Contents

-

Q4 Outlook Overview: Key Drivers

-

Q4 FX & Metals Outlook: King Dollar is Back, but for How Long?

-

Q4 Crude Outlook: Oil Faces Key Demand Risks

-

Q4 EM Outlook: Stagflation, dollar threaten emerging markets

-

Q4 Global Stock Market Outlook

-

Q4 Crypto Outlook

1. Q4 Outlook Overview: Key Drivers

By Fawad Razaqzada

After several quarters of consecutive gains for global stocks (especially the US and definitely not China), the final month of the third quarter saw the rally come to an abrupt halt. Volatility rose in September after months of relative calm as stagflation concerns replaced optimism about economic growth. Investors realised that supply bottlenecks were not only fuelling inflation but were hurting economic activity. Surging energy prices exacerbated inflationary pressures, which, in turn, worried previously-relaxed central bank officials in the US and UK. The Federal Reserve prepared the markets for the potential tapering of its massive stimulus programme before the end of this year, sending bond yields and the dollar surging higher against the likes of the euro and yen, where the central banks remained dovish. The dollar hurt emerging market currencies, with the Turkish lira falling to a new record low, while the likes of Pakistani and Indian rupees were pressured further by surging energy prices, making imports of oil and other commodities even dearer. Elsewhere, precious metals failed to find much haven flows despite the stock market volatility, as they were held back by rising yields and stronger dollar. Silver suffered a double whammy as concerns about growth weighed on industrial demand expectations from China – something which also hurt copper prices. September (or China) also ruined what was otherwise a decent quarter for cryptos.

Heading into the final quarter of the year, concerns over stagflation and hyper inflation will dominate the agenda. Investors will want to know what steps governments and central banks might take to stem price pressures, and at the same time, keep their respective economies ticking over. Will the Fed taper QE faster to avoid overcooking inflation? Will the OPEC+ release more than 400K barrels of oil per day to halt the oil price rally? Will gold finally catch a haven bid or will the dollar prove too hot for the metal once again?

2. Q4 FX & Metals Outlook: King Dollar is Back, but for How Long?

By Victor Golovtchenko

After a blissful third quarter and in line with our outlook the US dollar has managed to eke out some gains over the summer months and especially in the last days of Q3. The current macroeconomic environment is favouring a continuation of this trend with the Federal Reserve expected to end its debt purchases by the middle of next year. The key for US dollar strength in the fourth quarter is: how long can it last?

There is no doubt that the currency market has some further repricing to do when it comes to the greenback - the Fed is widely expected to taper in November and the present conditions in the labor market will be closely watched. That said, the weight of these macroeconomic reports is greatly diminished, now that Chairman Powell communicated the intentions of the Fed to move at the next Fed meeting in the beginning of November.

We expect US dollar strength to persist into that meeting and perhaps start to taper off (pun intended) after the news is finally announced. The ECB and the BOE shouldn’t take too long after the Fed to move, and the repricing of that could trap US dollar bulls on the long side. The assumption here is that we’re going to see a fairly strong rally over the coming month, with November probably being neutral, and a full reversal ensues into the end of the quarter as other central banks turn more hawkish.

That said, the ongoing equity markets correction could put a dent into this outlook. We expect that should the market fall too quickly, the Fed will get spooked and will continue to hold its foot on the gas pedal. If that happens, the credibility of the international markets in the US dollar’s value as a reserve currency will greatly diminish and provide significant impetus for a rebound of USD bears.

Speaking of the risks to the outlook, we expect that gold and silver will continue to be highly correlated to the US dollar’s performance. The same factors that we discussed above hold true for precious metals and should we see a meaningful market correction that triggers the Fed to walk back on its promise to taper asset purchases, the hedging value of gold should resurface.

In short, the actions of the US Federal Reserve are the key factor for US dollar and precious metals traders this quarter. Should the Fed manage to taper, in the face of a falling stock market, the US dollar could rally significantly from current levels and level off into the end of the quarter as other central banks start contemplating to reduce their monetary stimulus measures. If, however, the Fed flip flops, the FX market is likely to sell off US dollars aggressively and gold and silver should skyrocket, as the confidence in the US central bank’s ability to manage the economy declines materially.

3. Q4 Crude Outlook: Oil Faces Key Demand Risks

By Fawad Razaqzada

Oil prices rose for the sixth straight quarter as demand recovered from the impact of lockdowns during the pandemic and supply remained tight. Heading into the final quarter of the year, my personal view is that I cannot see how crude oil prices will rising significantly further from here and reckon the risks are skewed to the downside.

