The market’s initial reaction was negative after an utterly chaotic Presidential debate last night, but the losses were mild, and the negativity didn’t last too long as index futures recovered shortly before the open on Wall Street. As shocking as the debate was, it was nothing unexpected from Donald Trump. Supporters of Donald Trump will still support him in the votes, but this was a marginal victory for Joe Biden, as reflected by betting odds moving in his favour. The prospect of a contested election is clearly unnerving some investors, but there is still time left for people who are undecided to make up their minds and in the next two debates we may see a more decisive move in the opinion polls – and, in turn, the markets.

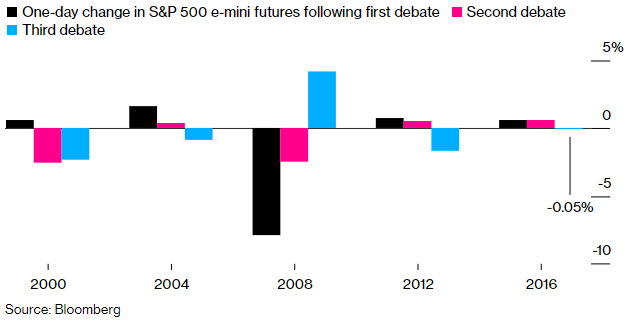

Indeed, it is rare for the markets to move sharply lower after the first debate, as this diagram from Bloomberg shows:

If anything, the S&P has ended higher in the past 4 out of the 5 occasions following the first debate. So, if this is anything to go by, then the markets may well end up in the positive territory today.

But if in the coming days and weeks, Biden takes a clear lead in the polls, investors may not like this outcome much as taxes will likely rise under Joe Biden’s leadership, and we could see some weakness for the indices leading up to the election. However, this will likely be a short-term move, as whoever wins the elections, monetary policy will remain extraordinary loose for years to come. Indeed, it is monetary policy – interest rates and QE – that have been the major driver behind equity markets rather than fiscal policy. So, the outcome of the election is unlikely to materially impact the stock market’s long-term direction.

As investors wonder what the potential implications of the debates and the outcome of the election will be on the markets, the current trend remains positive towards equities, thanks mainly to ongoing central bank support hopes over a vaccine. Signs that lawmakers are getting closer to reaching a fiscal stimulus deal is also helping to offset election worries.

Recovery hopes alive as global data beat expectations

We have also had a few stronger-than-expected macro pointers released today, suggesting economic recovery is still ongoing despite the resurgent coronavirus cases. The latest Chinese PMIs, German retail sales (3.1% m/m) and French consumer spending (2.3% m/m) were all positive. From the US, the ADP private sector payrolls report came in well above expectations with a print of 749K vs. 650K expected, while the Chicago PMI surged unexpectedly sharply to 62.4 from 51.2 previously. Meanwhile, Canadian monthly GDP showed a better-than-expected 3% jump following a 6.5% increase the month before.

S&P holds support

After breaking out of its falling wedge pattern to the upside a few days ago, the S&P has managed to hold the initial rounded-retest of the broken resistance in the area between 3279 and 3297:

Source: ThinkMarkets and TradingView.com

So far, the bulls thus remain in control. It will be a positive outcome if they reclaim the 21-day exponential on a daily closing basis, next. If successful, we could soon be talking about 3500 again and possibly a new record high.

The bears will need to hold their ground and prevent the index from making further gains, for if that happens it could trigger a short-squeeze rally. From the bears’ point of view, a move below the abovementioned support between 3279 and 3297 would be a positive outcome. However, for as long as that 3214 support holds, the longer term outlook would remain bullish regardless of what the index may do in the short-term.

Overall, I think the best days of the bull trend are over and we will see more side-ways actions leading up to the elections, as investors will unlikely be in the mood to take too much risk on in the event of a shock.