Here is our week ahead preview for the week commencing 14 September 2020.

This week has been dominated by events in Europe, with rising Covid-19 infections making Western Europe the new global hotspot for the virus, while the European Central Bank decided not to intervene to weaken the euro. Yet in terms of market reaction, it has been the dreaded B-word causing the most prominent moves in sterling. As Brexit-related uncertainty rose, this hurt the GBP/USD and other pound crosses badly and the downbeat currency was limping as the weekend approached ahead of more talks between the two sides next week.

But there has been a silver lining behind the pound sell-off: the weaker exchange rate has helped the FTSE 100 to end a 3-week sell-off, at least for now. The FTSE was up this morning, outperforming the rest of Europe. However, it remains to be seen whether investors will continue to shrug off rising new virus cases in Europe and remain positive towards risk in the week ahead amid vaccine hopes and ongoing central bank support, or dump stocks.

Three major central bank meetings

The US Federal Reserve will decide on monetary policy on Wednesday 16th, while the Bank of Japan and the Bank of England will be making their decisions a day later on Thursday 17th.

Among them, the BoE’s policy decision will be the most important on in my view owing to increased Brexit uncertainty (see below). The BoJ is unlikely to make any major changes, while the Fed will likely be in a wait-and-see mode after loosening its belt completely in response to the pandemic.

- Although the BoE is widely expected to hold interest rates unchanged at 0.1% and QE at £745bn, rising Brexit-related uncertainty, and the revival of Covid-19 in the UK and Western Europe, means there is the potential for a dovish surprise from the bank. However, the dovish surprise, if seen, would most likely be in the form of preparing the markets for more QE in the near future rather than anything immediate. If that’s the case, then this should be good news for the FTSE, and bad for the pound.

- The FOMC will be meeting on Wednesday for the first time since the Federal Reserve moved to a new monetary policy regime called ‘Average Inflation Targeting’ (AIT). In essence this means, the Fed will be slower to hike rates even if the economy is growing above trend and the labour market is improving. One way to boost inflation is to drive the dollar lower. How will they achieve that remains to be seen as QE is running at full throttle and interest rates already at zero. What other policy tools do they have at their disposal? That’s a question Jay Powell and co. must provide in order to (re)gain credibility given their pathetic record of economic projections.

Brexit to remain at forefront

In so far as Brexit is concerned, the probability of a no-deal has risen sharply over the past few days as yet again no significant progress was made following this week’s talks between the two sides, and with time fast running out. If anything, the UK-EU relationship has deteriorated after the UK government's plan to rewrite the withdrawal accord angered EU lawmakers, who asked the plan to be scrapped. But the UK has refused this request, which, in turn, forced the EU to demand that it should be done so by the end of the month, or else… yeah, I don’t know what they would do if Boris Johnson’s government doesn’t listen, but it all points to more tension and uncertainty. This is why analysts at Morgan Stanley, for example, reckon that the chance of a “WTO Brexit” outcome has risen to 40% compared to 25% previously. This is their updated expectations and the likely reaction of the pound and the FTSE:

Are the markets too pessimistic on Brexit?

Are the markets too pessimistic on Brexit?

While the situation certainly looks bleak and a chaotic split with no trade deal is what is being priced in, that’s not to say the clouds will never clear and the storm won’t pass. Boris Johnson is playing a dangerous game, but this could be all part of his negotiation tactics and strategy. In the end, a compromise may be reached, and a cliff edge Brexit will probably be avoided, as it is not in either party’s interests.

So, I wouldn’t be surprised that after huffing and puffing, one of the two parties blink and agree to some comprise in the coming weeks. The pound could strengthen sharply if investors realise they have overreacted to this week’s events. Meanwhile, the UK and Japan were about to conclude a post-Brexit trade pact on Friday evening.

As Brexit talks continue between the EU and UK, expect the pound to become even more headline-driven in the days and weeks ahead. The BoE meeting has the potential to move it sharply in the event of a surprise policy change (see above for more).