In short, I reckon the growth in demand could slow down sharply, because of (1) EM currency crisis in several oil-importing nations as USD extends rally, (2) China’s slowing recovery and (2) supply bottlenecks could undermine the economic recovery in more developed economies.

Meanwhile, the OPEC+ might address some of the supply risks – possibly as its meeting schedule for 4th October.

Why oil has rallied

September saw oil prices hit new multi-year highs. In the US, crude production dropped due to the impact of the hurricane Ida, causing stockpiles to shrink. Inventories have actually declined across the world amid supply shortages and stronger-than-expected demand growth. Crude has also been supported by the fact the energy sector has been rallying across the board. Scorching hot weather in parts of Europe caused demand for cooling to surge, which, in turn, increased natural gas demand by electric power plants, causing inventories to plummet. As gas prices rose, some factories halted production of things like fertilizers while some switched to oil-fired power generation, boosting demand for crude. Expectations that more companies will turn to oil for power generation helped to keep the rally intact despite stock market sell-off and the dollar’s rally in September.

Oil prices face major headwinds

While oil has had a great year so far, that’s not to say prices will continue rising, as the market is always forward-looking. Looking ahead, I see some potential obstacles that could derail the rally. So, I reckon that the risks are skewed to the downside for oil prices. Some of the reasons why I think that might be the case are listed below:

- Emerging market currency crisis is already being felt in places like Pakistan and Turkey. India could potentially be next. India is the world’s third largest oil importer and consumer, meaning that if the dollar rises against the rupee, it would hurt demand for oil and other commodities as the strength of USD would make imports even dearer.

- Weakening economic growth in China and the fact they have tapped their strategic reserves indicate demand from the world’s largest oil importer is already getting soft

- Supply bottlenecks could undermine the economic recovery in more developed economies.

So, the net result of the above: potentially weaker demand growth for oil in the months ahead and thus lower prices.

OPEC + may boost output more robustly

For crude oil, the key question moving forward is how the OPEC+ will respond. Right now, some members in the group are undoubtedly loving high oil prices. But if prices get too expensive, they could negatively impact economic growth, which in turn will reduce demand for oil in the near future. So, the OPEC+ are going to have to make a decision and it will be interesting how they will respond.

If the OPEC+ decide to continue restoring production levels by 400,000 barrels a day each month, as previously agreed, this will not change the trajectory of oil prices. However, if they decide to ease supply curbs a bit more aggressively then this may help to halt the rally. The group may decide to ramp up production by 800K bpd at their meeting on October 4, with the view of potentially not raising output in the next month. The impact of this would be more supplies hitting the market in November.

At $80 for a barrel of Brent oil, investors may realise that prices have gotten too strong. It is difficult to justify such prices when stagflation risks are on the rise and there is the potential for the OPEC+ to ramp up its production and allow more barrels to hit the global market to prevent demand from collapsing.

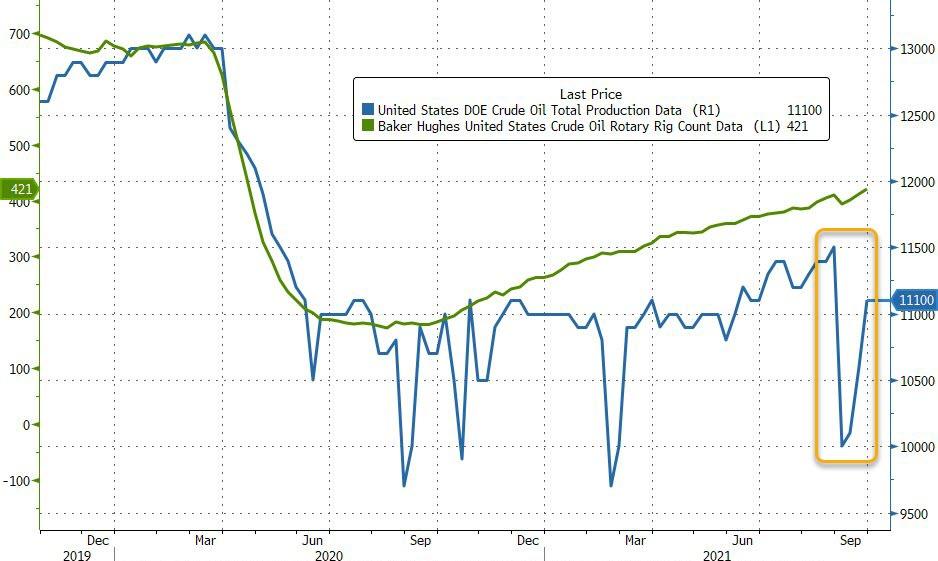

What’s more, it looks like the hurricane-hit US supplies have been slowing re-stored and rig counts continue to rise:

Source: Bloomberg

Supply tightness is therefore easing in the US and depending on what the OPEC decides and how the demand dynamics evolve in the coming months, price pressures could ease sharply.

4. Q4 EM Outlook: Stagflation, dollar threaten emerging markets

By Fawad Razaqzada

Currency crises in some emerging market economies poses additional risk to global equities and other risk-sensitive assets in Q4. The ongoing supply chain disruptions sweeping major economies have boosted stagflation risks. That’s, a period where inflation is spiking despite weaker economic growth. Supply bottlenecks have already hurt activity in major global economies and as we entered Q4, the situation was still deteriorating. The risk to emerging markets from stagflation is twofold.

First, foreign demand for EM exports could weaken as the global economy slows down as stagflation takes hold.

Second, the strength of US dollar, if sustained, will make foreign imports of commodities dearer for EM economies. Crude oil, copper and other materials are all priced in the dollar. With the greenback staging a strong recovery so far this year, at the same time as supply bottlenecks have helped to fuel a rally in some commodity prices, this means that businesses and consumers in EM economies will feel the impact of inflation even more.

In more advanced economies, inflation is already sharply higher:

Source: FT and OECD

If inflation picks up further in these nations, causing a drop in real disposable incomes, then it could hurt exports from EM countries, compounding the troubles for their currencies.

5. Q4 Global Stock Market Outlook

By Kearabilwe Nonyana

It seems as if the world is moving in circles when things look brighter, they get darker. We are done with 75% of the year and it has been a wonder as to why the equity indices and equities remain close to all-time highs even in the face of slowing global growth and the threat of the delta variant engulfing the world.

Forward looking valuations

US earnings season for the 3rd quarter commences in the first two weeks of October and the barometer of how global stocks will perform will be seen in the performance of companies in the S&P500. It sounds like a repetition, but the technology sector listed stocks are trading at very high multiples and valuations and would need consistent earnings beats in the next quarter to sustain these hefty ratings given by market participants. The Nasdaq composite index is trading at a P/E of 35.96 and the S&P500 is trading at a higher valuation of 35.96. These are hefty valuations and would require correct manoeuvring in determining the momentum of the market. In Europe, the recent election results in Germany have made market participants sceptical about the future political landscape for the euro zone. Olaf Scholz of the socialist centre left party won the majority and can formulate a coalition government. This poses a threat to policy certainty in the euro zone’s most industrialised and strongest economy. Common prosperity and inequality have been at the forefront of many governments as there is a growing discontent with how within the pandemic people who were invested in the stock markets got wealthier while people who earn incomes had a threat to their income. The FTSE 100 sits very close to its 52-week high of 7224.46 and a P/E of 15.070 which in comparison to the US market seems better priced but the economic prospects of the UK are far less rosy than the US. The Euro Stoxx 600 has had a YTD return of 16.98% and has given back about 3.29% in the one month before the end of the quarter. The predicted growth of the 3rd quarter was 8.3% for the Eurozone.

China, China, China

China holds the world’s economic fortunes squarely in their hands. The Chinese economy was the first to come out of this pandemic and that gave it an added advantage in the global economic recovery. China remains one of the countries still driving economic industrialisation. It has not been averse to spending money to increase their industrialisation. The Chinese stock market has not yet found the same fortune. The Chinese factory activity has shown signs of slowing down and there have been cutbacks on CO2 emissions. These have largely targeted steel makers, weighing heavily on Iron ore prices. The threat of increased regulations as well as energy shortages in China threatens economic growth and the prospects of the Chinese stock index recovering. I expect some consolidation on China stock indices as well as general emerging markets.

6. Q4 Crypto Outlook

By Carl Capolingua

Quite a bit has happened since our last quarterly crypto update, but activity and volatility is what we have come to expect from this exciting asset class! Here are the key developments from the last three months, and then we'll conclude with a look ahead to the factors that may impact cryptocurrencies in the final quarter of the year.

