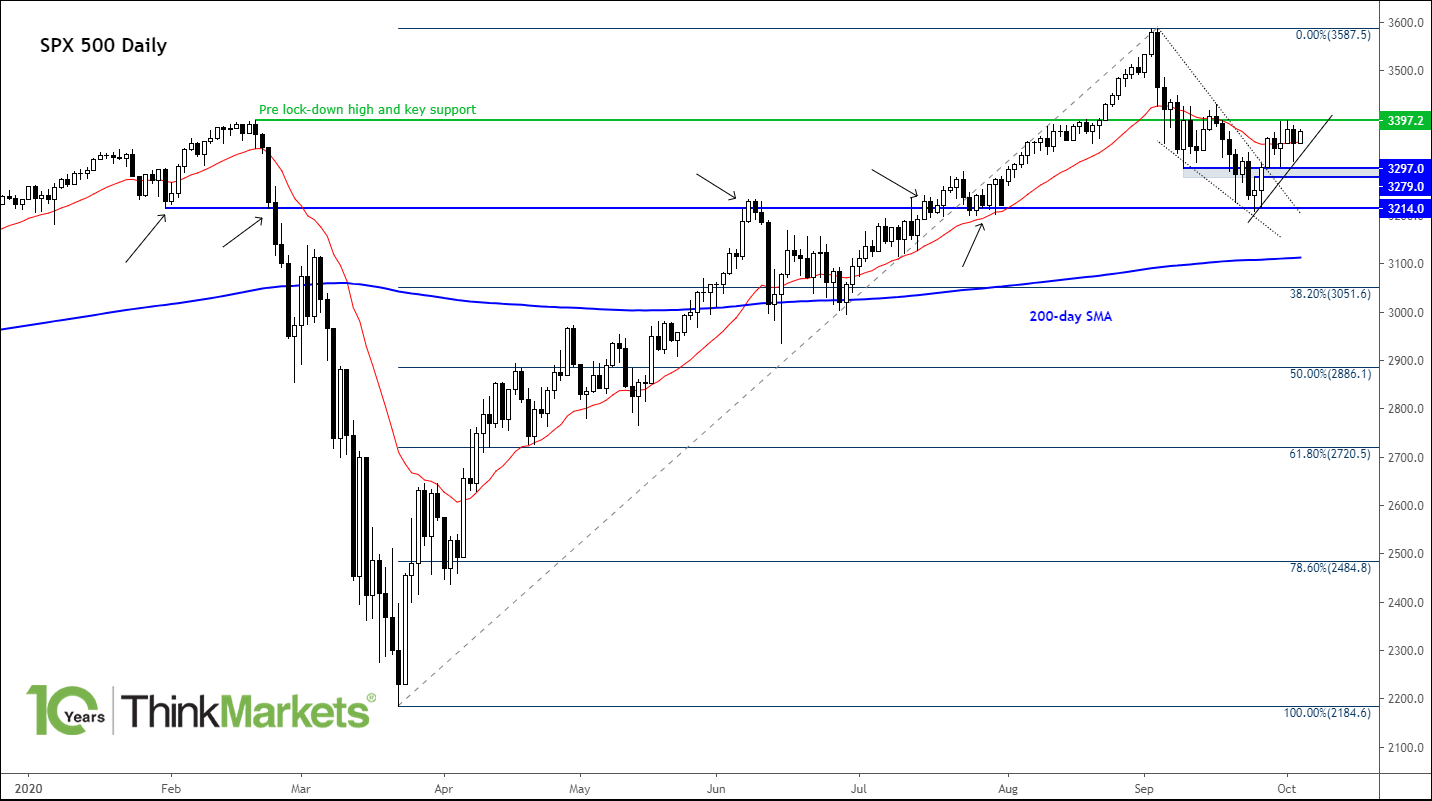

But, for now, the path of least resistance is still to the upside for indices after the S&P broke out of its falling wedge pattern and held this key support:

From here, the S&P needs to go back above the previous all-time high that was hit before the lockdown at just under 3400. If it rises and holds above this level, then we could see a run to a new high soon. The trigger could be the potential signing of the fiscal stimulus package. However, if the index goes back below the short-term support range between 3279 and 3297, then this would be a bearish development, in which case a drop towards the 200-day average would become likely. The trigger for this potential scenario could be if risks of a contest election rises again, or there is no fiscal stimulus.

Economic calendar

The week ahead is very quiet in terms of macro data. Here are the data highlights:

Monday

- Flash services PMI from Spain disappointed but Italy beat while the final PMIs from most other parts of Europe were revised higher (except for French PMI):

- UK 56.1 vs Exp. 55.0 (Prev 55.1)

- EZ 48.0 vs Exp 47.6 (Prev 47.6)

- Spain 42.4 vs Exp 46.3 (Prev 47.7)

- France 47.5 vs Exp 47.5 (Prev 47.5)

- Germany 50.6 vs Exp 49.1 (Prev 49.1)

- Eurozone Sentix Investor Confidence Oct: -8.3 (exp -9.3; prev -8.0)

- Eurozone retail sales +4.4% m/m vs. +2.4% expected and -1.8% lass

- Coming up: US ISM non-manufacturing PMI (expected to moderate to 56.3 from 56.9 last)

Tuesday

- RBA likely to hold rates steady at 0.25%

- Australia Annual Budget Release

- German Factory Orders expected +3.0% m/m vs. +2.8% last

- Central bank speeches: ECB’s President Lagarde and Fed’s Chair Powell

Wednesday

- German Industrial Production m/m

- Speech by ECB’s Lagarde

- FOMC Meeting Minutes

Thursday

- ECB Monetary Policy Meeting Accounts

- Central bank speeches: BoE’s Governor Baily and BoC’s Governor Macklem

- US Unemployment Claims

Friday

- UK monthly GDP and industrial production

- Canadian jobs report

Back