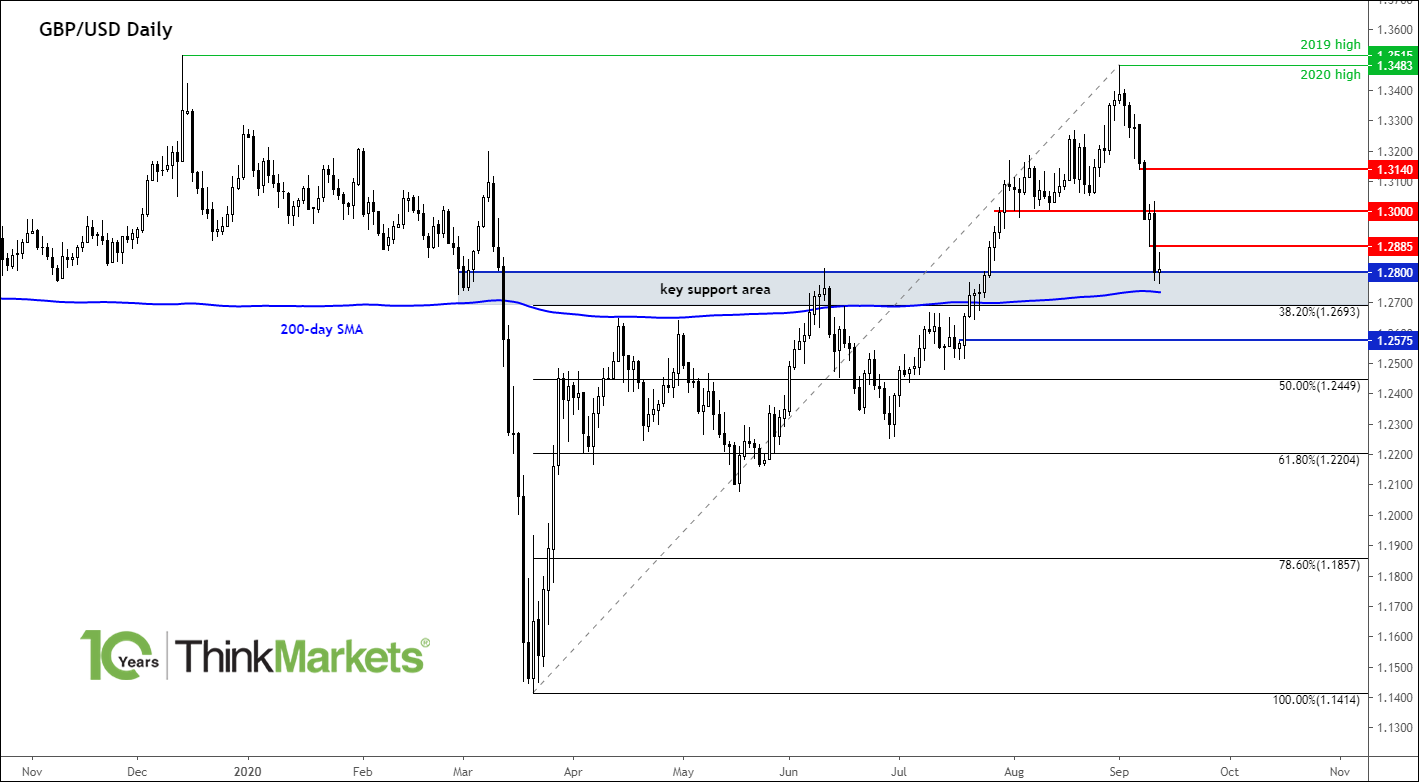

It is worth pointing out though that the GBP/USD has now reached some key technical levels, which means that those who are optimistic about the UK economy post Brexit, may be looking to buy the dip, potentially causing rates to turn higher after this week’s sharp sell-off.

Source: TradingView.com and ThinkMarkets

Economic data highlights

As well as Brexit situation and the above central bank meetings, there will be some key economic data to look forward to as well for the week ahead. Here are the week’s data highlights:

Monday: No major economic news

Tuesday:

- Chinese industrial production and retail sales

- UK jobless claims, average earnings and unemployment rate

Wednesday:

- UK CPI

- US retail sales

- FOMC policy statement, economic projections and Jay Powell's press conference

Thursday:

- New Zealand quarterly GDP

- Australian employment report

- Bank of Japan (BOJ) policy decision

- Bank of England (BoE) policy decision

- US Philly Fed Manufacturing Index and Unemployment Claims

Friday:

- UK retail sales

- Canadian retail sales

- US Preliminary UoM Consumer Sentiment

In a nutshell

So, there will be further Brexit talks, key data and a few central bank meetings to look forward to in the week ahead. All this at a time Western Europe has become the hotspot of coronavirus again. Will the euro weaken amid rising new virus cases in France and elsewhere, and given the ECB’s concerns over the exchange rate? A lot may depend on the outcome of the Fed and BoE policy decisions, which could impact the EUR/USD and EUR/GBP exchange rates meaningfully. The Fed will do its best to weaken the dollar further, which should be good news for gold all else being equal.

Back