B Word Bolsters Bitcoin

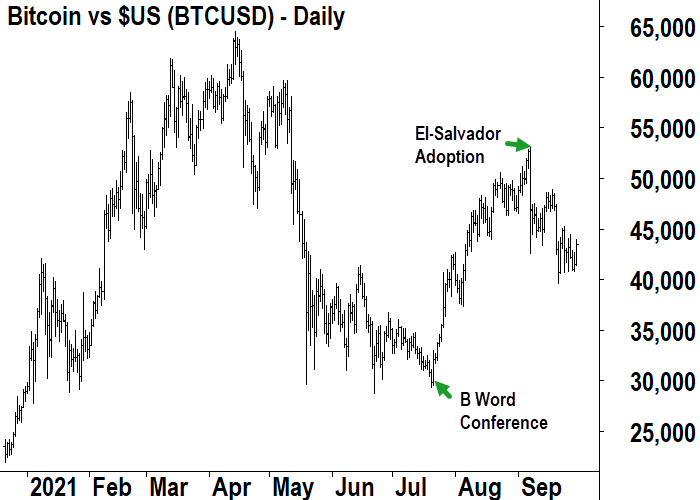

It was make or break for Bitcoin (BTC), and really, the entire crypto space in July as prices slumped amid threats of increased regulation, and aggressive moves from the Chinese government to crack down on cryptocurrency miners and related businesses operating within mainland China.

As the price of one Bitcoin threatened to decisively break below the key US$30,000 support level, megastar cryptocurrency proponents Cathy Wood (Ark Invest), Jack Dorsey (CEO of Twitter and Square), and Elon Musk (CEO of Tesla and SpaceX) agreed to meet in a publically televised virtual conference dubbed The B Word Conference.

Over a couple of hours, the trio discussed the benefits and bright future for Bitcoin and the cryptocurrency universe in general. It was enough to spur a short covering and buy-the-dip rally that swung the momentum of the entire cryptocurrency market. The rally saw the market capitalisation of cryptocurrencies more than double over the next few weeks.

El-Salvador Adopts Bitcoin as Legal Tender

The other major news in Q3 was the official adoption of Bitcoin as legal tender in the El-Salvador, which took effect on September 7.

El-Salvador's economy is heavily reliant on remittances from ex-patriots who work overseas and send money to relatives back home. Approximately 23% of the country's GDP was directly related to remittances, and transfer fees have historically been extremely high, costing around US$400 million per year. The adoption allows El-Salvadorians to transfer wealth instantly, with wait for it, zero fees.

Whether by coincidence, or due the fact the market had risen in anticipation of the adoption, September 7 saw a sharp and substantial sell-off in Bitcoin, which it is still yet to recover from.

Smart Contracts Race Hots Up

Smart contracts allow developers to build decentralised finance (DeFi) applications which allow users to conduct peer-to-peer financial transactions over a blockchain. Up until very recently, the major player in the smart contracts space was Ethereum (ETH).

On September 12, major DeFi rival Cardano (ADA) launched its own smart contract capability following the completion of its Alonzo upgrade. Cardano's blockchain technology is widely considered to be superior to Ethereum's as it uses a more efficient proof of stake consensus mechanism compared to Ethereum's energy intensive proof of work. Proponents also note Cardano's significant speed improvements (in terms of transactions per second "TPS") and the network's significantly lower transaction costs. ADA, Cardano's native token almost doubled in value leading up to the launch.

Ethereum is slowly transitioning to proof of stake in order to alleviate some of its energy efficiency, speed and cost issues, but Ethereum 2.0 as it has been dubbed, is not expected to be completed until well into next year. The developers of Ethereum did launch an important update in Q3 however. The London update introduced an automated burn of some of the fees generated by verifying transactions on the network. This means the fees, known as "gas,” are lost to the system forever, thus reducing the overall supply of Ethereum. Fans of the cryptocurrency hope that the reduced supply of Ethereum will lead to higher prices in the future.

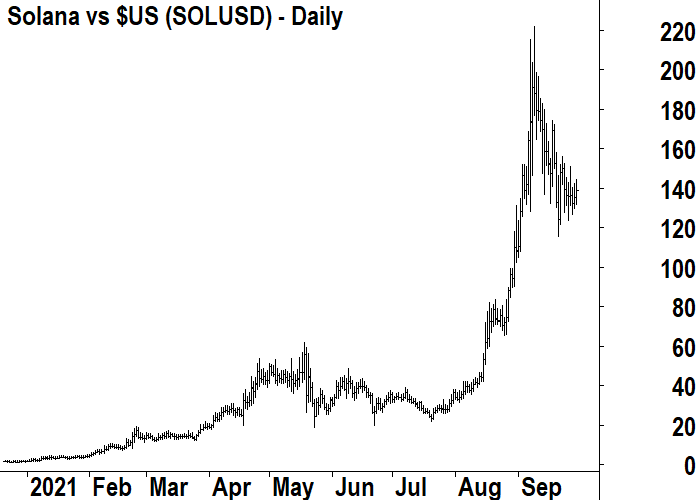

A discussion on Q3 smart contract blockchain developments wouldn't be complete without a shout out to Solana (SOL). The smart contract enabled blockchain jumped as much as 650% over the quarter and is up a staggering 18000% since it launched back in April 2020. Proponents of Solana note its ultra-fast transaction speed, as it is potentially capable of processing as many as 710,000 TPS. This compares most favourably to Bitcoin's 5-10 TPS, and Ethereum's TPS 10-15 TPS.

Altcoin Recovery, but Memecoins Miss Out

More broadly speaking, alt-coins (which are usually considered to be cryptocurrency coins and tokens outside of Bitcoin, Ethereum and Cardano), also experienced a strong recovery in the quarter with the market capitalisation of alt-coins roughly doubling from the July lows before experiencing a modest pullback in September.

An interesting development in the space was the conspicuous absence of memecoins such as Dogecoin and ShibaInu from the broader rally. Memecoins are cryptocurrencies which were created as a joke, and typically are only traded by investors as pure speculation or "for fun". Instead, the best performing altcoins were those with coherent development schedules, progress, and real-world usage applications. Altcoins Algorand (ALGO), Avalanche (AVAX), and COTI, and were all big gainers in the quarter.

It is possible that those trading cryptocurrencies simply for fun moved on to another rapidly expanding crypto concept, non-fungible tokens "NFTs". An NFT is a digitised asset whose provenance and ownership can be tracked and verified via a blockchain (like Ethereum or Cardano). Many digital artists (but really anyone with the nous to create a JPEG image and put it on a blockchain!) have enjoyed the ravenous appetite for investors in this new asset class. Many NFTs are now selling for millions of dollars after having started their lives as worthless pixels!

Look ahead to Q4

Whilst the day-to-day price movements for various cryptocurrencies will no doubt continue to be more volatile than more traditional asset classes, there are a number of key themes investors should look out for as 2021 draws to a close.

Firstly, and potentially the most imminent, is China's continuing crackdown on cryptocurrency businesses and transactions. Most analysts expect China to continue to reinforce their existing position that virtual currencies are not legal, and therefore it is illegal to operate a cryptocurrency business (e.g. one that issues cryptocurrencies or facilitates their transfers) within China. Actions by the Chinese government to curb cryptocurrency activities earlier in the year saw a major decline in the number of computers (or "nodes") supporting the Bitcoin network. It will likely take some time for this support to relocate to other jurisdictions, and as many Chinese cryptocurrency businesses incur costs in doing so, their sales of Bitcoin to recoup those costs may weigh on prices.

The next item to watch out for in Q4 is also related to regulation, but in Western jurisdictions such as the USA, the UK, and Europe. There is a growing call from various regulatory bodies including central banks and the Securities and Investment Commission "SEC" for more oversight of the cryptocurrency industry, in particular with respect to new issuance and stable coins. Most of these developments are likely to be a positive in the long run however, as greater oversight of issuers would likely increase investor protection, and greater regulations on which assets stable coins are required to hold as collateral would also help to increase the stability of the wider cryptocurrency ecosystem.

Finally, and this one is a clear positive, we may see further progress made towards a publicly listed Bitcoin, or more broadly based, cryptocurrency exchange traded fund "ETF". This would allow a wider adoption of the asset class into investors' portfolios. It would also be a significant step in further legitimising cryptocurrency as a mainstream investment alternative.

Any opinions, news, research, analyses, prices or other information contained on this website is provided as general market commentary and does not constitute investment advice. ThinkMarkets will not accept liability for any loss or damage including, without limitation, to any loss of profit which may arise directly or indirectly from use of or reliance on such information.